Динамическая двойная стратегия «Супертренд» с учетом объема и цены

Обзор

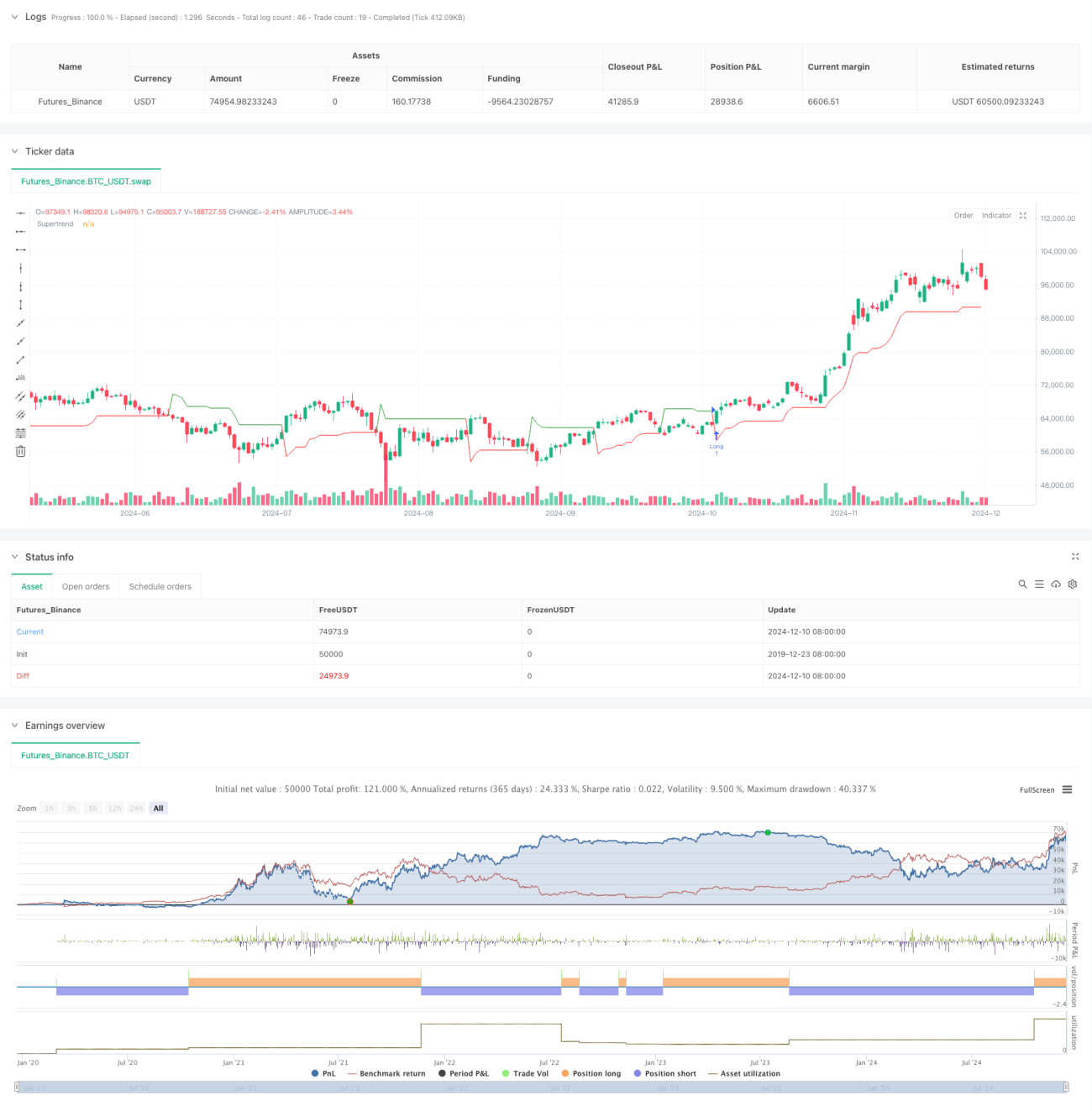

Это продвинутая количественная торговая стратегия, сочетающая индикатор SuperTrend и анализ объема. Стратегия выявляет потенциальные точки разворота тренда путем динамического отслеживания пересечений цены с линией SuperTrend и аномалий объема. Для обеспечения гибкости сделок и надежности контроля риска используются динамические стоп-лосс и тейк-профит, основанные на ATR (средний истинный диапазон).

Принцип стратегии

Основная логика стратегии базируется на следующих ключевых элементах:

- В качестве основного инструмента для определения тренда используется индикатор SuperTrend, который рассчитывается на основе ATR и динамически адаптируется к рыночной волатильности.

- За базовый уровень принимается 20-периодное скользящее среднее объема, а порог аномалии установлен на уровне 1,5-кратного превышения.

- Торговый сигнал генерируется, когда цена пробивает линию SuperTrend и объем удовлетворяет условию аномалии.

- Динамический стоп-лосс (1,5 ATR) и тейк-профит (3 ATR) на основе ATR позволяют оптимизировать соотношение риска и доходности.

Преимущества стратегии

- Высокая надежность сигналов: комбинация подтверждения от тренда и объема значительно снижает вероятность ложных сигналов.

- Совершенное управление рисками: динамические стоп-лосс и тейк-профит автоматически корректируют параметры риска в зависимости от волатильности рынка.

- Высокая адаптивность: параметры стратегии можно гибко настраивать под разные рыночные условия и торговые инструменты.

- Четкое исполнение: правила торговли ясны, без субъективных факторов, подходят для автоматизированной торговли.

Риски стратегии

- Риск бокового рынка: в условиях флэта возможны частые ложные сигналы.

- Риск проскальзывания: в периоды аномального объема может возникнуть значительное проскальзывание.

- Чувствительность к параметрам: эффективность стратегии сильно зависит от настроек параметров, требуется постоянная оптимизация.

- Системный риск: во время резких рыночных движений стоп-лосс может не сработать.

Направления оптимизации стратегии

- Внедрение фильтра силы тренда: добавление индикатора ADX для оценки силы тренда, открытие позиций только в периоды сильного тренда.

- Оптимизация индикатора объема: можно использовать относительную скорость изменения объема (ROC) вместо простого кратного порога.

- Улучшение механизма стоп-лосса: внедрение трейлинг-стопа для лучшей фиксации прибыли.

- Добавление временного фильтра: настройка временного окна для сделок, чтобы избежать периодов высокой волатильности.

Заключение

Данная стратегия, объединяя индикатор SuperTrend с анализом объема, создает торговую систему с высокой надежностью и адаптивностью. Ее преимущества заключаются в многомерном подтверждении сигналов и динамическом управлении рисками, однако важно учитывать влияние рыночных условий на производительность стратегии. Благодаря постоянной оптимизации и усовершенствованию, стратегия способна показывать стабильные результаты в различных рыночных условиях.

- 1