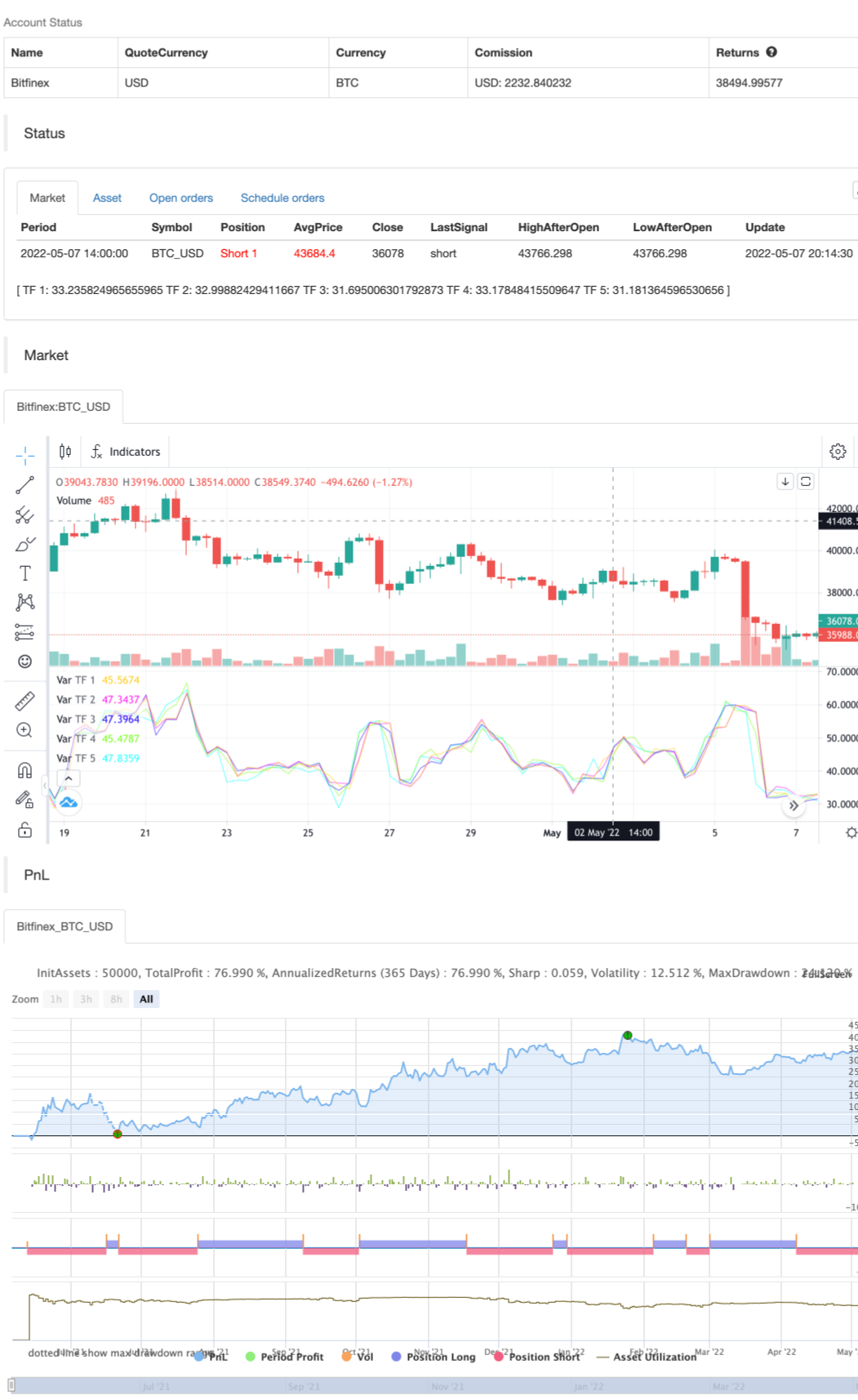

RSI MTF Ob+Os

12

Follow

657

Followers

Hello Traders,

This indicator use the same concept as my previous indicator "CCI MTF Ob+Os".

It is a simple "Relative Strength Index" ( RSI ) indicator with multi-timeframe (MTF) overbought and oversold level.

It can detect overbought and oversold level up to 5 timeframes, which help traders spot potential reversal point more easily.

There are options to select 1-5 timeframes to detect overbought and oversold.

Aqua Background is "Oversold" , looking for "Long".

Orange Background is "Overbought" , looking for "Short".

Have fun :)

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1