Overview

This strategy is a momentum trading system that combines multiple technical indicators while integrating a flexible take profit and stop loss mechanism. The strategy primarily uses crossover signals from three popular technical indicators - RSI, EMA, and MACD - to assess market trends and momentum for making trading decisions. It also incorporates percentage-based take profit and stop loss levels, as well as a risk-reward ratio concept to optimize money management and risk control.

Strategy Principles

The core principle of this strategy is to identify potential trading opportunities through the synergistic effect of multiple indicators. Specifically:

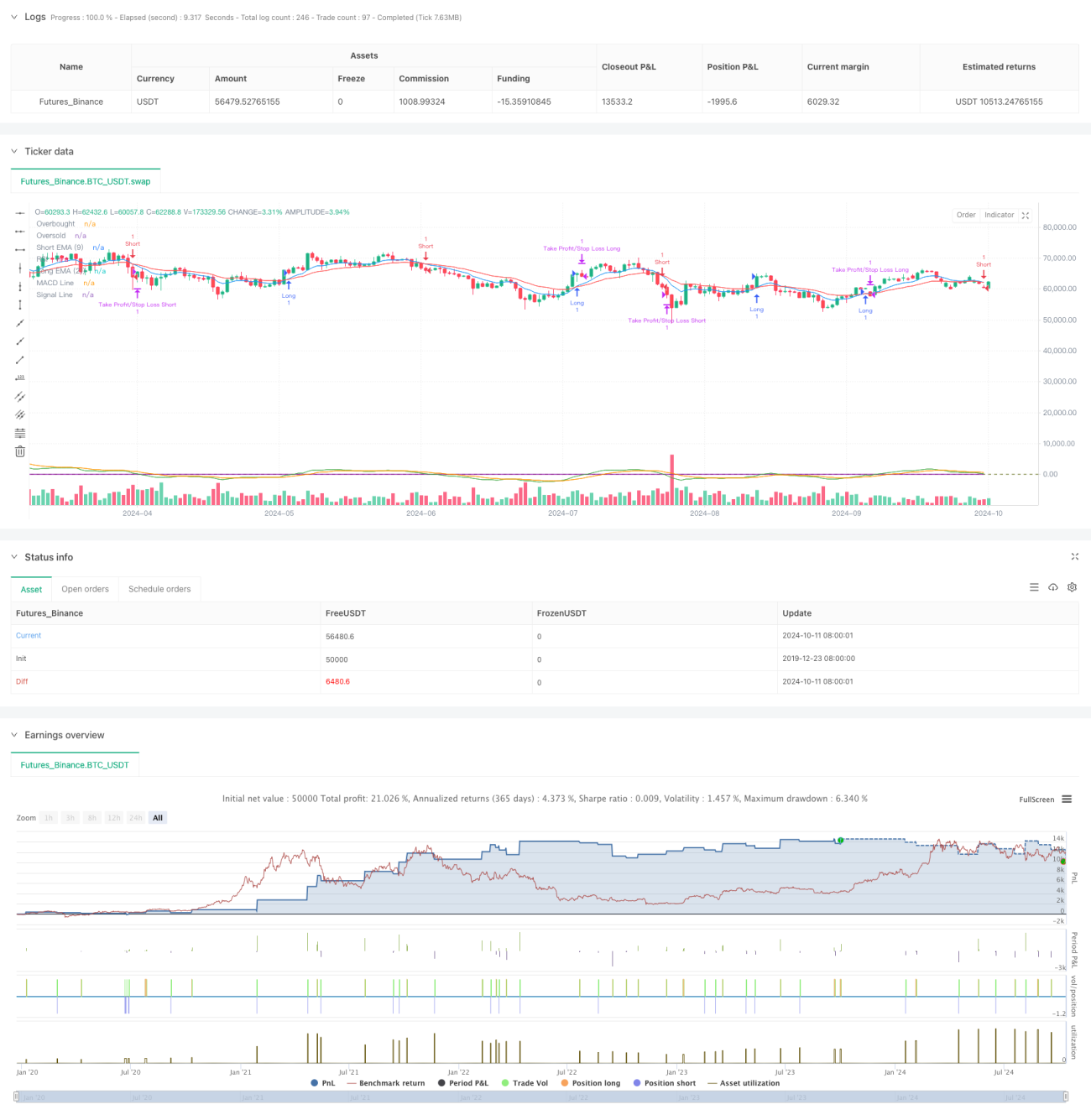

- It uses the RSI (Relative Strength Index) to determine if the market is in overbought or oversold conditions.

- It utilizes the crossover of short-term and long-term EMAs (Exponential Moving Averages) to confirm trend changes.

- It further verifies momentum through the relationship between the MACD (Moving Average Convergence Divergence) histogram and signal line.

The strategy triggers trading signals when these indicators simultaneously meet specific conditions. For example, a long signal is generated when the short-term EMA crosses above the long-term EMA, the RSI is below the overbought level, and the MACD histogram is above the signal line. Opposite conditions trigger short signals.

Additionally, the strategy incorporates a percentage-based take profit and stop loss mechanism, allowing traders to set appropriate profit targets and stop loss levels based on their risk preferences. The introduction of a risk-reward ratio further optimizes the money management strategy.

Strategy Advantages

- Multi-indicator synergy: By combining RSI, EMA, and MACD, the strategy can analyze the market from multiple perspectives, increasing the reliability of signals.

- Flexible money management: The percentage-based take profit and stop loss settings, along with the risk-reward ratio, allow the strategy to be adjusted according to different market environments and individual risk preferences.

- Trend following and momentum combination: EMA crossovers provide trend signals, while RSI and MACD supplement momentum factors, helping to capture strong market movements.

- Visual support: The strategy plots key indicators on the chart, facilitating intuitive understanding of market conditions and strategy logic.

- Adjustable parameters: The periods and thresholds of major indicators can be adjusted through input parameters, increasing the strategy's adaptability.

Strategy Risks

- Overtrading: In choppy markets, multiple indicators may frequently generate conflicting signals, leading to excessive trading.

- Lagging nature: All indicators used are essentially lagging indicators, which may not react timely in rapidly changing markets.

- False breakout risk: EMA crossover strategies are susceptible to market noise and may produce false breakout signals.

- Parameter sensitivity: The strategy's performance highly depends on the chosen parameters, which may require different settings for various market environments.

- Lack of market sentiment consideration: The strategy is primarily based on technical indicators and does not account for fundamental factors or market sentiment, potentially underperforming during significant news events.

Strategy Optimization Directions

- Introduce volatility filtering: Consider adding the ATR (Average True Range) indicator to reduce trading frequency in low volatility environments and improve signal quality.

- Add trend strength filtering: For example, use the ADX (Average Directional Index) to ensure trading only in strong trends, avoiding frequent trades in ranging markets.

- Dynamic take profit and stop loss: Adjust take profit and stop loss levels dynamically based on market volatility, such as using multiples of ATR.

- Time filtering: Add trading time window restrictions to avoid highly volatile opening and closing sessions.

- Incorporate volume analysis: Combine volume indicators like OBV (On-Balance Volume) or CMF (Chaikin Money Flow) to validate price movements.

- Machine learning optimization: Use machine learning algorithms to dynamically adjust and optimize strategy parameters to adapt to changing market environments.

Conclusion

This multi-indicator crossover momentum trading strategy provides traders with a comprehensive trading system by integrating RSI, EMA, and MACD technical indicators with a flexible take profit and stop loss mechanism. The strategy's strengths lie in its ability to analyze the market from multiple angles and its flexible risk management methods. However, like all trading strategies, it faces risks such as overtrading and parameter sensitivity. By introducing optimization directions such as volatility filtering, dynamic stop loss, and machine learning, the strategy has the potential to further improve its performance in various market environments. When using this strategy, traders need to carefully adjust parameters and combine market analysis with risk management principles to achieve optimal trading results.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-10-12 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Crypto Futures Day Trading with Profit/Limit/Loss", overlay=true, margin_long=100, margin_short=100)

// Parameters for the strategy- 1