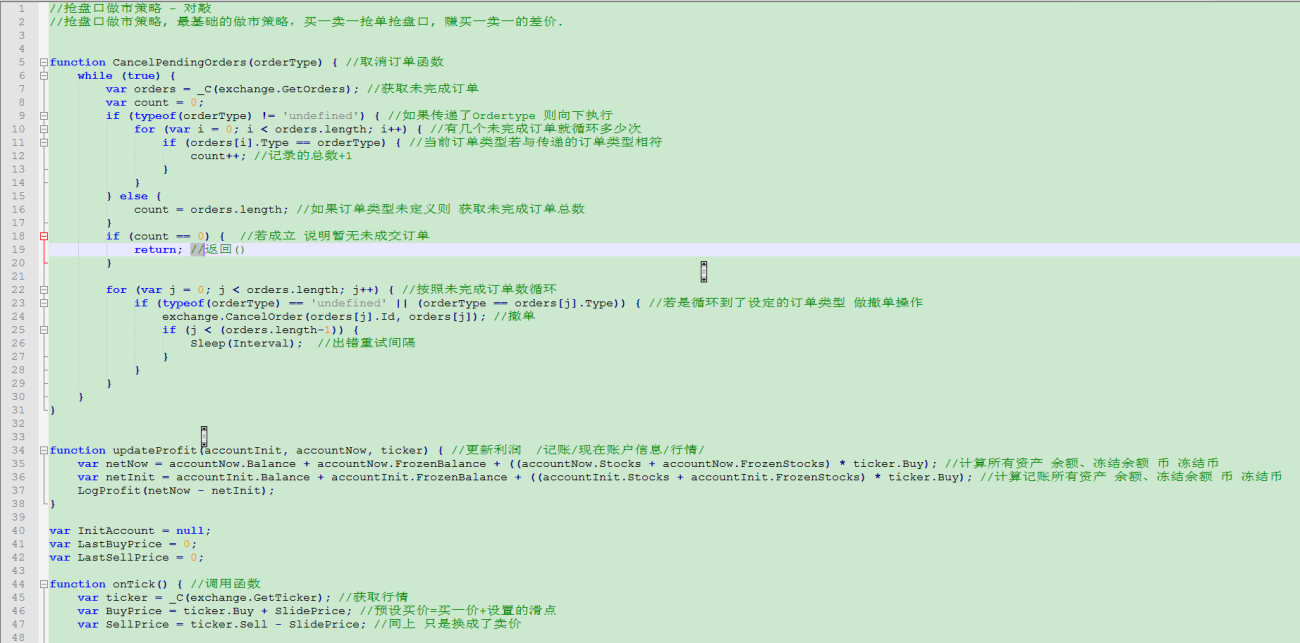

抢盘口做市策略, 最基础的做市策略,买一卖一抢单抢盘口, 赚买一卖一的差价.

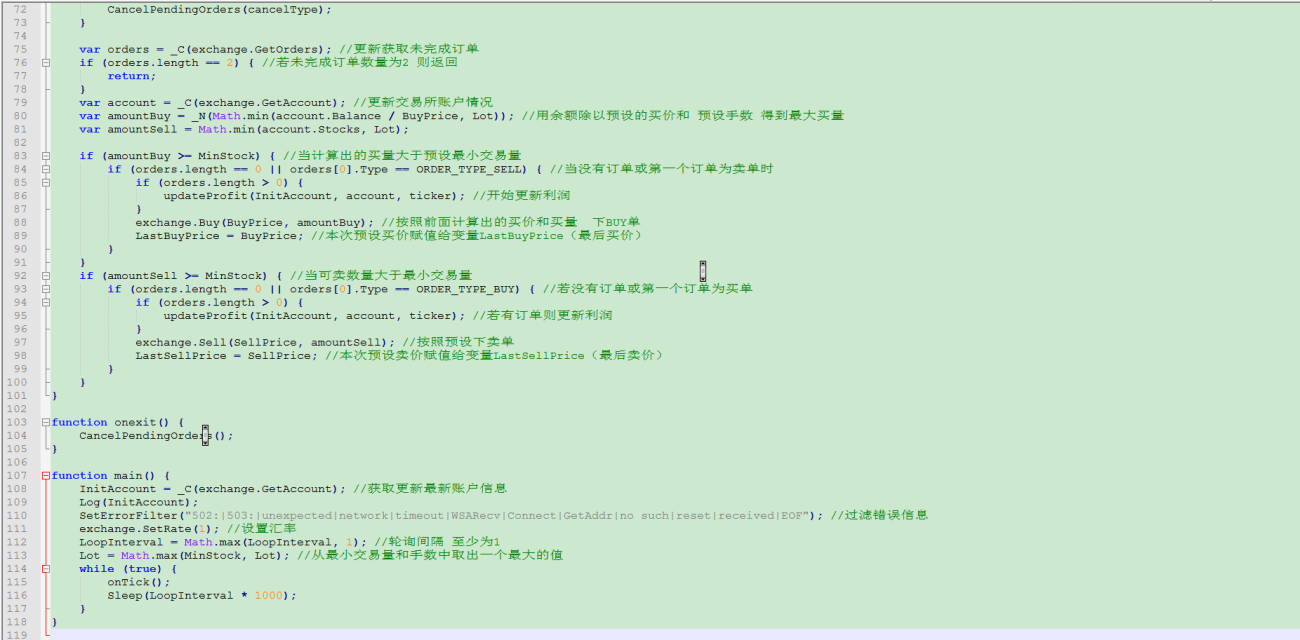

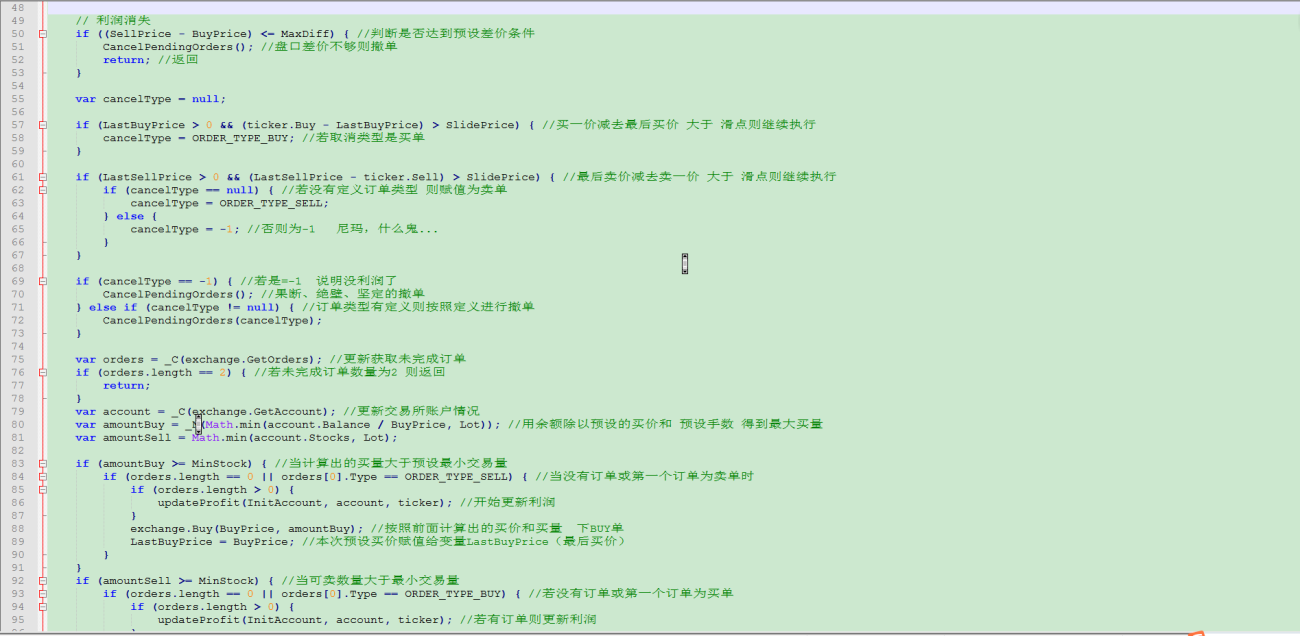

function CancelPendingOrders(orderType) { while (true) { var orders = _C(exchange.GetOrders); var count = 0; if (typeof(orderType) != 'undefined') { for (var i = 0; i < orders.length; i++) { if (orders[i].Type == orderType) { count++; } } } else {

怎么确定币种呢?

感谢分享,尽量在读,有些地方还是不太懂,做了些注释,谢谢分享。

感谢注释

if (orders.length == 0 || orders[0].Type == ORDER_TYPE_SELL) { 请问为什么需要对这个 orders[0].Type == ORDER_TYPE_SELL)进行判断啊?