🎯 Что это за волшебная стратегия? 20 индикаторов работают вместе!

Знаете ли вы? Эта стратегия подобна суперумному AI-ассистенту для вашей торговли! Она одновременно отслеживает 20 различных рыночных сигналов и даёт торговые рекомендации только тогда, когда большинство индикаторов говорят «можно». Как при покупке дома: смотришь на расположение, цену, планировку, транспорт... и только когда всё устраивает, принимаешь решение!

Важный момент! Это не обычная стратегия с одним индикатором, а «многомерная резонансная система». Представьте: если только один друг скажет, что акции хороши, вы можете сомневаться; но если 20 профессионалов единодушны — уверенность возрастает, не так ли?

📊 Раскрываем основное оружие

Три меча определения тренда 🗡️

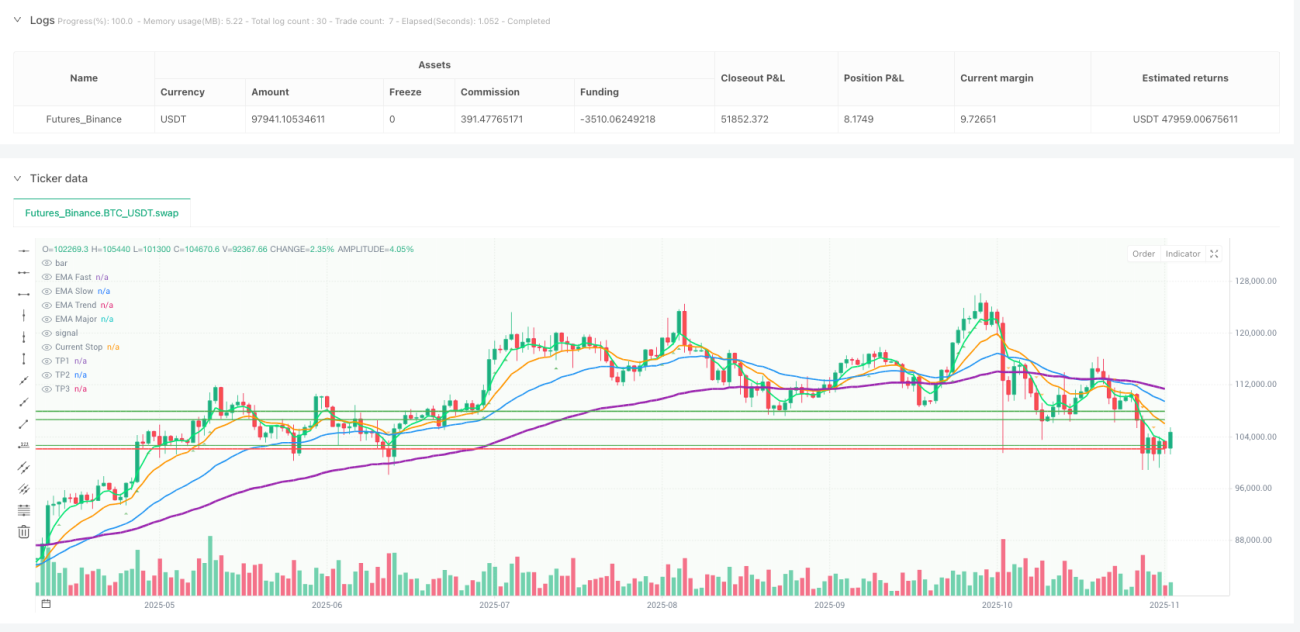

- Быстрая EMA(5) vs медленная EMA(13): улавливают краткосрочные развороты

- Фильтрующая EMA(34): подтверждает среднесрочное направление

- Главная EMA(89): определяет глобальный тренд, не отвлекаясь на мелкие колебания

Мультивременной анализ ⏰

Эта функция потрясающая! Стратегия одновременно смотрит на 1-часовой и 4-часовой тренды, как водитель, который видит и дорогу перед собой, и общий маршрут навигатора. Это позволяет избежать неловкой ситуации, когда «на малом таймфрейме тренд вверх, а на большом — вниз»!

Умное управление рисками 🛡️

- Динамическая корректировка размера позиции: автоматически меняет объём сделки в зависимости от волатильности рынка

- Частичная фиксация прибыли: не жадничать, забирать часть при хорошем раскладе

- Трейлинг-стоп: мощный инструмент защиты прибыли

🔥 Логика 20-кратной страховки

Сигнал на покупку требует:

- Тренд вверх: все EMA выстроены в бычьем порядке

- Достаточный импульс: RSI, MACD, стохастический RSI дают зелёный свет

- Подтверждение объёмов: рост на увеличении объёма — настоящий рост

- Здоровая структура рынка: последовательное повышение максимумов

- Поддержка ликвидности: ключевые уровни поддержки не нарушены

Сигнал на продажу — полная противоположность!

Руководство по избеганию ловушек ⚠️: стратегия также включает «детектор сжатия полос Боллинджера». Когда рынок слишком спокоен, сделки приостанавливаются, чтобы не попасть в ловушку боковика!

💰 Секретное оружие максимизации прибыли

Стратегия частичной фиксации прибыли 📈

- Первая фиксация: при соотношении риск/прибыль 1:2 продаём 30% позиции

- Вторая фиксация: при 3,5× ещё 40% позиции

- Оставшаяся часть: защищается трейлинг-стопом, давая прибыли расти

Улучшенный стоп-лосс 🎯

После достижения 2,5× прибыли стоп-лосс автоматически перемещается на уровень безубытка, гарантируя, что эта сделка хотя бы не принесёт убытка. Это как страховка вашей прибыли!

Динамический трейлинг-стоп 🏃♂️

Когда прибыль достигает определённого уровня, стоп-лосс следует за ценой как тень, защищая прибыль и оставляя пространство для роста.

🚀 Почему эта стратегия так эффективна?

- Всестороннее покрытие: технический анализ, управление капиталом, контроль рисков — всё в одном

- Умная фильтрация: 20 условий многоступенчатого отбора значительно повышают вероятность успеха

- Высокая адаптивность: мультивременной анализ подходит для разных рыночных условий

- Человеко-ориентированный дизайн: автоматическое исполнение исключает эмоциональные решения

Эта стратегия словно воплощает в коде команду опытных трейдеров, которая 24/7 ищет для вас лучшие торговые возможности!

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1