Стратегия множителя параметров: рыночный метроном с интеграцией множества индикаторов

🎯 Что это за волшебная стратегия?

Знаете что? Эта стратегия – как установить на рынок «суперрадар»! Она не просто смотрит на один-два индикатора, а объединяет 9 различных технических индикаторов, словно оркестр, где каждый индикатор – это «инструмент». Только когда они звучат в гармонии, стратегия подаёт торговый сигнал. Представьте, как будто 9 экспертов дают вам советы одновременно, и вы действуете, только когда большинство из них согласны!

📊 Раскрываем основной принцип

Важно! Суть стратегии кроется в концепции «мультипликатора параметров». Она стандартизирует такие индикаторы, как RSI, ADX, Momentum, Rate of Change, ATR, Volume, Acceleration и Slope, приводя их к единой шкале, а затем перемножает для получения «комплексного значения силы». Как в кулинарии: у каждой приправы есть идеальная пропорция, и стратегия помогает найти идеальное сочетание всех рыночных «ингредиентов»! Когда комплексное значение силы пересекает свою скользящую среднюю – это идеальный момент для входа.

🔧 Настраиваемый инструмент для торговли

Что в этой стратегии самое крутое? Вы можете свободно комбинировать её как конструктор! Не нужен какой-то индикатор? Просто отключите его. Хотите изменить период настройки? Как вам угодно. К тому же есть фильтр тренда SMA, помогающий избежать ловушек контртрендовой торговли. Это как «набор инструментов DIY для торговых стратегий», позволяющий адаптировать конфигурацию под разные рыночные условия.

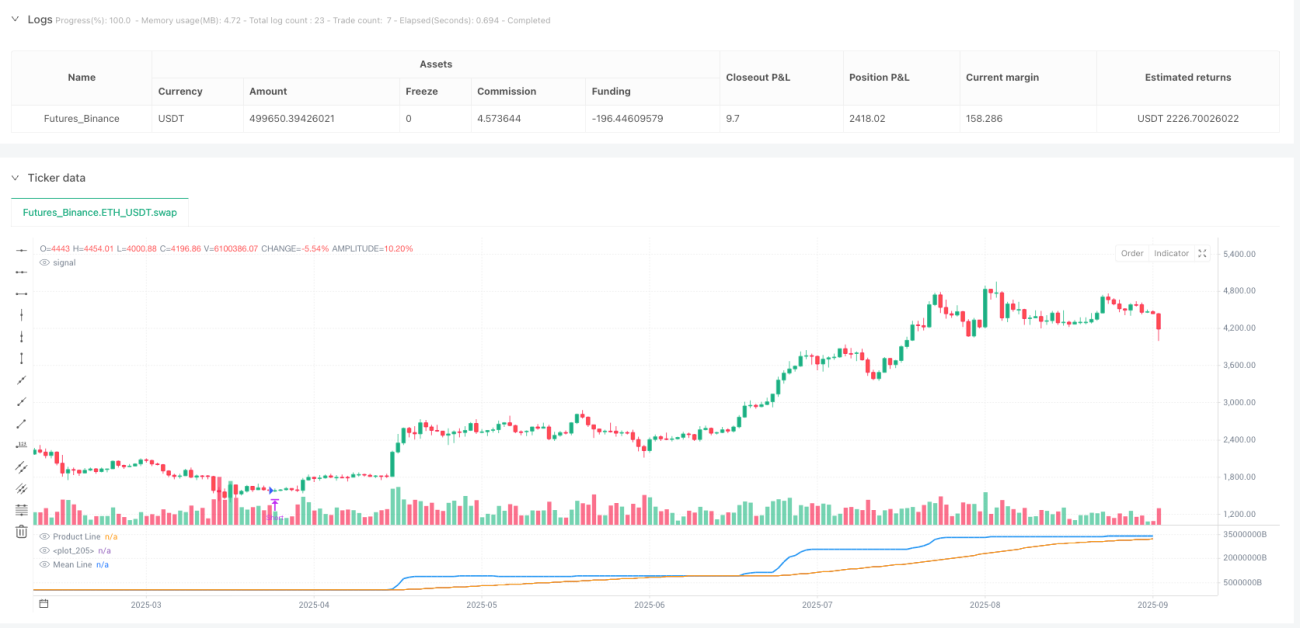

⚡ Практическое руководство по применению

Внимание, советы по избеганию ошибок! Эта стратегия особенно хороша на рынках, сочетающих флэт и тренд. Когда синяя линия продукта пересекает оранжевую скользящую среднюю вверх – открываем длинную позицию, при пересечении вниз – короткую. Стратегия также предусматривает автоматическое закрытие позиции, чтобы вы не оставались в сделке при появлении противоположного сигнала. Помните: включение фильтра тренда позволит уверенно торговать в направлении большого тренда, а его отключение – ловить больше краткосрочных возможностей!

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1