Deribit期权Delta动态对冲策略

本次FMZ量化带来的策略是Deribit期权Delta动态对冲策略,简称DDH(dynamic delta hedging)策略。

对于期权交易的学习,我们通常要掌握这几个方面的概念:

-

期权定价模型,B-S模型,期权价格根据【标的物价格】、【行权价】、【到期剩余时间】、【(隐含)波动率】、【无风险利率】确定价格。

-

期权的风险敞口:

- Delta — 期权的方向风险。如果Delta为+0.50,那这个期权,在标的价格涨跌时的盈亏表现,可视为0.50个现货。

- Gamma — 方向风险的加速度。比如看涨期权,由于Gamma的作用,从标的价格位于行权价开始,价格不断上涨的过程中,Delta会从+0.50逐渐向+1.00靠拢。

- Theta— 时间敞口。当你买入期权时,如果标的价格不动,每过一天,你会支付Theta金额所示的费用(Deribit以USD计价)。

当你卖出期权时,如果标的价格不动,每过一天,你会收到Theta金额所示的费用。 - Vega — 波动率敞口。当你买入期权时,Vega为正,即做多波动率。隐含波动率提高时,你会在Vega敞口获得收益。反之亦然,当你卖出期权时,隐含波动率降低,你会获得收益。

DDH策略讲解:

-

DDH 原理讲解

通过配平期权和期货的Delta,达到交易方向的风险中性。由于期权的Delta是会跟随标的物价格变动而变动的,期货和现货的Delta是不变的。

在持有期权合约仓位,并用期货对冲配平Delta之后,随着标的物价格变动,总体Delta会再次出现不平衡的状态。对于期权仓位和期货仓位这样的组合就需要持续的动态对冲配平Delta。举个例子:

当我们买入了一张看涨期权,此时就持有了一个看多方向的头寸。此时需要做空期货来对冲期权的Delta,达到总体Delta中性(0或者接近于0)。

我们先不考虑期权合约到期剩余时间、波动率等因素。

情况1:

标的物价格上涨,期权部分的Delta增大,总体Delta向正数移动,需要期货再次对冲,开一部分空头仓继续做空期货,使总体Delta再次平衡。

(再次平衡前,此时期权的Delta大,期货的Delta相对小,看涨期权的边际盈利超过合约空头的边际损失,整个组合会出现收益)情况2:

标的物价格下跌,期权部分的Delta减小,总体Delta向负数移动,平仓一部分空头的期货持仓,使总体Delta再次平衡。

(再次平衡前,此时期权的Delta小,期货的Delta相对大,看涨期权的边际损失小于合约空头的边际盈利,整个组合还是会出现收益)所以理想状态,标的物涨跌都会带来收益,只要市场有波动即可。

然而还需要考虑的因素还有:时间价值、交易成本等因素。

所以引用知乎大牛的解释:

Gamma Scalping 的关注点并不是delta,dynamic delta hedging 只是过程中规避underlying价格风险的一种做法而已。 Gamma Scalping 关注的是Alpha,此Alpha不是选股的Alpha,这里的Alpha = Gamma/Theta也就是单位Theta的时间损耗换来多少Gamma, 这个是关注的点。可以构建出上涨和下跌都浮盈的组合,但一定伴随时间损耗,那问题就在于性价比了。 作者:许哲 链接:https://www.zhihu.com/question/51630805/answer/128096385

DDH 策略设计讲解

- 聚合行情接口封装,框架设计

- 策略UI设计

- 策略交互设计

- 自动对冲功能设计

源码:

javascript

// 构造函数

function createManager(e, subscribeList, msg) {

var self = {}

self.supportList = ["Futures_Binance", "Huobi", "Futures_Deribit"] // 支持的交易所的

// 对象属性

self.e = e

self.msg = msg

self.name = e.GetName()

self.type = self.name.includes("Futures_") ? "Futures" : "Spot"

self.label = e.GetLabel()

self.quoteCurrency = ""

self.subscribeList = subscribeList // subscribeList : [strSymbol1, strSymbol2, ...]

self.tickers = [] // 接口获取的所有行情数据,定义数据格式:{bid1: 123, ask1: 123, symbol: "xxx"}}

self.subscribeTickers = [] // 需要的行情数据,定义数据格式:{bid1: 123, ask1: 123, symbol: "xxx"}}

self.accData = null

self.pos = null

// 初始化函数

self.init = function() {

// 判断是否支持该交易所

if (!_.contains(self.supportList, self.name)) {

throw "not support"

}

}

self.setBase = function(base) {

// 切换基地址,用于切换为模拟盘

self.e.SetBase(base)

Log(self.name, self.label, "切换为模拟盘:", base)

}

// 判断数据精度

self.judgePrecision = function (p) {

var arr = p.toString().split(".")

if (arr.length != 2) {

if (arr.length == 1) {

return 0

}

throw "judgePrecision error, p:" + String(p)

}

return arr[1].length

}

// 更新资产

self.updateAcc = function(callBackFuncGetAcc) {

var ret = callBackFuncGetAcc(self)

if (!ret) {

return false

}

self.accData = ret

return true

}

// 更新持仓

self.updatePos = function(httpMethod, url, params) {

var pos = self.e.IO("api", httpMethod, url, params)

var ret = []

if (!pos) {

return false

} else {

// 整理数据

// {"jsonrpc":"2.0","result":[],"usIn":1616484238870404,"usOut":1616484238870970,"usDiff":566,"testnet":true}

try {

_.each(pos.result, function(ele) {

ret.push(ele)

})

} catch(err) {

Log("错误:", err)

return false

}

self.pos = ret

}

return true

}

// 更新行情数据

self.updateTicker = function(url, callBackFuncGetArr, callBackFuncGetTicker) {

var tickers = []

var subscribeTickers = []

var ret = self.httpQuery(url)

if (!ret) {

return false

}

// Log("测试", ret)// 测试

try {

_.each(callBackFuncGetArr(ret), function(ele) {

var ticker = callBackFuncGetTicker(ele)

tickers.push(ticker)

if (self.subscribeList.length == 0) {

subscribeTickers.push(ticker)

} else {

for (var i = 0 ; i < self.subscribeList.length ; i++) {

if (self.subscribeList[i] == ticker.symbol) {

subscribeTickers.push(ticker)

}

}

}

})

} catch(err) {

Log("错误:", err)

return false

}

self.tickers = tickers

self.subscribeTickers = subscribeTickers

return true

}

self.getTicker = function(symbol) {

var ret = null

_.each(self.subscribeTickers, function(ticker) {

if (ticker.symbol == symbol) {

ret = ticker

}

})

return ret

}

self.httpQuery = function(url) {

var ret = null

try {

var retHttpQuery = HttpQuery(url)

ret = JSON.parse(retHttpQuery)

} catch (err) {

// Log("错误:", err)

ret = null

}

return ret

}

self.returnTickersTbl = function() {

var tickersTbl = {

type : "table",

title : "tickers",

cols : ["symbol", "ask1", "bid1"],

rows : []

}

_.each(self.subscribeTickers, function(ticker) {

tickersTbl.rows.push([ticker.symbol, ticker.ask1, ticker.bid1])

})

return tickersTbl

}

// 返回持仓表格

self.returnPosTbl = function() {

var posTbl = {

type : "table",

title : "pos|" + self.msg,

cols : ["instrument_name", "mark_price", "direction", "size", "delta", "index_price", "average_price", "settlement_price", "average_price_usd", "total_profit_loss"],

rows : []

}

/* 接口返回的持仓数据格式

{

"mark_price":0.1401105,"maintenance_margin":0,"instrument_name":"BTC-25JUN21-28000-P","direction":"buy",

"vega":5.66031,"total_profit_loss":0.01226105,"size":0.1,"realized_profit_loss":0,"delta":-0.01166,"kind":"option",

"initial_margin":0,"index_price":54151.77,"floating_profit_loss_usd":664,"floating_profit_loss":0.000035976,

"average_price_usd":947.22,"average_price":0.0175,"theta":-7.39514,"settlement_price":0.13975074,"open_orders_margin":0,"gamma":0

}

*/

_.each(self.pos, function(ele) {

if(ele.direction != "zero") {

posTbl.rows.push([ele.instrument_name, ele.mark_price, ele.direction, ele.size, ele.delta, ele.index_price, ele.average_price, ele.settlement_price, ele.average_price_usd, ele.total_profit_loss])

}

})

return posTbl

}

self.returnOptionTickersTbls = function() {

var arr = []

var arrDeliveryDate = []

_.each(self.subscribeTickers, function(ticker) {

if (self.name == "Futures_Deribit") {

var arrInstrument_name = ticker.symbol.split("-")

var currency = arrInstrument_name[0]

var deliveryDate = arrInstrument_name[1]

var deliveryPrice = arrInstrument_name[2]

var optionType = arrInstrument_name[3]

if (!_.contains(arrDeliveryDate, deliveryDate)) {

arr.push({

type : "table",

title : arrInstrument_name[1],

cols : ["PUT symbol", "ask1", "bid1", "mark_price", "underlying_price", "CALL symbol", "ask1", "bid1", "mark_price", "underlying_price"],

rows : []

})

arrDeliveryDate.push(arrInstrument_name[1])

}

// 遍历arr

_.each(arr, function(tbl) {

if (tbl.title == deliveryDate) {

if (tbl.rows.length == 0 && optionType == "P") {

tbl.rows.push([ticker.symbol, ticker.ask1, ticker.bid1, ticker.mark_price, ticker.underlying_price, "", "", "", "", ""])

return

} else if (tbl.rows.length == 0 && optionType == "C") {

tbl.rows.push(["", "", "", "", "", ticker.symbol, ticker.ask1, ticker.bid1, ticker.mark_price, ticker.underlying_price])

return

}

for (var i = 0 ; i < tbl.rows.length ; i++) {

if (tbl.rows[i][0] == "" && optionType == "P") {

tbl.rows[i][0] = ticker.symbol

tbl.rows[i][1] = ticker.ask1

tbl.rows[i][2] = ticker.bid1

tbl.rows[i][3] = ticker.mark_price

tbl.rows[i][4] = ticker.underlying_price

return

} else if(tbl.rows[i][5] == "" && optionType == "C") {

tbl.rows[i][5] = ticker.symbol

tbl.rows[i][6] = ticker.ask1

tbl.rows[i][7] = ticker.bid1

tbl.rows[i][8] = ticker.mark_price

tbl.rows[i][9] = ticker.underlying_price

return

}

}

if (optionType == "P") {

tbl.rows.push([ticker.symbol, ticker.ask1, ticker.bid1, ticker.mark_price, ticker.underlying_price, "", "", "", "", ""])

} else if(optionType == "C") {

tbl.rows.push(["", "", "", "", "", ticker.symbol, ticker.ask1, ticker.bid1, ticker.mark_price, ticker.underlying_price])

}

}

})

}

})

return arr

}

// 初始化

self.init()

return self

}

function main() {

// 初始化,清空日志

if(isResetLog) {

LogReset(1)

}

var m1 = createManager(exchanges[0], [], "option")

var m2 = createManager(exchanges[1], ["BTC-PERPETUAL"], "future")

// 切换为模拟盘

var base = "https://www.deribit.com"

if (isTestNet) {

m1.setBase(testNetBase)

m2.setBase(testNetBase)

base = testNetBase

}

while(true) {

// 期权

var ticker1GetSucc = m1.updateTicker(base + "/api/v2/public/get_book_summary_by_currency?currency=BTC&kind=option",

function(data) {return data.result},

function(ele) {return {bid1: ele.bid_price, ask1: ele.ask_price, symbol: ele.instrument_name, underlying_price: ele.underlying_price, mark_price: ele.mark_price}})

// 永续期货

var ticker2GetSucc = m2.updateTicker(base + "/api/v2/public/get_book_summary_by_currency?currency=BTC&kind=future",

function(data) {return data.result},

function(ele) {return {bid1: ele.bid_price, ask1: ele.ask_price, symbol: ele.instrument_name}})

if (!ticker1GetSucc || !ticker2GetSucc) {

Sleep(5000)

continue

}

// 更新持仓

var pos1GetSucc = m1.updatePos("GET", "/api/v2/private/get_positions", "currency=BTC&kind=option")

var pos2GetSucc = m2.updatePos("GET", "/api/v2/private/get_positions", "currency=BTC&kind=future")

if (!pos1GetSucc || !pos2GetSucc) {

Sleep(5000)

continue

}

// 交互

var cmd = GetCommand()

if(cmd) {

// 处理交互

Log("交互命令:", cmd)

var arr = cmd.split(":")

// cmdClearLog

if(arr[0] == "setContractType") {

// parseFloat(arr[1])

m1.e.SetContractType(arr[1])

Log("exchanges[0]交易所对象设置合约:", arr[1])

} else if (arr[0] == "buyOption") {

var actionData = arr[1].split(",")

var price = parseFloat(actionData[0])

var amount = parseFloat(actionData[1])

m1.e.SetDirection("buy")

m1.e.Buy(price, amount)

Log("执行价格:", price, "执行数量:", amount, "执行方向:", arr[0])

} else if (arr[0] == "sellOption") {

var actionData = arr[1].split(",")

var price = parseFloat(actionData[0])

var amount = parseFloat(actionData[1])

m1.e.SetDirection("sell")

m1.e.Sell(price, amount)

Log("执行价格:", price, "执行数量:", amount, "执行方向:", arr[0])

} else if (arr[0] == "setHedgeDeltaStep") {

hedgeDeltaStep = parseFloat(arr[1])

Log("设置参数hedgeDeltaStep:", hedgeDeltaStep)

}

}

// 获取期货合约价格

var perpetualTicker = m2.getTicker("BTC-PERPETUAL")

var hedgeMsg = " PERPETUAL:" + JSON.stringify(perpetualTicker)

// 从账户数据中获取delta总值

var acc1GetSucc = m1.updateAcc(function(self) {

self.e.SetCurrency("BTC_USD")

return self.e.GetAccount()

})

if (!acc1GetSucc) {

Sleep(5000)

continue

}

var sumDelta = m1.accData.Info.result.delta_total

if (Math.abs(sumDelta) > hedgeDeltaStep && perpetualTicker) {

if (sumDelta < 0) {

// delta 大于0 对冲期货做空

var amount = _N(Math.abs(sumDelta) * perpetualTicker.ask1, -1)

if (amount > 10) {

Log("超过对冲阈值,当前总delta:", sumDelta, "买入期货")

m2.e.SetContractType("BTC-PERPETUAL")

m2.e.SetDirection("buy")

m2.e.Buy(-1, amount)

} else {

hedgeMsg += ", 对冲下单量小于10"

}

} else {

// delta 小于0 对冲期货做多

var amount = _N(Math.abs(sumDelta) * perpetualTicker.bid1, -1)

if (amount > 10) {

Log("超过对冲阈值,当前总delta:", sumDelta, "卖出期货")

m2.e.SetContractType("BTC-PERPETUAL")

m2.e.SetDirection("sell")

m2.e.Sell(-1, amount)

} else {

hedgeMsg += ", 对冲下单量小于10"

}

}

}

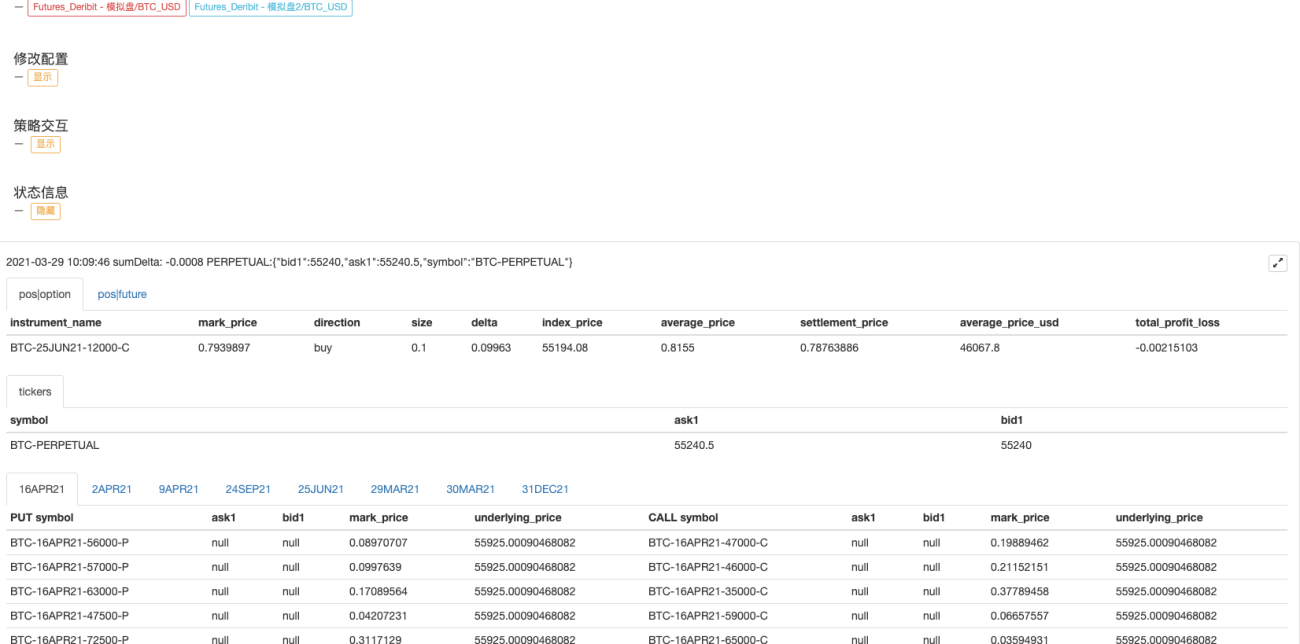

LogStatus(_D(), "sumDelta:", sumDelta, hedgeMsg,

"\n`" + JSON.stringify([m1.returnPosTbl(), m2.returnPosTbl()]) + "`", "\n`" + JSON.stringify(m2.returnTickersTbl()) + "`", "\n`" + JSON.stringify(m1.returnOptionTickersTbls()) + "`")

Sleep(10000)

}

}

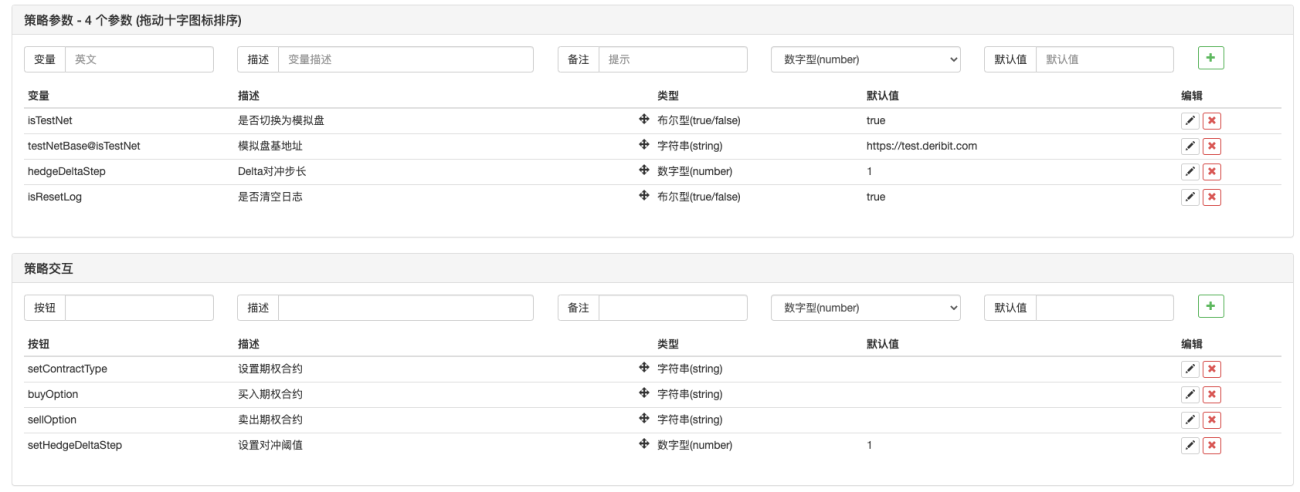

策略参数:

策略地址:https://www.fmz.com/strategy/265090

策略运行:

本策略为教学策略,学习为主,实盘请谨慎使用。