Triple Supertrend with EMA and ADX

1

Follow

1789

Followers

Publishing a strategy that includes adx and ema filter as well

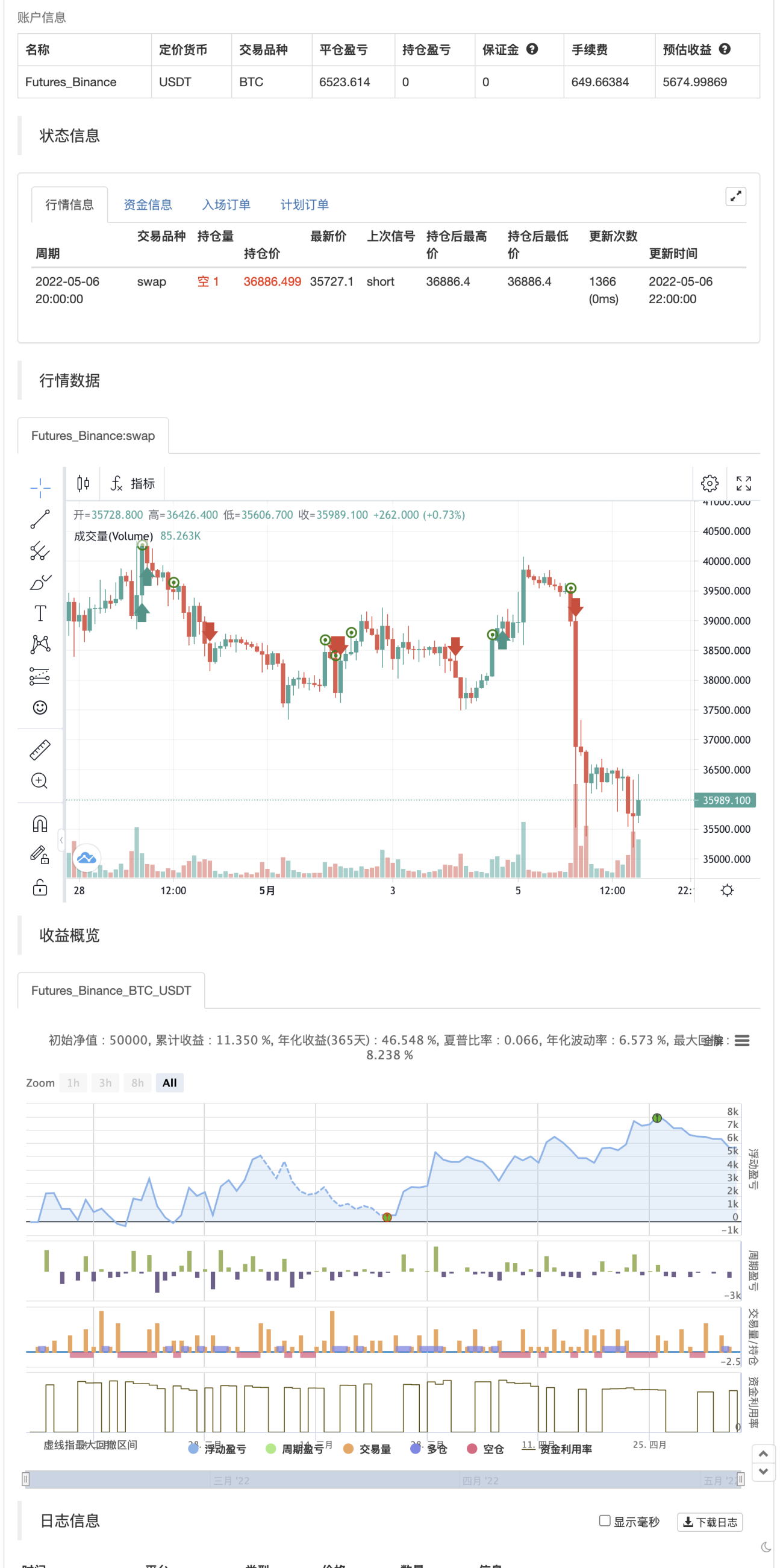

Entry: all three Supertrend turns positive. If a filter of ADX and EMA is applied, also check if ADX is above the selected level and close is above EMA

Exit: when the first supertrend turns negative

opposite for short entries

A FIlter is given to take or avoid re-enter on the same side. For example, After a long exit, if the entry condition is satisfied again for long before the short single is triggered it takes re-entry if selected.

backtest

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1