Обзор

Мультииндикаторная взвешенная интеллектуальная торговая стратегия представляет собой комплексную количественную торговую систему, которая генерирует решения путем объединения сигналов нескольких технических индикаторов с присвоением различных весов. Стратегия сочетает в себе такие инструменты технического анализа, как MACD, Stochastic RSI, EMA, SuperTrend и пересечение скользящих средних, формируя всесторонний торговый фреймворк. Система не только поддерживает многоуровневый тейк-профит и динамический стоп-лосс, но и автоматически корректирует параметры в зависимости от рыночных условий, что обеспечивает высокую адаптивность в различных рыночных средах. Стратегия особенно подходит для средне- и долгосрочных трейдеров, делая торговые решения более стабильными и надежными благодаря системе распределения весов.

Принцип стратегии

Ядро стратегии заключается в её взвешенной сигнальной системе, которая генерирует сигналы через пять различных подстратегий:

-

Стратегия MACD: Использует пересечение линии MACD и сигнальной линии для определения направления тренда. Когда линия MACD пересекает сигнальную линию снизу вверх — сигнал на покупку, сверху вниз — на продажу.

-

Стратегия Stochastic RSI: Сочетает преимущества RSI и стохастического осциллятора для мониторинга зон перекупленности/перепроданности. Когда Stochastic RSI опускается ниже заданного порога перепроданности — сигнал на покупку, выше порога перекупленности — на продажу.

-

Стратегия EMA для перекупленности/перепроданности: Использует EMA для выявления отклонения цены от среднего значения. Когда RSI ниже порога перепроданности — сигнал на покупку, выше порога перекупленности — на продажу.

-

Стратегия SuperTrend: Строит ценовые каналы на основе множителя ATR и определяет направление торговли по изменению тренда. Когда SuperTrend меняет знак с минуса на плюс — сигнал на покупку, с плюса на минус — на продажу.

-

Стратегия пересечения скользящих средних: Использует пересечение двух скользящих средних с разными периодами для определения тренда. Когда короткая скользящая средняя пересекает длинную снизу вверх — сигнал на покупку, сверху вниз — на продажу.

Стратегия взвешивает сигналы каждой подстратегии через настраиваемую систему весов; сделка срабатывает только когда взвешенная сумма превышает заданный порог. Кроме того, стратегия включает механизм распознавания потенциальных вершин и оснований, позволяющий корректировать позиции при возможных разворотах рынка.

Такая многоуровневая система подтверждения сигналов эффективно снижает количество ложных сигналов, повышая надёжность системы, а гибкие настройки параметров позволяют адаптироваться к различным торговым инструментам и таймфреймам.

Преимущества стратегии

-

Множественное подтверждение сигналов: Сигналы пяти независимых технических индикаторов взвешиваются, что снижает вероятность вводящих в заблуждение показателей одного индикатора и повышает качество и надёжность торговых сигналов.

-

Адаптивная система весов: Каждая подстратегия может иметь собственный вес, что позволяет трейдеру корректировать акценты в зависимости от уверенности в том или ином индикаторе и исторической эффективности, повышая гибкость стратегии.

-

Развитое управление рисками: Стратегия включает многоуровневые механизмы контроля рисков: стоп-лосс, многоуровневый тейк-профит и динамическое смещение стоп-лосса для быстрого ограничения убытков при неблагоприятных движениях рынка.

-

Автоматическое распознавание потенциальных вершин и оснований: Благодаря комплексному анализу RSI, объёма и ценового движения стратегия способна выявлять потенциальные вершины и основания рынка и частично закрывать позиции в подходящий момент для фиксации прибыли или сокращения убытков.

-

Высокая настраиваемость: Практически все параметры поддаются регулировке: периоды расчёта индикаторов, веса, проценты тейк-профита и стоп-лосса и т.д., что позволяет трейдеру оптимизировать стратегию под свой стиль и различные рыночные условия.

-

Встроенный механизм задержки: Чтобы избежать преждевременного входа в сделку или торговли на шумовых сигналах, стратегия использует механизм подтверждения с задержкой, гарантируя, что сделка происходит только при устойчивом сигнале, снижая влияние краткосрочных колебаний.

-

Фильтр по времени: Стратегия позволяет задавать даты начала и окончания торговли, что даёт возможность тестировать эффективность на исторических данных за определённые периоды или избегать периодов известных рыночных аномалий.

Риски стратегии

-

Риск переоптимизации параметров: Из-за большого числа параметров существует риск подгонки под исторические данные, что может привести к плохим результатам в реальной торговле. Решение: тестировать на нескольких таймфреймах и инструментах, использовать относительно устойчивые параметры, избегая чрезмерной оптимизации под конкретные исторические данные.

-

Риск изменения рыночных условий: Эффективность стратегии может различаться на трендовых и флэтовых рынках; внезапное изменение рыночного состояния может снизить результативность. Решение: внедрить механизм определения рыночной среды с корректировкой параметров или приостановкой торговли в зависимости от состояния.

-

Риск конфликта сигналов: Использование нескольких индикаторов одновременно может порождать противоречащие друг другу сигналы, вызывая путаницу в решениях. Решение: разумно назначать веса, делая акцент на более надёжных индикаторах, и устанавливать пороги сигналов таким образом, чтобы снизить вероятность конфликтов.

-

Риск неверного управления капиталом: Несмотря на наличие стоп-лосса, неправильное управление капиталом может привести к быстрому истощению средств. Решение: строго контролировать долю капитала на одну сделку, чтобы максимальный риск на сделку был в пределах допустимого.

-

Риск технических сбоев: Автоматизированные торговые системы могут столкнуться с проблемами сети, задержками данных и т.п. Решение: предусмотреть механизм ручного вмешательства, регулярно мониторить состояние системы и своевременно обрабатывать нештатные ситуации.

Направления оптимизации

-

Добавление фильтра рыночной среды: Разработать индикатор, определяющий, является ли рынок трендовым или флэтовым, и динамически корректировать веса подстратегий: усиливать трендовые стратегии на трендовом рынке, ослаблять — на флэтовом, где предпочтительнее осцилляторные.

-

Внедрение машинного обучения: Использовать машинное обучение для автоматической настройки параметров и весов индикаторов, чтобы стратегия постоянно обучалась и адаптировалась к последним рыночным данным, повышая динамическую приспособляемость.

-

Добавление анализа объёма торгов: Использовать изменения объёма как дополнительный сигнал подтверждения; совершать сделки только при поддержке объёмов, соответствующих ожиданиям, повышая достоверность сигналов.

-

Оптимизация алгоритма распознавания вершин и оснований: Улучшить существующую логику, добавив больше подтверждающих факторов, таких как ценовые паттерны, многотаймфреймовое подтверждение и т.д., для повышения точности.

-

Добавление индикаторов настроений: Интегрировать рыночные индикаторы настроений, такие как индекс страха (VIX), соотношение опционов колл/пут и т.п. При экстремальных настроениях корректировать стратегию или приостанавливать торговлю, чтобы избежать избыточной активности в периоды высокой волатильности.

-

Разработка динамического тейк-профита и стоп-лосса: Автоматически корректировать уровни тейк-профита и стоп-лосса в зависимости от рыночной волатильности: расширять стоп на высоковолатильных рынках, сужать на низковолатильных, делая управление рисками более гибким и эффективным.

-

Оптимизация по таймфреймам: Добавить анализ на нескольких таймфреймах, требовать подтверждения сигналов как на старшем, так и на младшем таймфреймах для снижения числа ложных пробоев и ложных сигналов.

Заключение

Мультииндикаторная взвешенная интеллектуальная торговая стратегия объединяет различные инструменты технического анализа с присвоением весов, создавая комплексную и гибкую торговую систему. Стратегия обладает множественным подтверждением сигналов, адаптивной системой весов и развитым управлением рисками, а также включает автоматическое распознавание потенциальных вершин и оснований, что обеспечивает высокую адаптивность в сложных и изменчивых рыночных условиях.

Несмотря на потенциальные риски, такие как переоптимизация параметров, изменение рыночных условий и конфликты сигналов, они могут быть эффективно контролируемы с помощью разумной настройки параметров, идентификации рыночной среды и строгого управления капиталом. Будущие направления оптимизации включают добавление фильтра рыночной среды, внедрение машинного обучения, усиление анализа объёмов и улучшение алгоритма распознавания вершин и оснований. Эти улучшения ещё больше повысят стабильность и прибыльность стратегии.

Для инвесторов, ищущих систематизированный подход к трейдингу, данная мультииндикаторная взвешенная стратегия предлагает достойный внимания фреймворк, который не только снижает влияние эмоций на торговые решения, но и позволяет непрерывно оптимизировать результаты на основе данных. При внедрении стратегии рекомендуется начинать с консервативных настроек, постепенно корректировать их и тщательно отслеживать производительность, чтобы найти наилучшую конфигурацию, соответствующую личной толерантности к риску и рыночным условиям.

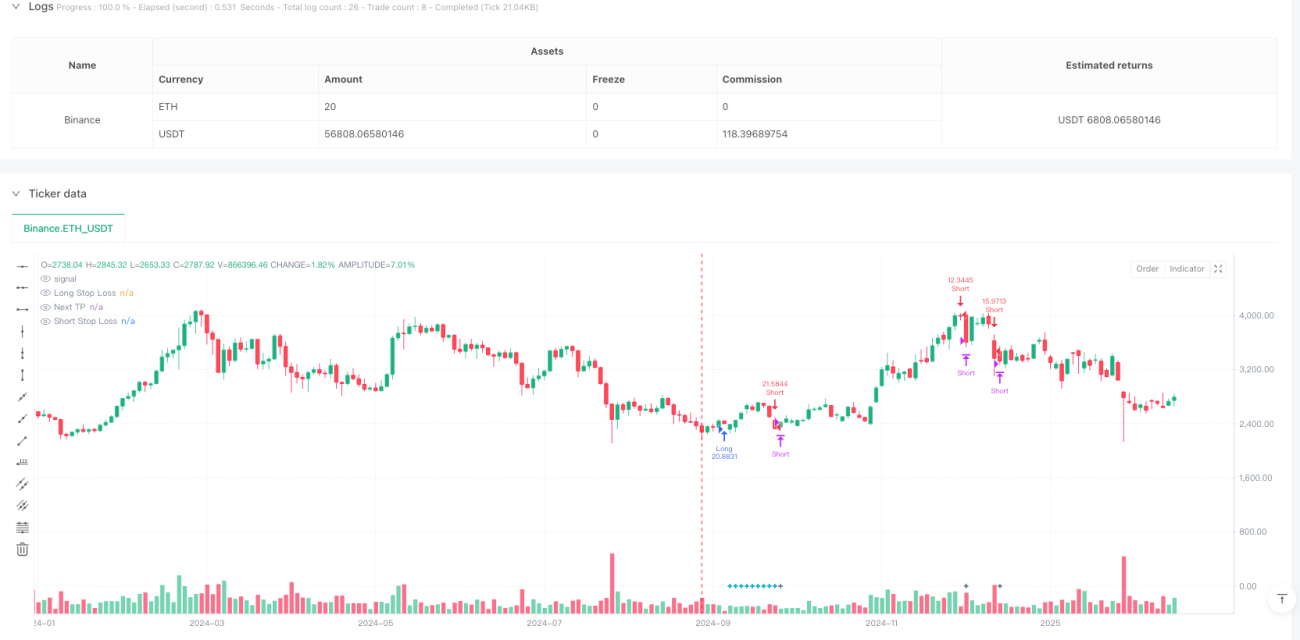

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1