FTSMA - Trend is your frend

This my new solid strategy: if you belive that "TREND IS YOUR FRIEND" this is for you!

I have tested with many pairs and at many timeframes and have profit with just minor changes in settings.

I suggest to use it for intraday trading.

VERY IMPORTANT NOTE: this is a trend following strategy, so the target is to stay in the trade as much as possible. If your trading style is more focused on scalping and/or pullbaks, this strategy is not for you.

This strategy uses moving averages applied to Fourier waves for forecasting trend direction.

How strategy works:

- Buy when fast MA is above mid MA and price is above slow MA, which acts as a trend indicator.

- Sell when fast MA is below mid MA and price is below slow MA, which acts as a trend indicator.

Strategy uses a lot of pyramiding orders because when you are in a flat market phase it will close 1 or 2 orders with a loss, but when a big trend starts, it will have profit in a lot of orders.

So, if you analize carefully the strategy results, you will note that "Percent Profitable" is very low (30% in this case) because strategy opened a lot of orders also in flat markets with small losses, BUT "Avg # bars in winning trades" is very high and overall Profit is very high: when a big trend starts, orders are kept open for long time generating big profits.

Thanks to all pinescripters mentioned in the code for their snippets.

I have also a study with alerts. Next improvement (only to whom is interested to this script and follows me): study with alerts on multiple tickers all at one. Leave a comment if you want to have access to study.

HOW TO USE STRATEGY AND STUDY TOGHETER:

1- Add to chart the strategy first, so your workspace will be as clean as possible.

2- Open the Strategy Tester tab at footer of the page.

3- Modify settings to get best results (Profit, Profit Factor, Drawdown).

4- Add study with alerts to your chart with same setting of strategy.

I WILL PROVIDE A DETAILED QUICK INSTALLATION GUIDE WITH THE STUDY!

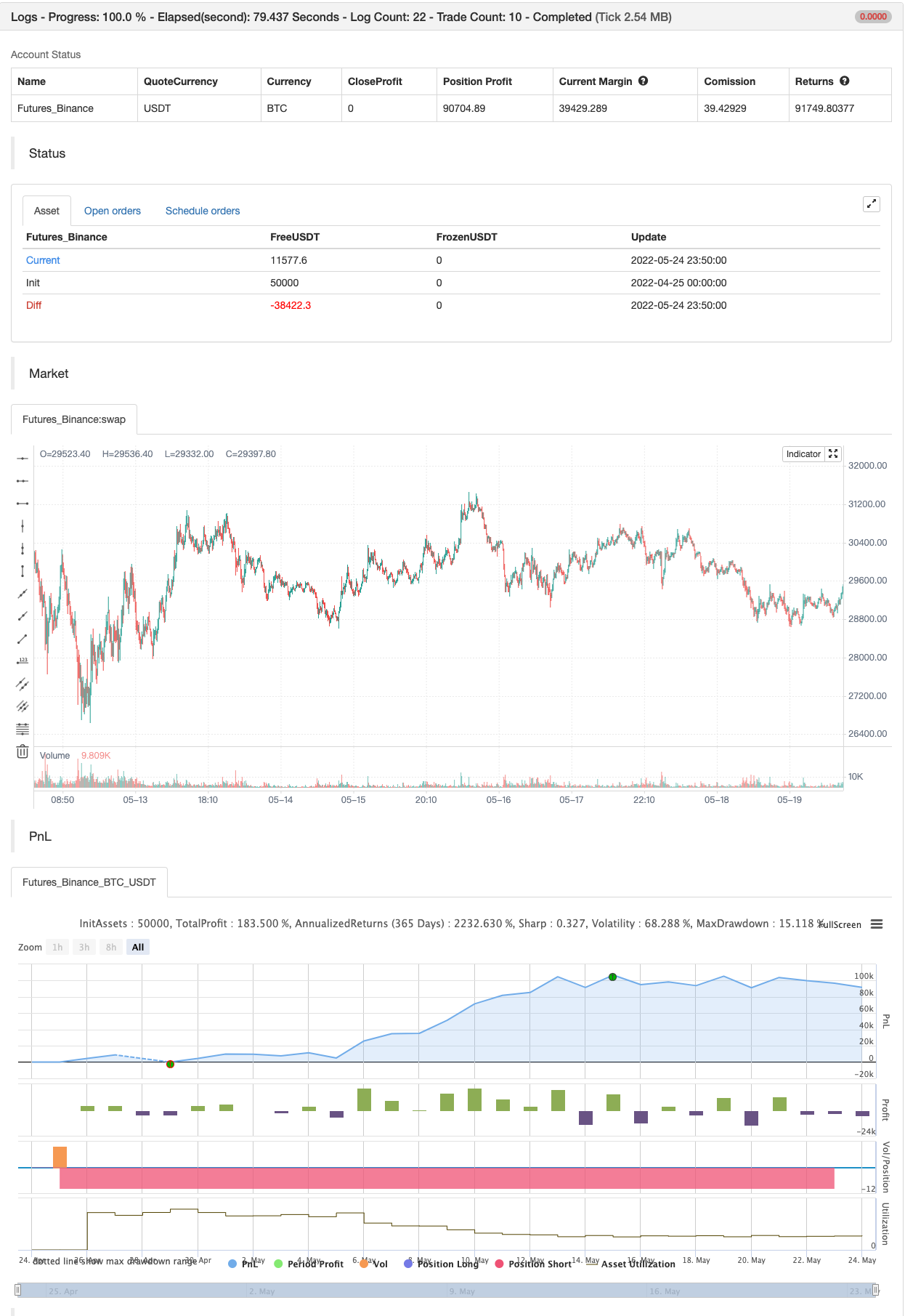

backtest

- 1