Chiến lược theo dõi xu hướng thích ứng dựa trên hồi quy hạt nhân và dải động ATR

Tổng quan

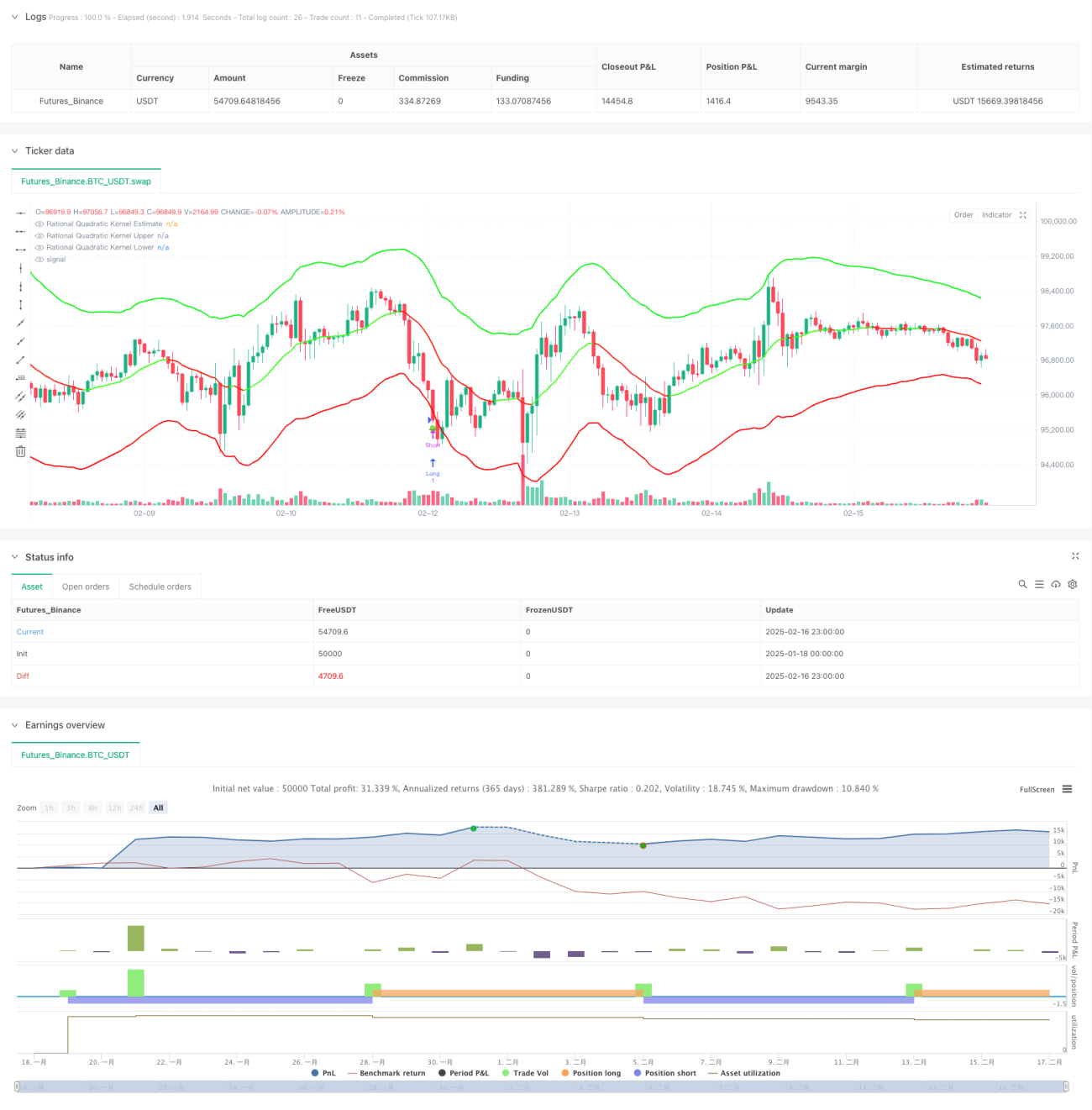

Chiến lược này là một hệ thống theo dõi xu hướng thích ứng kết hợp hồi quy hạt nhân Nadaraya-Watson và dải động ATR. Nó dự đoán xu hướng giá thông qua hàm hạt nhân bậc hai hợp lý và sử dụng các dải hỗ trợ/kháng cự động dựa trên ATR để xác định cơ hội giao dịch. Hệ thống mô hình hóa thị trường chính xác thông qua cửa sổ nhìn lại và tham số trọng số có thể cấu hình.

Nguyên lý chiến lược

Cốt lõi của chiến lược là hồi quy hạt nhân phi tham số dựa trên phương pháp Nadaraya-Watson, sử dụng hàm hạt nhân bậc hai hợp lý để làm mịn chuỗi giá. Hồi quy được tính từ thanh bắt đầu đã đặt, kiểm soát mức độ phù hợp thông qua hai tham số chính: cửa sổ nhìn lại (h) và trọng số tương đối (r). Đồng thời kết hợp chỉ báo ATR để xây dựng dải động, dải trên và dải dưới lần lượt là ước tính hồi quy cộng/trừ bội số của ATR. Hệ thống kích hoạt tín hiệu giao dịch khi giá cắt qua các dải - khi giá phá vỡ dải dưới thì mua lên, phá vỡ dải trên thì bán xuống. Đánh giá xu hướng có thể dựa trên tỷ lệ thay đổi giá hoặc cơ chế giao cắt, và được hiển thị trực quan qua sự thay đổi màu sắc.

Ưu điểm chiến lược

- Phương pháp hồi quy hạt nhân có nền tảng toán học vững chắc, có thể nắm bắt xu hướng giá hiệu quả mà không quá phù hợp.

- Các dải động tự điều chỉnh theo biến động thị trường, cung cấp các mức hỗ trợ/kháng cự hợp lý hơn.

- Khả năng cấu hình tham số cao, có thể điều chỉnh linh hoạt theo đặc điểm thị trường khác nhau.

- Cơ chế nhận dạng xu hướng linh hoạt, có thể chọn chế độ mượt hoặc nhạy.

- Hiệu ứng trực quan trực giác, tín hiệu giao dịch rõ ràng.

Rủi ro chiến lược

- Lựa chọn tham số không phù hợp có thể dẫn đến quá phù hợp hoặc độ trễ.

- Trong thị trường đi ngang có thể tạo ra quá nhiều tín hiệu giao dịch.

- Cài đặt bội số ATR không hợp lý có thể dẫn đến stop loss quá rộng hoặc quá hẹp.

- Trong giai đoạn chuyển đổi xu hướng có thể xuất hiện tín hiệu giả.

Khuyến nghị tối ưu hóa tham số thông qua backtest lịch sử và kết hợp các chỉ báo khác để xác nhận hỗ trợ.

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo khối lượng làm xác nhận xu hướng.

- Phát triển cơ chế tối ưu hóa tham số thích ứng.

- Thêm bộ lọc cường độ xu hướng để giảm tín hiệu giả trong thị trường đi ngang.

- Tối ưu hóa cơ chế stop loss/take profit để cải thiện tỷ lệ lợi nhuận/rủi ro.

- Xem xét thêm phân loại môi trường thị trường, áp dụng tham số khác nhau trong các thị trường khác nhau.

Tổng kết

Chiến lược này kết hợp các phương pháp học thống kê với phân tích kỹ thuật, xây dựng một hệ thống giao dịch có nền tảng lý thuyết vững chắc và tính thực tiễn cao. Tính thích ứng và khả năng cấu hình của nó cho phép thích nghi với các môi trường thị trường khác nhau, nhưng khi sử dụng cần chú ý tối ưu hóa tham số và kiểm soát rủi ro. Thông qua cải tiến và tối ưu hóa liên tục, chiến lược này hứa hẹn sẽ đóng vai trò quan trọng trong giao dịch thực tế.

- 1