Bull Bear Power Trading Strategy with Volume-Percentile Based Dynamic Take-Profit System

Overview

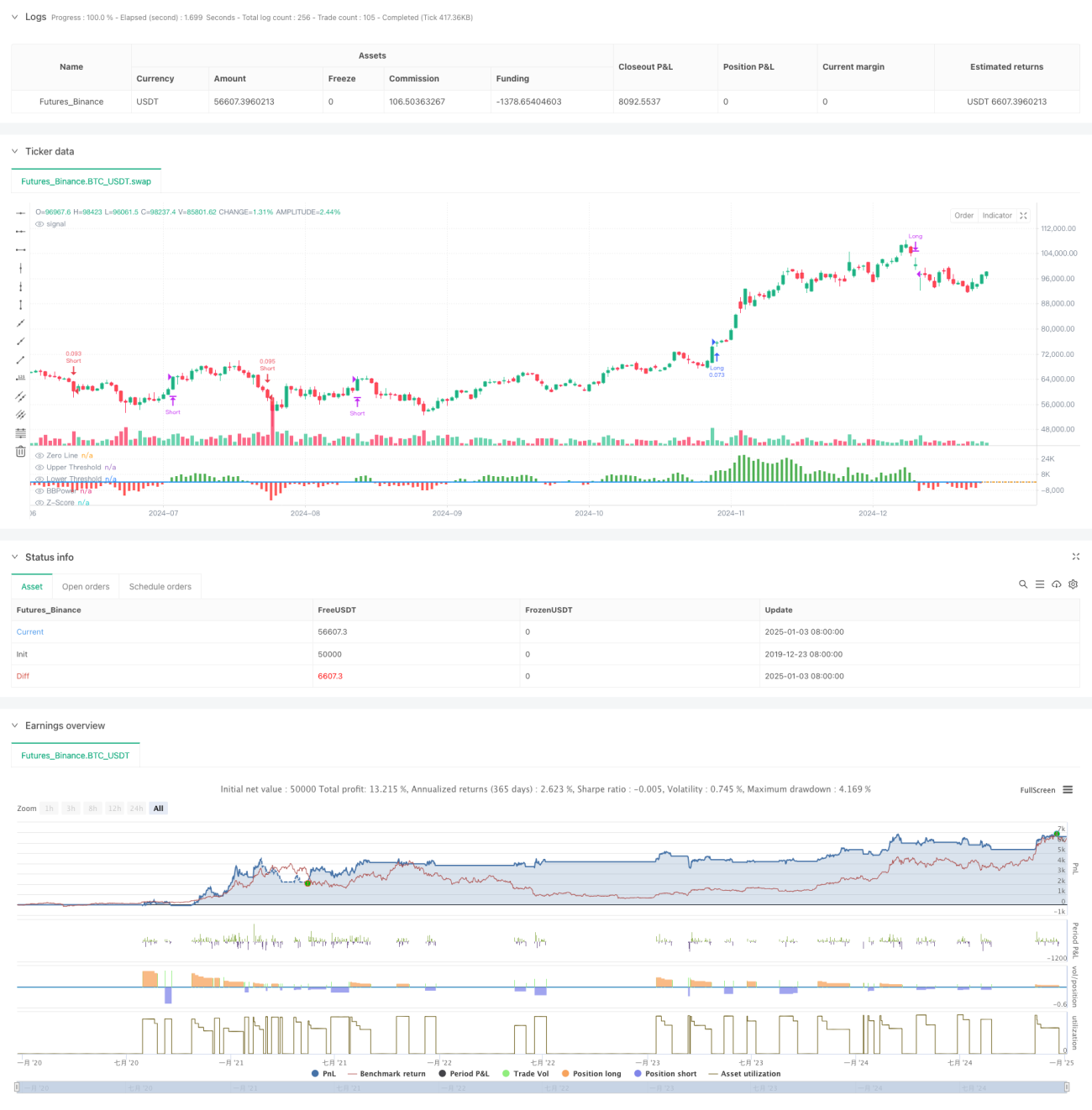

This strategy combines the Bull Bear Power (BBP) indicator with a multi-level dynamic take-profit system based on volume percentiles. It creates an adaptive and risk-controlled trading system through multi-dimensional analysis of price, volume, and momentum data. The core logic includes using the Z-Score normalized BBP values as trade signal triggers, while incorporating volume percentile analysis for dynamic take-profit adjustments.

Strategy Principles

The core calculations include several key components:

- BBP Indicator: Measures market force balance by summing the difference between high price and EMA (bull power) and low price and EMA (bear power).

- Z-Score Normalization: Standardizes BBP values to assess market strength deviation levels.

- Volume Analysis: Calculates current volume relative to moving average to gauge market activity.

- Percentile Analysis: Computes historical percentiles of price and volume for market state probability distribution.

- Dynamic Take-Profit: Adjusts take-profit levels based on composite scoring of ATR, volume percentile, and price percentile.

Strategy Advantages

- Multi-dimensional Analysis: Provides comprehensive market perspective through price momentum, volume, and market positioning.

- High Adaptability: Adapts to different market environments through dynamic take-profit mechanism.

- Risk Diversification: Implements multi-level take-profit strategy for profit realization at different price levels.

- Statistical Edge: Achieves significant advantage through Z-Score and percentile analysis.

- Extensibility: Framework allows easy addition of new analysis dimensions.

Strategy Risks

- Parameter Sensitivity: Multiple parameters require optimization for different market environments.

- Market Environment Dependency: May underperform during volatile periods or trend transitions.

- Execution Slippage: Multi-level take-profit orders may face execution slippage.

- Computational Complexity: Real-time calculation of multiple indicators may cause system load.

- False Signal Risk: May generate incorrect trading signals in ranging markets.

Optimization Directions

- Parameter Adaptation: Introduce machine learning methods for automatic parameter optimization.

- Market Prediction: Add market environment classification module for early identification of adverse conditions.

- Stop-Loss Optimization: Implement dynamic stop-loss mechanism for improved risk control.

- Signal Filtering: Add trend strength filters to reduce false signals.

- Position Management: Optimize position allocation algorithm for improved capital efficiency.

Summary

This strategy combines traditional BBP indicator with modern quantitative analysis methods to create a trading system with solid theoretical foundation and strong practicality. It achieves good balance between returns and risk through multi-level take-profit and dynamic adjustment mechanisms. While parameter optimization presents some challenges, the strategy framework's extensibility provides ample room for future improvements. In practical application, traders should make specific adjustments based on market characteristics and individual risk preferences.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability. - 1