MyLanguage is a programmatic trading language that is compatible and enhanced with MyLanguage. The MyLanguage of FMZ Quant will undergo strict syntax checking. For example, when using language enhancement to embed JavaScript language code, an extra space character after the %% operator will cause an error to be reported.

-

Basic instructions

-

Contract

Cryptocurrency Contract

Cryptocurrency Contract

pinethis_week cryptocurrency futures contract this week next_week cryptocurrency futures contract next week month cryptocurrency futures contract month quarter cryptocurrency futures contract quarter next_quarter cryptocurrency futures contract next quarter third_quarter cryptocurrency futures contract third quarter last_quarter contract last quarter XBTUSD BITMEX perpetual contract swap cryptocurrency futures perpetual contracts other than BITMEX exchange For details, please refer to the exchange.SetContractType() function section of the JavaScript/Python/C++ documentation

-

Variables

A variable is a space opened up in the computer memory to store data. Simply put, it is used to store data.

open the first variable

mylang// assign 1 to variable a a:=1;In

MyLanguage, it is simple to distinguish from thedata volume:- Single-valued data: There is only one value, such as

0,1,'abc'. - Sequence data: a data sequence composed of a bunch of single-valued data, such as

Close(closing price), whereClosecontains the closing price ofnperiods.[ 10.1 , 10.2 , 10.3 , 10.4 , 10.5 ...]

Distinguish from "variable type"

- String type: it must be wrapped with ```''``, string type is not allowed to be used directly, and it need to be output to the view with the function.

mylangINFO(CLSOE>OPEN,'OK!');- Value types: including integers, floating-point numbers (decimals).

mylang// integer int:=2; // decimal float:=3.1;- Boolean type, using 1 (for true) or 0 (for false): 1, 0, true or false. For example:

A:=1>0;After this code is executed, the value ofAis 1.

mylang// The closing price of the current period is greater than -999, you will find that the return value of each period is 1, which means true, because the closing price is almost impossible to be negative. is_true:=Close>-999;- Global variables

javascriptVARIABLE:VALUE1:10; // Declare a global variable, assign the value 10, and execute it only once.Remark that when backtesting:

mylangVARIABLE:NX:0; // The initial global variable NX is 0 NX..NX+1; // Accumulate 1 each time INFO(1,NX); // Print NX every timeInitially, the

INFOstatement prints101, maybe it's not0initially?

The reason is that there are 100 initial K-lines in the backtest, and 100 K-lines have already been run through, which has been accumulated 100 times.

The actual price depends on how many K-lines are initially obtained.-

Naming rules

In most systems, variable naming does not allow the use of system "reserved words" (built-in variable names, function names). For example, the well-known

Close,C. In addition, pure numbers or leading numbers are not allowed. Finally, it is not allowed to be very long, and different systems have different length restrictions.

In fact, you don't have to worry about the efficiency of the mainstream system's parsing of Chinese. I believe that "MyLanguage" is very friendly to Chinese. For experienced programmer, it is recommended that you use the following two naming rules:- Chinese name

mylang// elegant output 5-day moving average:=MA(C,5);- English + underline

mylang// Output move_avg_5:=MA(C,5);If you prefer English, try to make the meaning of your variables as understandable as possible. Do not use names such as:

A1,AAA,BBB.... Trust me when you review your indicator code again in a few days, you will be very miserable due to memory loss. Similarly, when you export the code to others, the reader must be devastated.So from now on, embrace the "MyLanguage" to the fullest! I hope it can become a powerful tool for your analysis and decision-making.

- Single-valued data: There is only one value, such as

-

Type of Data

Type of data is a basic concept. When we assign a clear data to a variable in writing, the variable also becomes the type of the data itself.

-

- Type of Value:

1.2.3.1.1234.2.23456 ... -

- String type(str):

javascript'1' .'2' .'3' ,String types must be wrapped with '' -

- Sequence data:

pineA collection of data consisting of a series of single-valued data -

- Boolean type(boolean):

Use

1representstrueand0forfalse.Example

mylang// declare a variable of value type var_int := 1; // Declare a variable for sequence data var_arr := Close; // The string type cannot be declared alone, it needs to be combined with the function INFO(C>O, 'positive line');

-

-

Operator

The operation and calculation used to execute the indicator code are simply the symbols involved in the operation.

-

Assignment operator

to assign a value to a variable

-

:

:, represents assignment and output to the graph (subgraph).javascriptClose1:Close; // Assign Close to the variable Close1 and output to the figure -

:=

:=, represents assignment, but is not output to the graph (main graph, sub graph...), nor is it displayed in the status bar table.mylangClose2:=Close; // Assign Close to the variable Close2 -

^^

^^, Two^symbols represent assignment, assign values to variables and output to the graph (main graph).mylanglastPrice^^C; -

..

.., two.symbols represent assignment, assign values to variables and display variable names and values in the chart, but do not draw pictures to the chart (main picture, sub-picture...).mylangopenPrice..O

-

-

Relational operators

Relational operators are binary operators that are used in conditional expressions to determine the relationship between two data.

Return value: Boolean type, either

true(1) orfalse(0).-

- more than

>

mylang// Assign the operation result of 2>1 to the rv1 variable, at this time rv1=1 rv1:=2>1; - more than

-

- less than

<

mylang// Returns false, which is 0, because 2 is greater than 1 rv3:=2<1; - less than

-

- more than or equal to

>=

mylangx:=Close; // Assign the result of the operation that the closing price is more than or equal to 10 to the variable rv2 // Remark that since close is a sequence of data, when close>=10 is performed, the operation is performed in each period, so each period will have a return value of 1 and 0 rv2:=Close>=10; - more than or equal to

-

- less than or equal to

<=

omitted here - less than or equal to

-

- equal to

=

mylangA:=O=C; // Determine whether the opening price is equal to the closing price. - equal to

-

- Not equal to

<>

javascript1<>2 // To determine whether 1 is not equal to 2, the return value is 1 (true) - Not equal to

-

-

Logical Operators

Return value: Boolean type, either

true(1) orfalse(0).- The logical and

&&, can be replaced byand, and the left and right sides of the and connection must be established at the same time.

mylang// Determine whether cond_a, cond_b, cond_c are established at the same time cond_a:=2>1; cond_b:=4>3; cond_c:=6>5; cond_a && cond_b and cond_c; // The return value is 1, established- Logical or

||, you can useorto replace the left and right sides of the or link, one side is true (true), the whole is true (return value true).

mylangcond_a:=1>2; cond_b:=4>3; cond_c:=5>6; cond_a || cond_b or cond_c; // The return value is 1, established()operator, the expression in parentheses will be evaluated first.

javascript1>2 AND (2>3 OR 3<5) // The result of the operation is false 1>2 AND 2>3 OR 3<5 // The result of the operation is true - The logical and

-

Arithmetic operators

pythonReturn value: numeric typeArithmetic operators are arithmetic operators. It is a symbol for completing basic arithmetic operations (arithmetic operators), which is a symbol used to process four arithmetic operations.

-

plus +

mylangA:=1+1; // return 2 -

minus -

mylangA:=2-1; // return 1 -

*multiply *

mylangA:=2*2; // return 4 -

divide /

mylangA:=4/2; // return 2

-

-

-

Functions

-

Functions

In the programming world, a "function" is a piece of code that implements a certain function. And it can be called by other code, the general form is as follows:

javascriptfunction(param1,param2,...)-

Composition:

Function name (parameter1, parameter2, ...), may have no parameters or have multiple parameters. For example,

MA(x,n);means to return to the simple moving average ofxwithinnperiods. Among them,MA()is a function,xandnare the parameters of the function.When using a function, we need to understand the basic definition of the function, that is, what data can be obtained by calling the function. Generally speaking, functions have parameters. When we pass in parameters, we need to ensure that the incoming data type is consistent. At this stage, the code hinting function of most IDEs is very imperfect. There is a data type of the parameter given, which brings some trouble to our use, and

MA(x,n);is interpreted as:pineReturn to simple moving average Usage: AVG:=MA(X,N): N-day simple moving average of X, algorithm (X1+X2+X3+...+Xn)/N, N supports variablesThis is very unfriendly to beginners, but next, we will dissect the function thoroughly, trying to find a quick way to learn and use the function.

-

-

Return value

To learn functions quickly, we need to understand a concept first, it's called "return value", "Return", as the name suggests, means "return back"; The value represents "specific value", then the meaning of the return value is: the data that can be obtained.

mylang// Because it will be used in the following code, the variable return_value is used to receive and save the return value of function() // retrun_value := function(param1,param2); // For example: AVG:=MA(C,10); // AVG is retrun_value, function is MA function, param1 parameter: C is the closing price sequence data, param2 parameter: 10. -

Parameters

Secondly, the second important concept of the function is the parameter, and different return values can be obtained by passing in different parameters.

mylang// The variable ma5 receives the 5-day moving average of closing prices ma5:=MA(C,5); // The variable ma10 receives the 10-day moving average of closing prices ma10:=MA(C,10);The first parameter

Xof the above variablesma5,ma10isC(closing price), in fact,Cis also a function (returns the sequence of closing prices from the opening to the present), but it has no parameters. The 5 and 10 of the second parameter are used to tell theMA()function that we want to get the moving average of the closing price for a few days. The function becomes more flexible to use through the parameters. -

How to learn

-

- First, we need to understand what a function does, that is, what data this function can return to us.

-

- The last thing is to understand the type of the return value. After all, we use functions to get the return value.

-

- Moreover, we need to know the data type of the parameter

MA(x,n), if you don't know the data type of the parameterx,n, it will not be able to get the return correctly value.

- Moreover, we need to know the data type of the parameter

In the following function introduction and use, follow the above three principles.

-

-

-

Language enhancement

-

MyLanguageandJavaScriptlanguage mixed programmingmylang%% // This can call any API quantified of FMZ scope.TEST = function(obj) { return obj.val * 100; } %% Closing price: C; Closing price magnified 100 times: TEST(C); The last closing price is magnified by 100 times: TEST(REF(C, 1)); // When the mouse moves to the K-line of the backtest, the variable value will be prompted-

scopeobjectThe

scopeobject can add attributes and assign anonymous functions to attributes, and the anonymous function referenced by this attribute can be called in the code part of MyLanguage. -

scope.getRefs(obj)functionIn

JavaScriptcode block, call thescope.getRefs(obj)function to return the data of the passed inobjobject.The

JavaScriptcode wrapped with the following%% %%will get theCpassed in when theTEST(C)function in MyLanguage code is called Close price.

Thescope.getRefsfunction will return all the closing prices of this K-line data. Because of the use ofthrow "stop"to interrupt the program, the variablearrcontains the closing price of the first bar only. You can try to deletethrow "stop", it will execute thereturnat the end of theJavaScriptcode, and return all closing price data.javascript%% scope.TEST = function(obj){ var arr = scope.getRefs(obj) Log("arr:", arr) throw "stop" return } %% TEST(C); -

scope.bars

Access all K-line bars in the

JavaScriptcode block.The

TESTfunction returns a value. 1 is a negative line and 0 is a positive line.javascript%% scope.TEST = function(){ var bars = scope.bars return bars[bars.length - 1].Open > bars[bars.length - 1].Close ? 1 : 0 // Only numeric values can be returned } %% arr:TEST;python# Attention: # An anonymous function received by TEST, the return value must be a numeric value. # If the anonymous function has no parameters, it will result in an error when calling TEST, writing VAR:=TEST; and writing VAR:=TEST(); directly. # TEST in scope.TEST must be uppercase. -

scope.bar

In the

JavaScriptcode block, access the current bar.Calculate the average of the high opening and low closing prices.

javascript%% scope.TEST = function(){ var bar = scope.bar var ret = (bar.Open + bar.Close + bar.High + bar.Low) / 4 return ret } %% avg^^TEST; -

scope.depth

Access to market depth data (order book).

javascript%% scope.TEST = function(){ Log(scope.depth) throw "stop" // After printing the depth data once, throw an exception and pause } %% TEST; -

scope.symbol

Get the name string of current trading pair.

javascript%% scope.TEST = function(){ Log(scope.symbol) throw "stop" } %% TEST; -

scope.barPos

Get the Bar position of the K-line.

javascript%% scope.TEST = function(){ Log(scope.barPos) throw "stop" } %% TEST; -

scope.get_locals('name')

This function is used to get the variables in the code section of MyLanguage.

javascriptV:10; %% scope.TEST = function(obj){ return scope.get_locals('V') } %% GET_V:TEST(C);python# Attention: # If a variable cannot calculate the data due to insufficient periods, call the scope.get_locals function in the JavaScript code at this time # When getting this variable, an error will be reported: line:XX - undefined locals A variable name is undefined -

scope.canTrade

The

canTradeattribute marks whether the current bar can be traded (whether the current Bar is the last one)For example, judging that the market data is printed when the strategy is in a state where the order can be traded

pine%% scope.LOGTICKER = function() { if(exchange.IO("status") && scope.canTrade){ var ticker = exchange.GetTicker(); if(ticker){ Log("ticker:", ticker); return ticker.Last; } } } %% LASTPRICE..LOGTICKER;

-

-

Application example:

mylang%% scope.TEST = function(a){ if (a.val) { throw "stop" } } %% O>C,BK; C>O,SP; TEST(ISLASTSP);Stop the strategy after opening and closing a position once.

-

-

Multiperiod reference

The system will select a suitable underlying K-line period automatically, and use this underlying K-line period data to synthesize all referenced K-line data to ensure the accuracy of the data.

-

Use:

#EXPORT formula_name ... #ENDto create a formula. If the formula is not calculated just to obtain data of different periods, you can also write an empty formula.An empty formula is:

python#EXPORT TEST NOP; #END // end -

Use:

#IMPORT [MIN,period,formula name] AS variable valueto refer to a formula. Get various data of the set period (closing price, opening price, etc., obtained by variable value).The

MINin theIMPORTcommand means minute level.MyLanguage of FMZ Quant platform, and only theMINlevel is supported in theIMPORTcommand. Non-standard periods are now supported. For example, you can use#IMPORT [MIN, 240, TEST] AS VAR240to import data such as 240-minute period (4 hours) K-line.Code example:

mylang// This code demonstrates how to reference formulas of different periods in the same code // #EXPORT extended grammar, ending with #END marked as a formula, you can declare multiple #EXPORT TEST Mean value 1: EMA(C, 20); Mean value 2: EMA(C, 10); #END // end #IMPORT [MIN,15,TEST] AS VAR15 // Quoting the formula, the K-line period takes 15 minutes #IMPORT [MIN,30,TEST] AS VAR30 // Quoting the formula, the K-line period takes 30 minutes CROSSUP(VAR15.Mean value is 1, VAR30.Mean value is 1),BPK; CROSSDOWN(VAR15.Mean value is 2, VAR30.Mean value is 2),SPK; The highest price in fifteen minutes:VAR15.HIGH; The highest price in thirty minutes:VAR30.HIGH; AUTOFILTER; -

It is necessary to pay attention to when using

REF,LLV,HHVand other instructions to reference data when referencing data in multiple periods.mylang(*backtest start: 2021-08-05 00:00:00 end: 2021-08-05 00:15:00 period: 1m basePeriod: 1m exchanges: [{"eid":"Futures_OKCoin","currency":"ETH_USD"}] args: [["TradeAmount",100,126961],["ContractType","swap",126961]] *) %% scope.PRINTTIME = function() { var bars = scope.bars; return _D(bars[bars.length - 1].Time); } %% BARTIME:PRINTTIME; #EXPORT TEST REF1C:REF(C,1); REF1L:REF(L,1); #END // end #IMPORT [MIN,5,TEST] AS MIN5 INFO(1, 'C:', C, 'MIN5.REF1C:', MIN5.REF1C, 'REF(MIN5.C, 1):', REF(MIN5.C, 1), 'Trigger BAR time:', BARTIME, '#FF0000'); INFO(1, 'L:', L, 'MIN5.REF1L:', MIN5.REF1L, 'REF(MIN5.L, 1):', REF(MIN5.L, 1), 'Trigger BAR time:', BARTIME, '#32CD32'); AUTOFILTER;Comparing the difference between

MIN5.REF1CandREF(MIN5.C, 1),we can find:

MIN5.REF1Cis the value of the closing price of the penultimate BAR at the current moment of the 5-minute K-line data.

REF(MIN5.C, 1)is the K -line period of the current model (the above code backtest period is set to 1 minute, i.e. ```period: 1m``), the closing price of the 5-minute period where the penultimate BAR is located at the current moment.

These two definitions are differentiated, and they can be used as needed.

-

-

Mode Description

-

Signal filtering model of one opening and one leveling

In the model, the

AUTOFILTERfunction is written to control and realize the signal filtering of one opening and one closing. When there are multiple opening signals that meet the conditions, the first signal is taken as the valid signal, and the same signal on the K-line will be filtered out.Instructions supported by filtering model: BK, BP, BPK, SK, SP, SPK, CLOSEOUT, etc. Instructions with lot numbers such as BK(5) are not supported.

For example

mylangMA1:MA(CLOSE,5); MA2:MA(CLOSE,10); CROSSUP(C,MA1),BK; CROSSUP(MA1,MA2),BK; C>BKPRICE+10||C<BKPRICE-5,SP; AUTOFILTER;mylangComprehension: As in the above example, when AUTOFILTER is not set, the third row BK, the fourth row BK and the fifth row SP are triggered in sequence, and each K-line triggers a signal once. After opening the position, and closing the position, the model state is reset. If AUTOFILTER is set, after triggering BK, only SP is triggered, other BK signals are ignored, and each K-line triggers a signal once. -

Increase and decrease position model

The

AUTOFILTERfunction is not written in the model, allowing continuous opening signals or continuous closing signals, which can increase and decrease positions.Supported instructions: BK(N), BP(N), SK(N), SP(N), CLOSEOUT, BPK(N), SPK(N), open and close orders without lot size are not supported.

(1)Instruction grouping is supported.

(2)When multiple instruction conditions are satisfied at the same time, the signals are executed in the order in which the conditional statements are written.

For example:mylangMA1:MA(CLOSE,5); MA2:MA(CLOSE,10); CROSSUP(C,MA1),BK(1); CROSSUP(MA1,MA2),BK(1); C>BKPRICE+10||C<BKPRICE-5,SP(BKVOL);Use

TRADE\_AGAIN

It is possible to make the same command line, multiple signals in succession.pineComprehension: The above example is executed one by one, and the signal after execution is no longer triggered. Reset the model status after closing the position. A K -line triggers a signal once. -

Model with one K-line and one signal

Regardless of whether the K-line is finished, the signal is calculated in real-time orders, that is, the K-line is placed before the order is completed; the K-line is reviewed at the end. If the position direction does not match the signal direction at the end of the K-line, the position will be automatically synchronized.

For example:

mylangMA1:MA(CLOSE,5); MA2:MA(CLOSE,10); CROSSUP(MA1,MA2),BPK; //The 5-period moving average crosses up, and the 10-period moving average goes long. CROSSDOWN(MA1,MA2),SPK; //The 5-period moving average crosses down, and the 10-period moving average goes short. AUTOFILTER; -

A model of multiple signals on one K-line

The model uses

multsigto control and implement multiple signals from one K-line.Regardless of whether the K-line is finished, the signal is calculated in real-time.

The signal is not reviewed, there is no signal disappearance, and the direction of the signal is always consistent with the direction of the position.

If multiple signal conditions are met in one K-line, it can be executed repeatedly.

mylangFor example: MA1:MA(CLOSE,5); MA2:MA(CLOSE,10); CROSSUP(MA1,MA2),BK; C>BKPRICE+10||C<BKPRICE-5,SP; AUTOFILTER; MULTSIG(0,0,2,0);MULTSIGcan execute multiple command lines within one K-line.

A command line is only signaled once.mylangO<C,BK; // These conditions may all be executed in a K-line Bar, but only one signal per line 10+O<C,BK; // Strategy plus TRADE_AGAIN(10);it can make multiple signals per line 20+O<C,BK; 40+O<C,BK; MULTSIG(1,1,10);Supplement:

1.The model of adding and reducing positions, two ways of one signal and one K-line: placing an order at the closing price and placing an order at the order price, are both supported.

2.The model of adding and reducing positions also supports ordering of multiple signals from one K-line.

The model of adding and reducing positions, write themultsigfunction to realize multiple additions or multiple reductions on one K-line.

-

-

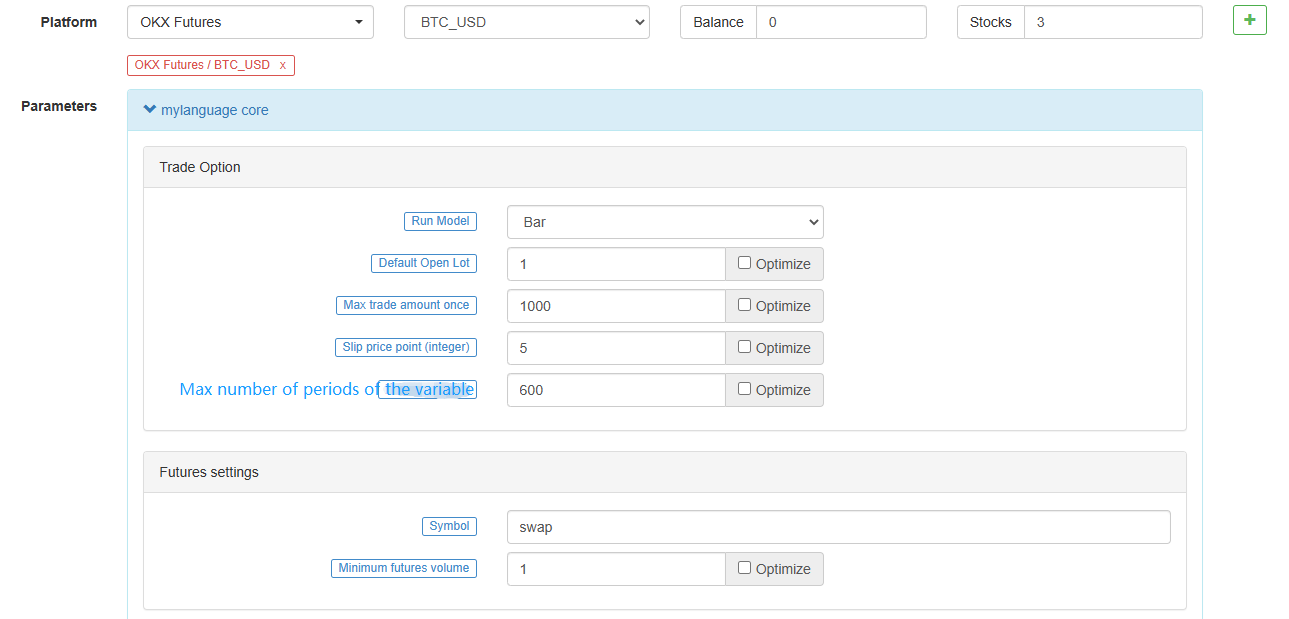

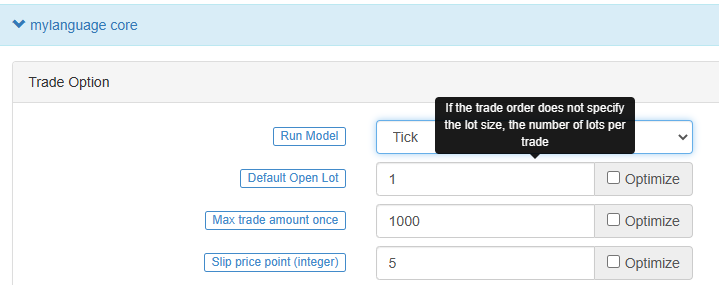

Execution mode

-

Bar model

The Bar model refers to the model that is executed after the current BAR is completed, and the trading is executed when the next BAR starts.

-

Tick model

The Tick model means that the model is executed once for each price movement and trades immediately when there is a signal.

The Tick model ignores the previous day's signal (the previous day's signal is executed immediately on the same day), and the Tick model focuses only on the current market data to determine whether the signal is triggered.

-

-

Chart display

-

Additional indicators for main chart

Use operator

^^, set indicators are displayed on the main chart while assigning values to variables.mylangMA60^^MA(C, 60); // Calculate the average indicator with the parameter of 60

-

Additional Indicators for sub-chart

Use operator

:, set indicators are displayed on the sub-chart while assigning values to variables.mylangATR:MA(MAX(MAX((HIGH-LOW),ABS(REF(CLOSE,1)-HIGH)),ABS(REF(CLOSE,1)-LOW)),26); // Assign a value to the ATR variable, the ":" symbol is followed by the formula for calculating the ATR

If you don't want it to be displayed on the main or subchart, use the "..." operator.

mylangMA60..MA(C, 60); // Calculate the average indicator with the parameter of 60You can use

DOTandCOLORREDto set the line type and color of the line, etc., in line with the habits of users familiar with the MyLanguage.

-

-

Common problems

Introduce the problems commonly encountered in the process of writing indicators, usually the points that need to be paid attention to when writing (continuously added).

-

Remark the semicolon

;at the end. -

Remark that system keywords cannot be declared as variables.

-

Remark that the string uses single quotes, for example: the string

'Open position'. -

Remark

Annotation

-

// The Remark content(input method can be typed in both Chinese and English) means that the code is not compiled during the execution process, that is, the content after//is not executed. Usually we use it to mark the meaning of the code, when it is convenient for code review, it can be quickly understood and recalled. -

{ Remark content }Block Remark.mylangA:=MA(C,10); {The previous line of code is to calculate the moving average.} -

(* Remark content *)Block Remark.mylangA:=MA(C,10); (*The previous line of code is to calculate the moving average.*)

-

-

Input

When writing code, because the input method is often switched between Chinese and English, resulting in symbol errors. The common errors are as follows: colon

:, terminator;, comma,, brackets(), etc. These characters in different states of Chinese and English need attention.If you use Sogou, Baidu, or Bing input methods, you can quickly switch between Chinese and English by pressing the

shiftkey once. -

Error-prone logic

- At least, not less than, not less than: the corresponding relational operator

>=. - Up to, at most, no more than: the corresponding relational operator

<=.

- At least, not less than, not less than: the corresponding relational operator

-

Strategy launch synchronization

In the futures strategy, if there is a manually opened position before the strategy robot starts, when the robot starts, it will detect the position information and synchronize it to the actual position status.

In the strategy, you can use theSP,BP,CLOSEOUTcommands to close the position.pine%% if (!scope.init) { var ticker = exchange.GetTicker(); exchange.Buy(ticker.Sell+10, 1); scope.init = true; } %% C>0, CLOSEOUT; -

Two-way positions are not supported

MyLanguage does not support the same contract with both long and short positions.

-

-

-

K-line data citation

-

OPEN

Obtain the opening price of the K-line chart.

Opening price

Function: OPEN, short for O

parameters: none

Explanation: Returns the opening price of "this period"

Sequence data

mylangOPEN gets the opening price of the K-line chart. Remark: 1.It can be abbreviated as O. Example 1: OO:=O; //Define OO as the opening price; Remark that the difference between O and 0. Example 2: NN:=BARSLAST(DATE<>REF(DATE,1)); OO:=REF(O,NN); //Take the opening price of the day Example 3: MA5:=MA(O,5); //Define the 5-period moving average of the opening price (O is short for OPEN). -

HIGH

Get the highest price on the K-line chart.

The highest price

Function: HIGH, abbreviated H

parameters: none

Explanation: Return the highest price of "this period"

Sequence data

mylangHIGH achieved the highest price on the K-line chart. Remark: 1.It can be abbreviated as H. Example 1: HH:=H; // Define HH as the highest price Example 2: HH:=HHV(H,5); // Take the maximum value of the highest price in 5 periods Example 3: REF(H,1); // Take the highest price of the previous K-line -

LOW

Get the lowest price on the K-line chart.

The lowest price

Function: LOW, abbreviated L

parameters: none

Explanation: Return the lowest price of "this period"

Sequence data

mylangLOW gets the lowest price on the K-line chart. Remark: 1.It can be abbreviated as L. Example 1: LL:=L; // Define LL as the lowest price Example 2: LL:=LLV(L,5); // Get the minimum value of the lowest price in 5 periods Example 3: REF(L,1); // Get the lowest price of the previous K-line -

CLOSE

Get the closing price of the K-line chart.

Closing price

Function: CLOSE, abbreviated as C

parameters: none

Explanation: Returns the closing price of "this period"

Sequence data

mylangCLOSE Get the closing price of the K-line chart Remarks: 1.Obtain the latest price when the intraday K-line has not finished. 2.It can be abbreviated as C. Example 1: A:=CLOSE; //Define the variable A as the closing price (A is the latest price when the intraday K-line has not finished) Example 2: MA5:=MA(C,5); //Define the 5-period moving average of the closing price (C is short for CLOSE) Example 3: A:=REF(C,1); //Get the closing price of the previous K-line -

VOL

Obtain the trading volume of K-line chart.

Trading volume

Function: VOL, abbreviated as V

parameters: none

Explanation: Returns the trading volume of "this period"

Sequence data

mylangVOL obtains the trading volume of the K-line chart. Remarks: It can be abbreviated as V. The return value of this function on the current TICK is the cumulative value of all TICK trading volume on that day. Example 1: VV:=V; // Define VV as the trading volume Example 2: REF(V,1); // Indicates the trading volume of the previous period Example 3: V>=REF(V,1); // The trading volume is greater than the trading volume of the previous period, indicating that the trading volume has increased (V is the abbreviation of VOL) -

OPI

Take the current total position in the futures (contract) market.

OpenInterest:OPI; -

REF

Forward citation.

mylangReference the value of X before N periods. Remarks: 1.When N is a valid value, but the current number of K-lines is less than N, returns null; 2.Return the current X value when N is 0; 3.Return a null value when N is null. 4.N can be a variable. Example 1: REF(CLOSE,5);Indicate the closing price of the 5th period before the current period is referenced Example 2: AA:=IFELSE(BARSBK>=1,REF(C,BARSBK),C);//Take the closing price of the K-line of the latest position opening signal // 1)When the BK signal is sent, the bar BARSBK returns null, then the current K-line REF(C, BARSBK) that sends out the BK signal returns null; // 2)When the BK signal is sent out, the K-line BARSBK returns null, and if BARSBK>=1 is not satisfied, it is the closing price of the K-line. // 3)The K-line BARSBK after the BK signal is sent, returns the number of periods from the current K-line between the K-line for purchasing and opening a position, REF(C,BARSBK) Return the closing price of the opening K-line. // 4)Example: three K-lines: 1, 2, and 3, 1 K-line is the current K-line of the position opening signal, then returns the closing price of the current K-line, 2, 3 The K-line returns the closing price of the 1 K-line. -

UNIT

Get the trading unit of the data contract.

mylangGet the trading unit of the data contract. Usage: UNIT takes the trading unit of the loaded data contract.Cryptocurrency spot

UNIT value is 1.

Cryptocurrency futures

The UNIT value is related to the contract currency.

pineOKEX futures currency standard contracts: 1 contract for BTC represents $100, 1 contract for other currencies represents $10 -

MINPRICE

The minimum variation price of the data contract.

mylangTake the minimum variation price of the data contract. Usage: MINPRICE; Take the minimum variation price of the loaded data contract. -

MINPRICE1

The minimum variation price of a trading contract.

mylangTake the minimum variation price of a trading contract. Usage: MINPRICE1; Take the minimum variation price of a trading contract.

-

-

Time function

-

BARPOS

Take the position of the K-line.

mylangBARPOS, Returns the number of periods from the first K-line to the current one. Remarks: 1.BARPOS returns the number of locally available K-line, counting from the data that exists on the local machine. 2.The return value of the first K-line existing in this machine is 1. Example 1:LLV(L,BARPOS); // Find the minimum value of locally available data. Example 2:IFELSE(BARPOS=1,H,0); // The current K-line is the first K-line that already exists in this machine, and it takes the highest value, otherwise it takes 0. -

DAYBARPOS

DAYBARPOS the current K-line BAR is the K-line BAR of the day.

-

PERIOD

The period value is the number of minutes.

1, 3, 5, 15, 30, 60, 1440 -

DATE

DateFunction DATE, Get the year, month, and day of the period since 1900.

mylangExample 1: AA..DATE; // The value of AA at the time of testing is 220218, which means February 18, 2022 -

TIME

The time of taking the K-line.

pineTIME, the time of taking the K-line. Remarks: 1.The function returns in real time in the intraday, and returns the starting time of the K-line after the K-line is completed. 2.This function returns the exchange data reception time, which is the exchange time. 3.The TIME function returns a six-digit form when used on a second period, namely: HHMMSS, and displays a four-digit form on other periods, namely: HHMM. 4.The TIME function can only be loaded in periods less than the daily period, and the return value of the function is always 1500 in the daily period and periods above the daily period. 5. It requires attention when use the TIME function to close a position at the end of the day (1).It is recommended to set the time for closing positions at the end of the market to the time that can actually be obtained from the return value of the K-line (for example: the return time of the last K-line in the 5-minute period of the thread index is 1455, and the closing time at the end of the market is set to TIME>=1458, CLOSEOUT; the signal of closing the position at the end of the market cannot appear in the effect test) (2).If the TIME function is used as the condition for closing the position at the end of the day, it is recommended that the opening conditions should also have a corresponding time limit (for example, if the condition for closing the position at the end of the day is set to TIME>=1458, CLOSEOUT; then the condition TIME needs to be added to the corresponding opening conditions. <1458; avoid re-opening after closing) Example 1: C>O&&TIME<1450,BK; C<O&&TIME<1450,SK; TIME>=1450,SP; TIME>=1450,BP; AUTOFILTER; // Close the position after 14:50. Example 2: ISLASTSK=0&&C>O&&TIME>=0915,SK; -

YEAR

Year.

mylangYEAR, year of acquisition. Remark: The value range of YEAR is 1970-2033. Example 1: N:=BARSLAST(YEAR<>REF(YEAR,1))+1; HH:=REF(HHV(H,N),N); LL:=REF(LLV(L,N),N); OO:=REF(VALUEWHEN(N=1,O),N); CC:=REF(C,N); // Take the highest price, lowest price, opening price, and closing price of the previous year Example 2: NN:=IFELSE(YEAR>=2000 AND MONTH>=1,0,1); -

MONTH

Take the month.

mylangMONTH, returns the month of a period. Remark: The value range of MONTH is 1-12. Example 1: VALUEWHEN(MONTH=3&&DAY=1,C); // Take its closing price when the K-line date is March 1 Example 2: C>=VALUEWHEN(MONTH<REF(MONTH,1),O),SP; -

DAY

Get the number of days in a period

mylangDAY, returns the number of days in a period. Remark: The value range of DAY is 1-31. Example 1: DAY=3&&TIME=0915,BK; // 3 days from the same day, at 9:15, buy it Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; CC:=IFELSE(DAY=1,VALUEWHEN(N=1,O),0); // When the date is 1, the opening price is taken, otherwise the value is 0 -

HOUR

Hour.

mylangHOUR, returns the number of hours in a period. Remark: The value range of HOUR is 0-23 Example 1: HOUR=10; // The return value is 1 on the K-line at 10:00, and the return value on the remaining K-lines is 0 -

MINUTE

Minute.

mylangMINUTE, returns the number of minutes in a period. Remarks: 1: The value range of MINUTE is 0-59 2: This function can only be loaded in the minute period, and returns the number of minutes when the K-line starts. Example 1: MINUTE=0; // The return value of the minute K-line at the hour is 1, and the return value of the other K-lines is 0 Example 2: TIME>1400&&MINUTE=50,SP; // Sell and close the position at 14:50 -

WEEKDAY

Get the number of the week.

mylangWEEKDAY, get the number of the week. Remark: 1: The value range of WEEKDAY is 0-6. (Sunday ~ Saturday) Example 1: N:=BARSLAST(MONTH<>REF(MONTH,1))+1; COUNT(WEEKDAY=5,N)=3&&TIME>=1450,BP; COUNT(WEEKDAY=5,N)=3&&TIME>=1450,SP; AUTOFILTER; // Automatically close positions at the end of the monthly delivery day Example 2: C>VALUEWHEN(WEEKDAY<REF(WEEKDAY,1),O)+10,BK; AUTOFILTER;

-

-

Logical judgment function

-

BARSTATUS

Return the position status for the current period.

mylangBARSTATUS returns the position status for the current period. Remark: The function returns 1 to indicate that the current period is the first period, returns 2 to indicate that it is the last period, and returns 0 to indicate that the current period is in the middle. Example: A:=IFELSE(BARSTATUS=1,H,0); // If the current K-line is the first period, variable A returns the highest value of the K-line, otherwise it takes 0 -

BETWEEN

Between.

mylangBETWEEN(X,Y,Z) indicates whether X is between Y and Z, returns 1 (Yes) if established, otherwise returns 0 (No). Remark: 1.The function returns 1(Yse) if X=Y, X=Z, or X=Y and Y=Z. Example 1: BETWEEN(CLOSE,MA5,MA10); // It indicates that the closing price is between the 5-day moving average and the 10-day moving average -

BARSLASTCOUNT

BARSLASTCOUNT(COND) counts the number of consecutive periods that satisfy the condition, counting forward from the current period.

pythonRemark: 1. The return value is the number of consecutive non zero periods calculated from the current period 2. the first time the condition is established when the return value of the current K-line BARSLASTCOUNT(COND) is 1 Example: BARSLASTCOUNT(CLOSE>OPEN); //Calculate the number of consecutive positive periods within the current K-line -

CROSS

Cross function.

mylangCROSS(A,B) means that A crosses B from bottom to top, and returns 1 (Yes) if established, otherwise returns 0 (No) Remark: 1.To meet the conditions for crossing, the previous k-line must satisfy A<=B, and when the current K-line satisfies A>B, it is considered to be crossing. Example 1: CROSS(CLOSE,MA(CLOSE,5)); // Indicates that the closing line crosses the 5-period moving average from below -

CROSSDOWN

Crossdown

mylangCROSSDOWN(A,B): indicates that when A passes through B from top to bottom, it returns 1 (Yes) if it is established, otherwise it returns 0 (No) Remark: 1.CROSSDOWN(A,B) is equivalent to CROSS(B,A), and CROSSDOWN(A,B) is easier to understand Example 1: MA5:=MA(C,5); MA10:=MA(C,10); CROSSDOWN(MA5,MA10),SK; // MA5 crosses down MA10 to sell and open a position // CROSSDOWN(MA5,MA10),SK; Same meaning as CROSSDOWN(MA5,MA10)=1,SK; -

CROSSUP

Crossup.

mylangCROSSUP(A,B) means that when A crosses B from the bottom up, it returns 1 (Yes) if it is established, otherwise it returns 0 (No) Remark: 1.CROSSUP(A,B) is equivalent to CROSS(A,B), and CROSSUP(A,B) is easier to understand. Example 1: MA5:=MA(C,5); MA10:=MA(C,10); CROSSUP(MA5,MA10),BK; // MA5 crosses MA10, buy open positions // CROSSUP(MA5,MA10),BK;与CROSSUP(MA5,MA10)=1,BK; express the same meaning -

EVERY

Determine if it is continuously satisfied.

mylangEVERY(COND,N), Determine whether the COND condition is always satisfied within N periods. The return value of the function is 1 if it is satisfied, and 0 if it is not satisfied. Remarks: 1.N contains the current K-line. 2.If N is a valid value, but there are not so many K-lines in front, or N is a null value, it means that the condition is not satisfied, and the function returns a value of 0. 3.N can be a variable. Example 1: EVERY(CLOSE>OPEN,5); // Indicates that it has been a positive line for 5 periods Example 2: MA5:=MA(C,5); // Define a 5-period moving average MA10:=MA(C,10); // Define a 10-period moving average EVERY(MA5>MA10,4),BK; // If MA5 is greater than MA10 within 4 periods, then buy the open position // EVERY(MA5>MA10,4),BK; has the same meaning as EVERY(MA5>MA10,4)=1,BK; -

EXIST

Determine if there is satisfaction.

mylangEXIST(COND, N) judges whether there is a condition that satisfies COND within N periods. Remarks: 1.N contains the current K-line. 2.N can be a variable. 3.If N is a valid value, but there are not so many K-lines in front, it is calculated according to the actual number of periods. Example 1: EXIST(CLOSE>REF(HIGH,1),10); // Indicates whether there is a closing price greater than the highest price of the previous period in 10 periods, returns 1 if it exists, and returns 0 if it does not exist Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; EXIST(C>MA(C,5),N); // Indicates whether there is a K-line that satisfies the closing price greater than the 5-period moving average on the day, returns 1 if it exists, returns 0 if it does not exist -

IF

Condition function.

IF(COND,A,B)Returns A if the COND condition is true, otherwise returns B. Remarks: 1.COND is a judgment condition; A and B can be conditions or values. 2.This function supports the variable circular reference to the previous period's own variable, that is, supports the following writing Y: IF(CON,X,REF(Y,1)). Example 1: IF(ISUP,H,L); // The K-line is the positive line, the highest price is taken, otherwise the lowest price is taken Example 2: A:=IF(MA5>MA10,CROSS(DIFF,DEA),IF(CROSS(D,K),2,0)); // When MA5>MA10, check whether it satisfies the DIFF and pass through DEA, otherwise (MA5 is not greater than MA10), when K and D are dead fork, let A be assigned a value of 2, if none of the above conditions are met, A is assigned a value of 0 A=1,BPK; // When MA5>MA10, the condition for opening a long position is to cross DEA above the DIFF A=2,SPK; // When MA5 is not greater than MA10, use K and D dead forks as the conditions for opening short positions -

IFELSE

Condition function.

IFELSE(COND,A,B) Returns A if the COND condition is true, otherwise returns B. Remarks: 1.COND is a judgment condition; A and B can be conditions or values. 2.This function supports variable circular reference to the previous period's own variable, that is, supports the following writing Y: IFELSE(CON,X,REF(Y,1)); Example 1: IFELSE(ISUP,H,L); // The K-line is the positive line, the highest price is taken, otherwise the lowest price is taken Example 2: A:=IFELSE(MA5>MA10,CROSS(DIFF,DEA),IFELSE(CROSS(D,K),2,0)); // When MA5>MA10, check whether it satisfies the DIFF and pass through DEA, otherwise (MA5 is not greater than MA10), when K and D are dead fork, let A be assigned a value of 2, if none of the above conditions are met, A is assigned a value of 0 A=1,BPK; // When MA5>MA10, the condition for opening a long position is to cross DEA above the DIFF A=2,SPK; // When MA5 is not greater than MA10, use K and D dead forks as the conditions for opening short positions -

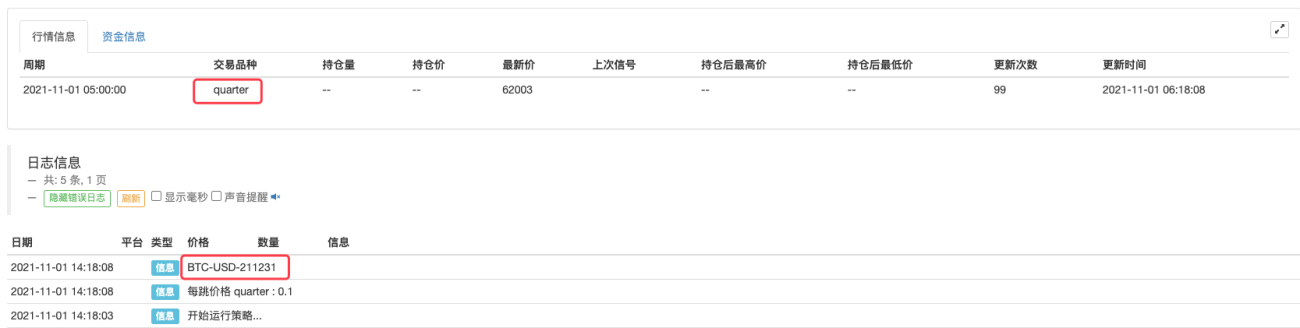

ISCONTRACT

Whether it is currently the specified contract.

mylangWhether ISCONTRACT(CODE) is currently the specified contract. Usage: ISCONTRACT(CODE); It is the current contract that returns 1, not the current contract that returns 0. Remark: 1.When judging whether it is a specified contract, CODE can be the trading code of the contract. Example: ISCONTRACT('this_week'); // Cryptocurrency OKEX futures contract ISCONTRACT('XBTUSD'); // Cryptocurrency BITMEX futures contractRegular expressions are supported.

Judgment contract

mylangISCONTRACT('this_week'); // Determine whether the current contract is OKEX futures this_week contractDetermining the name of the exchange

mylangISCONTRACT('@Futures_(Binance|FTX)'); // Determine whether the current exchange object is Binance futures or FTX futures ISCONTRACT('@(OKEX|Bitfinex)'); // To judge the exchange, you need to add the @ character at the beginning -

ISDOWN

Negative line.

mylangISDOWN Determine whether the period closed negative. Remark: 1.ISDOWN is equivalent to C<O Examples: ISDOWN=1&&C<REF(C,1),SK; // When the K-line closes negative and the closing price is less than the closing price of the previous period, then open short position // ISDOWN=1&&C<REF(C,1),SK; has the same meaning as ISDOWN&&C<REF(C,1),SK; -

ISEQUAL

Flat plate.

mylangISEQUAL determines whether the period is flat or not. Remark: 1.ISEQUAL is equal to C=O Example 1: EVERY(ISEQUAL=1,2),CLOSEOUT; // If 2 K-lines are flat for a sustained period, then all flat -

ISLASTBAR

Determine whether the period is the last K-line.

mylangISLASTBAR judges whether the period is the last K-line. Example 1: VALUEWHEN(ISLASTBAR=1,REF(H,1)); // The current K-line is the last K-line, then take the highest price of the previous period -

ISNULL

Determine the null value.

mylangISNULL Determine the null value. Usage: ISNULL(N); If N is null, the function returns 1; if N is non-null, the function returns 0. Example :MA5:=IFELSE(ISNULL(MA(C,5))=1,C,MA(C,5)); // Define a five-period moving average. When the number of K-lines is less than five, return the closing price of the current K-line -

ISUP

Positive line.

mylangISUP determines whether the period closes positive or not. Remark: 1.ISUP is equivalent to C>O. Example : ISUP=1&&C>REF(C,1),BK; // If the current K-line closes positive and the closing price is greater than the closing price of the previous period, then open a long position // ISUP=1&&C>REF(C,1),BK; together with ISUP&&C>REF(C,1),BK // Express the same meaning -

LAST

Judgment function.

mylangLAST(COND,N1,N2) determine whether the COND condition has been satisfied in the past N1 to N2 periods. Remarks: 1.If the difference between N1 and N2 is only one period (such as N1=3, N2=2), the function determines whether the condition is satisfied on the period closest to the current K-line (that is, to determine whether the K-line in the past N2 periods satisfies the condition or not) ). 2.When N1/N2 is a valid value, but the current number of K-lines is less than N1/N2, or the case of N1/N2 null, the representative is not valid and the function returns 0. 3.N1 and N2 cannot be variables. Example 1: LAST(CLOSE>OPEN,10,5); // Indicates a positive line from the 10th period to the 5th period in the past Example 2: MA5:=MA(C,5); LAST(C>MA5,4,3); // Determine if the K-line that is 3 periods away from the current K-line meets C is greater than MA5 -

LONGCROSS

Maintain the cross function.

mylangLONGCROSS(A,B,N)Indicates that A is less than B in N periods, and A crosses B from bottom to top in this period. Remarks: 1.When N is a valid value, but the current number of K-lines is less than N, the LONGCROSS function returns null. 2.N does not support variables. Example 1: LONGCROSS(CLOSE,MA(CLOSE,10),20); // Indicates that the closing line is below the 10-day SMA for 20 periods and then crosses the 10-day SMA from bottom to top -

NOT

Not.

mylangNOT(X): Takes not. Returns 1 when X = 0, otherwise returns 0. Example 1: NOT(ISLASTBK); If the last signal is not a BK signal, NOT(ISLASTBK) returns a value of 1; if the last signal is a BK signal, NOT(ISLASTBK) returns a value of 0. Example 2: NOT(BARSBK>=1)=1; // BK signal is issued when the current K-line meets the conditions // NOT(BARSBK>=1)=1 has the same meaning as NOT(BARSBK>=1) -

NULL

Return null.

mylangReturn null Usage: MA5:=MA(C,5); MA10:=MA(C,10); A:=IFELSE(MA5>MA10,MA5,NULL),COLORRED; // When MA5>MA10, draw the five-day moving average MA5, when MA5>MA10 is not satisfied, return null and no line is drawn -

VALUEWHEN

Take values.

mylangVALUEWHEN(COND,X)When the COND condition is true, the current value of X is taken. If the COND condition is not established, the value of X when the last COND condition is established is taken. Remark: X can be a numerical value or a condition. Example 1: VALUEWHEN(HIGH>REF(HHV(HIGH,5),1),HIGH); // Indicates that the current highest price is returned when the current highest price is greater than the maximum value of the highest prices in the previous five periods Example 2: VALUEWHEN(DATE<>REF(DATE,1),O); // Indicates to take the opening price of the first K-line of the day (that is, the opening price of the day) Example 3: VALUEWHEN(DATE<>REF(DATE,1),L>REF(H,1)); // Indicates whether the current low price is greater than the high price of yesterday's last K-line on the first K-line of the day. Returns 1, indicating that the day jumped higher. If returns 0, it means the day does not meet the condition of jumping high.

-

-

Loop execution function

-

LOOP2

Loop condition function.

LOOP2(COND,A,B); The loop condition function returns A if the COND condition is true, otherwise returns B. Remarks: 1.COND is a judgment condition; A and B can be conditions or values. 2.This function supports variable circular reference to the previous period's own variable, that is, supports the following writing method Y:=LOOP2(CON,X,REF(Y,1)); Example 1: X:=LOOP2(ISUP,H,REF(X,1)); // If the K-line is a positive line, take the highest price of the current K-line, otherwise, take the highest price of the K-line that was a positive line last time; if there has been no positive line before, X returns null Example 2: BB:=LOOP2(BARSBK=1,LOOP2(L>LV(L,4),L,LV(L,4)),LOOP2(L>REF(BB,1),L,REF(BB,1))); // When holding a long order, the lowest price in the previous 4 periods of the long order is the starting stop loss point BB, the lowest price of the subsequent K-line is higher than the previous lowest price, and the current lowest price stop loss point is taken, otherwise take the previous low and stop loss SS:=LOOP2(BARSSK=1,LOOP2(H<HV(H,4),H,HV(H,4)),LOOP2(H<REF(SS,1),H,REF(SS,1))); // When holding a short order, the highest price in the previous 4 periods of the short order is the starting stop loss point SS, the highest price is lower than the previous highest price, and the current highest price stop loss point is taken, otherwise take the stop loss point of the previous high point H>HV(H,20),BK; L<LV(L,20),SK; C<BB,SP; C>SS,BP; AUTOFILTER;

-

-

Financial statistics functions

-

BARSCOUNT

The number of periods from the first valid period to the current one.

pineBARSCOUNT(COND)The number of periods from the first valid period to the current one. Remarks: 1.The return value is the number of periods counted by COND from the first valid period until now. 2.When the condition is satisfied for the first time, the return value of BARSCOUNT(COND) on the K-line is 0. Example: BARSCOUNT(MA(C,4)); // Calculate the number of periods from the first time MA(C,4) has a return value to the current one -

BARSLAST

The position where the last condition was met.

mylangBARSLAST(COND), the number of periods since the last time the condition COND was established. Remark: 1.When the condition is satisfied, the return value of BARSLAST(COND) on the current K-line is 0. Example 1: BARSLAST(OPEN>CLOSE); // Number of periods from the last negative line to the present Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, number of K-lines for the day // Since the return value of BARSLAST(COND) is 0 for the current K-line when the condition is established, "+1" is the number of k-lines for that dayDescription of the

BARSLASTfunction:- 1.If the current K-line condition is established, it will return 0.

- 2.If it does not hold, it will keep going back until it finds the K-line for which the condition holds, returning a number of periods traced.

- 3.If the K-line whose condition holds is not found even after tracing back to the end, returns null.

-

BARSSINCE

The number of periods from when the first condition was established to the current one.

pineBARSSINCE(COND)the number of periods from when the first condition was established to the current one. Remarks: 1.The return value is the number of periods from the first time COND was established to the current. 2.When the condition is satisfied for the first time, the return value of BARSSINCE(COND) on the K-line is 0. Example: BARSSINCE(CLOSE>OPEN); // Count the number of periods from the first positive K-line to the present -

BARSSINCEN

Count the number of periods from the first condition held in N periods to the current one.

mylangBARSSINCEN(COND,N) counts the number of periods between the first condition held in N periods and the current one. Remarks: 1.N contains the current K-line. 2.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines. 3.Returns null if N is 0. 4.N can be a variable. Examples: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines on the day BARSSINCEN(ISUP,N); // Count the number of periods from the first positive line met in N periods to the current period -

CONDBARS

Obtain the number of periods between the most recent K-lines that satisfy the A,B condition.

pineCONDBARS(A,B); obtain the number of periods between the most recent K-lines that satisfy the A,B condition. Attention: 1.This function returns the number of periods without the last K-line that meets the condition. 2.The closest satisfied condition to the current K-line is the B condition, then the function returns the number of periods from the last K-line that satisfied the A condition to the K-line that satisfied the B condition (the first K-line that satisfied the B condition after the A condition was satisfied). The closest satisfied condition to the current K-line is the A condition, then the function returns the number of periods from the last K-line that satisfied the B condition to the K-line that satisfied the A condition (the first K-line that satisfied the A condition after the B condition was satisfied). Example 1: MA5:=MA(C,5); // 5-period moving average MA10:=MA(C,10); // 10-period moving average CONDBARS(CROSSUP(MA5,MA10),CROSSDOWN(MA5,MA10)); // The number of periods between the last time the 5-period moving average crosses the 10-period moving average and the 5-period moving average crosses the 10-period moving average -

COUNT

Total statistics.

mylangCOUNT(COND,N), counts the number of periods in N periods that satisfy the COND condition. Remarks: 1.N contains the current K-line. 2.If N is 0, count from the first valid value. 3.If N is valid, but the current number of K-lines is less than N, count from the first one to the current period. 4.If N is null, the return value is null. 5.N can be a variable. Example 1: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines on the day M:=COUNT(ISUP,N); // Count the number of positive lines since the market opened in the minute period Example 2: MA5:=MA(C,5); // Define the 5-period moving average MA10:=MA(C,10); // Define the 10-period moving average M:=COUNT(CROSSUP(MA5,MA10),0); // Count the number of times that the 5-period moving average crossed the 10-period moving average during the period from the applied market data to the current period. -

DMA

Dynamic moving average.

mylangDMA(X,A): Find the dynamic moving average of X, where A must be less than 1 and greater than 0. Remarks: 1.A can be a variable. 2.If A<=0 or A>=1, return null. Calculation formula: DMA(X,A)=REF(DMA(X,A),1)*(1-A)+X*A Example 1: DMA3:=DMA(C,0.3); // The calculation result is REF(DMA3,1)*(1-0.3)+C*0.3 -

EMA

Index-weighted moving average.

mylangEMA(X,N): finds the index-weighted moving average (smoothed moving average) of the N-period X values. Remarks: 1.N contains the current K-line. 2.A larger weight is given to the K-line that is closer to the current one. 3.When N is valid, but the current number of K-lines is less than N, the actual number of lines will be counted. 4.When N is 0 or null, the return value is null. 5.N can be a variable. EMA(X,N)=2*X/(N+1)+(N-1)*REF(EMA(X,N),1)/(N+1) Example 1: EMA10:=EMA(C,10); // Find the 10-period index-weighted moving average of closing prices -

EMA2

Linear weighted moving average.

pineEMA2(X,N); // Find the linear weighted moving average (also known as WMA) of the N period X values EMA2(X,N)=[N*X0+(N-1)*X1+(N-2)*X2+...+1*X(N-1)]/[N+(N-1)+(N-2)+...+1], X0 represents the current period value, X1 represents the previous period value Remarks: 1.N contains the current K-line. 2.When N is valid, but the current number of K-lines is less than N, the return value is null. 3.When N is 0 or null, the return value is null. 4.N can be a variable. Example 1: EMA2(H,5); // Find the linearly weighted moving average of the highest price over 5 periods -

EMAWH

Index-weighted moving average.

mylangEMAWH(C,N), index-weighted moving average, also known as smoothed moving average, it uses index-weighted method to give greater weight to the K-line that is closer to the current one. Remark: 1.When N is valid and the current number of K-lines is less than N, or when the value of the previous period is still applied to the current period, EMAWH returns null. Because the weight of the current period is mainly considered in the EMAWH calculation formula, when the period is longer, the previous period value has less influence on the current period. EMAWH starts showing the values taken when the previous data no longer affects the current period, so even if the selected data starts at a different time, the EMAWH value of the currently displayed K-line will not change. 2.When N is 0 or null, the return value is null. 3.N cannot be a variable. EMAWH(C,N)=2*C/(N+1)+(N-1)*REF(EMAWH(C,N),1)/(N+1) Remark: EMAWH is used in the same way as EMA(C,N) -

HARMEAN

Reconciliation average.

javascriptHARMEAN(X,N), Find the reconciliation average of X over N periods. Example of algorithm: HARMEAN(X,5)=1/[(1/X1+1/X2+1/X3+1/X4+1/X5)/5] Remarks: 1.N contains the current K-line. 2.The reconciliation average and the reciprocal simple average are the reciprocals of each other. 3.When N is valid, but the current number of K-lines is less than N, the function returns null. 4.When N is 0 or null, the function returns null. 5.When X is 0 or null, the function returns null. 6.N can be a variable. Example: HM5:=HARMEAN(C,5); // Find the reconciliation average of the 5-period closing prices -

HHV

The highest value.

mylangHHV(X,N): Find the highest value of X over N periods. Remark: 1.N contains the current K-line. 2.If N is 0, start counting from the first valid value. 3.When N is valid, but the current number of K-lines is less than N, calculate according to the actual number of lines. 4.When N is null, the return value is null. 5.N can be a variable. Example 1: HH:=HHV(H,4); // Find the maximum value of the highest price in 4 periods, that is, the 4-period high point (including the current K-line) Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day HH1:=HHV(H,N); // In the minute period, the high point in the day -

HV

The highest value except the current K-line.

mylangHV(X,N), Find the highest value of X in N periods (excluding the current K-line). Remarks: 1.If N is 0, it starts from the first valid value (excluding the current K-line). 2.When N is valid, but the current number of K-lines is less than N, the first K-line returns null according to the actual number of K-lines. 3.When N is null, the return value is null. 4.N can be a variable. Example 1: HH:=HV(H,10); // Find the highest point of the first 10 K-lines Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; NN:=REF(N,N); ZH:=VALUEWHEN(DATE<>REF(DATE,1),HV(H,NN)); // In the minute period, find the highest price yesterday Example 3: The results of HV(H,5) and REF(HHV(H,5),1) are the same, and it is more convenient to write in HV. -

HHVBARS

The previous highest point position.

mylangHHVBARS(X,N), find the highest value of X in N periods to the current number of periods. Remarks: 1.If N is 0, it starts from the first valid value (excluding the current K-line). 2.When N is valid, but the current number of K-lines is less than N, the first K-line returns null according to the actual number of K-lines. 3.When N is null, the return value is null. 4.N can be a variable. Example 1: HHVBARS(VOL,0); // Find the period with the largest historical volume to the current number of periods (the return value of HHVBARS(VOL,0); on the K-line with the maximum value is 0, and the return value of the first K-line after the maximum value is 1, and so on) Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day ZHBARS:=REF(HHVBARS(H,N),N)+N; // In the minute period, find the number of periods between the K-line where the highest price was yesterday and the current K-line -

LLV

The minimum value.

mylangLLV(X,N), find the minimum value of X over N periods. Remarks: 1.N contains the current K-line. 2.If N is 0 then the count starts from the first valid value. 3.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines. 4.When N is null, the return value is null. 5.N can be a variable. Example 1: LL:=LLV(L,5); // Find the lowest point of 5 K-lines (including the current K-line) Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day LL1:=LLV(L,N); // In the minute period, find the minimum value from the first K-line of the day to the lowest price of all K-lines in the current period -

LV

The lowest value except the current K-line.

mylangLV(X,N), find the minimum value of X in N periods (excluding the current K-line). Remarks: 1.If N is 0 then the count starts from the first valid value. 2.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines. 3.When N is null, the return value is null. 4.N can be a variable. Example 1: LL:=LV(L,10); // Find the lowest point of the previous 10 K-lines (excluding the current K-line) Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day NN:=REF(N,N); ZL:=VALUEWHEN(DATE<>REF(DATE,1),LV(L,NN)); // Find the lowest price yesterday in the minute period. Example 3: The results of LV(L,5) and REF(LLV(L,5),1) are the same, and it is more convenient to write with LV. -

LLVBARS

The previous lowest point position.

mylangLLVBARS(X,N), find the lowest value of X in N periods to the current number of periods. Remarks: 1.If N is 0, it starts from the first valid value (excluding the current K-line). 2.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines, the first K-line returns null. 3.When N is null, the return value is null. 4.N can be a variable. Example 1: LLVBARS(VOL,0); // Find the period with the smallest historical volume to the current number of periods (the return value of HHVBARS(VOL,0); on the K-line with the minimum value is 0, and the return value of the first K-line after the minimum value is 1, and so on) Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day ZLBARS:=REF(LLVBARS(L,N),N)+N; // In the minute period, find the number of periods between the K-line where yesterday's lowest price is located to the current K-line. -

MA

Arithmetic moving average.

mylangMA(X,N), find the simple moving average of X over N periods. Algorithm: MA(X,5)=(X1+X2+X3+X4+X5)/5 Remarks: 1.N contains the current K-line. 2.Simple moving averages follow the simplest statistical approach, taking the average of prices over a specific period of time in the past. 3.When N is valid, but the current number of K-lines is less than N, the function returns null. 4.When N is 0 or null, the function returns null. 5.N can be a variable. Example 1: MA5:=MA(C,5); // Find the simple moving average of the 5-period closing price Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-lines in the day M:=IFELSE(N>10,10,N); // If there are more than 10 K-lines, M takes 10, otherwise M takes the actual number MA10:=MA(C,M); // In the minute period, if the number of K-lines on the day is less than 10, the MA10 is calculated according to the actual number of K-lines, and the MA10 is calculated according to the 10-period if it is more than 10 K-lines. -

MV

Take the average.

mylangMV(A,...P), take the average of A to P. Remarks: 1.It supports to take the average of 2-16 values. 2.A...P can be numbers or variables. Example 1: MV(CLOSE,OPEN); // Take the average of the closing and opening prices -

NUMPOW

Sum of powers of natural numbers.

mylangNUMPOW(X,N,M), sum of powers of natural numbers. Algorithm: NUMPOW(x,n,m)=n^m*x+(n-1)^m*ref(x,1)+(n-2)^m*ref(x,2)+...+2^m*ref(x,n-2)+1^m*ref(x,n-1) Attention: 1.N is a natural number, M is a real number; and N and M cannot be variables. 2.X is the basic variable. Example: JZ:=NUMPOW(C,5,2); -

SAR

Parabolic steering.

mylangSAR(N,STEP,MAX), returns the parabolic steering value. Calculated according to the formula SAR(n)=SAR(n-1)+AF*(EP(n-1)-SAR(n-1)). Among which: SAR(n-1): The absolute value of the last K-line SAR. AF: acceleration factor, when AF is less than MAX, it is accumulated by AF+STEP one by one, and AF is recalculated when the ups and downs are converted. EP: An extreme value within an up or down market is the highest price of the previous K-line in an up market; the lowest price of the previous K-line in a down market. Remark: 1.parameter N, Step, Max do not support variables. Example 1: SAR(17,0.03,0.3); // Indicates that 17 periods of parabolic steering are calculated, the step size is 3%, and the limit value is 30% -

SMA

Extended index-weighted moving average.

mylangSMA(X,N,M) find the extended index-weighted moving average over N periods of X, where M is the weight. Calculation formula: SMA(X,N,M)=REF(SMA(X,N,M),1)*(N-M)/N+X(N)*M/N Remarks: 1.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines. 2.When N is 0 or null, the function returns null. Example 1: SMA10:=SMA(C,10,3); // Extended index-weighted moving average of the 10-period closing price found, with a weight of 3 -

SMMA

Fluent moving average.

mylangSMMA(X,N), X is a variable, N is a period, SMMA(X, N) represents the fluent moving average of X in N periods on the current K-line Algorithm: SMMA(X,N)=(SUM1-MMA+X)/N Among which SUM1=X1+X2+.....+XN MMA=SUM1/N Example 1: SMMA(C,5); // The 5-period fluent moving average of the closing price -

SORT

Take the value sorted at the corresponding position.

pythonSORT(Type,POS,N1,N2,...,N16); Arrange in ascending (descending) order, and take the value corresponding to the POSth parameter. Remarks: 1.When Type is 0, it is sorted in ascending order, and when Type is 1, it is sorted in descending order. 2.TYPE, POS, variables are not supported. 3.N1,...,N16 are parameters, support constants, variables, up to 16 parameters. Example: SORT(0,3,2,1,5,3); // 2, 1, 5, 3 are arranged in ascending order, take the third number 3 -

SUM

SUM.

mylangSUM(X,N), find the sum of X over N periods. Remarks: 1.N contains the current K-line. 2.If N is 0, start counting from the first valid value. 3.When N is valid, but the current number of K-lines is less than N, it is calculated according to the actual number of lines. 4.When N is null, the return value is null. 5.N can be a variable. Example 1: SUM(VOL,25); Indicates the total trading volume within 25 periods of statistics. Example 2: N:=BARSLAST(DATE<>REF(DATE,1))+1; // Minute period, the number of K-line in the day SUM(VOL,N); // In the minute period, take the sum of the day's trading volume -

SUMBARS

The number of periods to accumulate to the specified value.

pineSUMBARS(X,A), fine the number of periods to accumulate to the specified value. Remark: parameter A supports variables. Example 1: SUMBARS(VOL,20000); Accumulate the volume forward until it is greater than or equal to 20000, and return the period number of this range. -

TRMA

Triangular moving average.

pineTRMA(X,N), find the triangular moving average of X over N periods. Algorithm: The triangular moving average formula is to take an arithmetic moving average and apply the arithmetic moving average again to the first moving average. The TRMA(X,N) algorithm is as follows: ma_half= MA(X,N/2) trma=MA(ma_half,N/2) Remarks: 1.N contains the current K-line. 2.When N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0 or null, the function returns null. 4.N supports the use of variables. Example 1: TRMA5:=TRMA(CLOSE,5); // Calculates the triangular moving average of closing prices over 5-period. (N is not divisible by 2) // TRMA(CLOSE,5)=MA(MA(CLOSE,(5+1)/2)),(5+1)/2); Example 2: TRMA10:=TRMA(CLOSE,10); // Calculates a triangular moving average of closing prices over 10-period. (N is divisible by 2) // TRMA(CLOSE,10)=MA(MA(CLOSE,10/2),(10/2)+1)); -

TSMA

Time series moving average.

javascriptTSMA(X,N), find the time series triangular moving average of X over N periods. TSMA(a,n) the algorithm is as follows: ysum=a[i]+a[i-1]+...+a[i-n+1] xsum=i+i-1+..+i-n+1 xxsum=i*i+(i-1)*(i-1)+...+(i-n+1)*(i-n+1) xysum=i*a[i]+(i-1)*a[i-1]+...+(i-n+1)*a[i-n+1] k=(xysum -(ysum/n)*xsum)/(xxsum- xsum/n * xsum) // slope b= ysum/n - k*xsum/n forcast[i]=k*i+b // Linear regression tsma[i] = forcast[i]+k // Linear regression + slope Remarks: 1.When N is valid, but the current number of K-lines is less than N, the function returns null. 2.When N is 0 or null, the function returns null. 3.N supports the use of variables. Example 1: TSMA5:=TSMA(CLOSE,5); // Calculate the serial triangular moving average of closing prices over 5 periods

-

-

Mathematical statistics functions

-

AVEDEV

Average absolute deviation.

mylangAVEDEV(X,N), returns the average absolute deviation of X over N periods. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N cannot be a variable. Example of algorithm: Calculate the value of AVEDEV(C,3); on the latest K-line. It can be expressed by MyLanguage functions as follows: (ABS(C-(C+REF(C,1)+REF(C,2))/3)+ABS(REF(C,1)-(C+REF(C,1)+REF(C,2))/3)+ABS(REF(C,2)-(C+REF(C,1)+REF(C,2))/3))/3; Example: AVEDEV(C,5); // Returns the average absolute deviation of the closing price over 5 periods // Indicates the average value of the absolute value of the difference between the closing price of each period and the average value of the closing prices in 5 periods, and judges the degree of deviation between the closing price and its average value -

COEFFICIENTR

Pearson correlation coefficient.

mylangCOEFFICIENTR(X,Y,N), find the Pearson correlation coefficient of X and Y over N periods. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N can be a variable. Example of algorithm: Calculate COEFFICIENTR(O, C, 3); the value on the nearest K-line. It can be expressed by MyLanguage functions as follows: (((O-MA(O,3))*(C-MA(C,3))+(REF(O,1)-MA(O,3))*(REF(C,1)-MA(C,3))+(REF(O,2)-MA(O,3))*(REF(C,2)-MA(C,3))) /(STD(O,3)*STD(C,3)))/(3-1); Example: COEFFICIENTR(C,O,10); //Find the Pearson correlation coefficient over 10 periods //The Pearson correlation coefficient is a measure of the degree of correlation between two random variables -

CORRELATION

Correlation coefficient.

mylangCORRELATION(X,Y,N), find the correlation coefficient of X and Y in N periods. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N can be a variable. Example of algorithm: Calculate CORRELATION(O,C,3); the value on the latest K-line. In terms of a MyLanguage function, it can be expressed as follows: (((O-MA(O,3))*(C-MA(C,3))+(REF(O,1)-MA(O,3))*(REF(C,1)-MA(C,3))+(REF(O,2)-MA(O,3))*(REF(C,2)-MA(C,3))))/SQRT((SQUARE(O-MA(O,3))+SQUARE(REF(O,1)-MA(O,3))+SQUARE(REF(O,2)-MA(O,3)))*(SQUARE(C-MA(C,3))+SQUARE(REF(C,1)-MA(C,3))+SQUARE(REF(C,2)-MA(C,3)))); Example: CORRELATION(C,O,10); // Find the correlation coefficient over 10 periods // The correlation coefficient is a measure of the degree of correlation between two random variables -

COVAR

Covariance.

mylangCOVAR(X,Y,N) Find the covariance of X and Y over N periods. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N can be a variable. Example of algorithm: Calculate COVAR(O,C,3); the value on the nearest K-line. In terms of a MyLanguage function, it can be expressed as follows: (((O-MA(O,3))*(C-MA(C,3))+(REF(O,1)-MA(O,3))*(REF(C,1)-MA(C,3))+(REF(O,2)-MA(O,3))*(REF(C,2)-MA(C,3))) )/3; Example: COVAR(C,O,10); // Find the covariance over 10 periods // The variance between two different variables is the covariance. If the trend of the two variables is the same, then the covariance between the two variables is positive; if the trend of the two variables is opposite, then the covariance between the two variables is negative -

DEVSQ

Obtain the sum of squared data deviations.

mylangDEVSQ(X,N): Calculate the sum of squares of data deviations for N periods of data X. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N is not supported as a variable. Example of algorithm: Calculate the value of DEVSQ(C,3); on the nearest K-line. In terms of a MyLanguage function, it can be expressed as follows: SQUARE(C-(C+REF(C,1)+REF(C,2))/3)+SQUARE(REF(C,1)-(C+REF(C,1)+REF(C,2))/3)+SQUARE(REF(C,2)-(C+REF(C,1)+REF(C,2))/3); Example: DEVSQ(C,5); // Calculate the sum of squared data deviations for 5 periods of the data closing price //Represents the sum of the square deviation between the closing price and the average closing price respectively, DEVSQ (C, 5) means the sum of the square deviations between the closing price and the average closing price of the 5 periods -

FORCAST

Linear regression value.

mylangForcast (x, n) is the predicted value of N-period linear regression of X. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N can be a variable. Example of algorithm: Calculate the value of FORCAST(C,3) on the nearest K-line by using the least square method. 1.Establish a linear formula of one variable: y=a+b*i+m 2.Estimated value of Y: y(i)^=a+b*i 3.Find the residuals: m^=y(i)-y(i)^=y(i)-a-b*i 4.Sum of squared errors. Q=m(1)*m(1)+...+m(3)*m(3)=[y(1)-a-b*1]*[y(1)-a-b*1]+...+[y(3)-a-b*3]*[y(3)-a-b*3] 5.Find the first-order partial derivative of parameters a and b in the linear formula: 2*{[y(1)-a-b*1]+...+[y(3)-a-b*3]}*(-1)=0 2*[y(1)-a-b*1]*(-1)+...+[y(3)-a-b*3]*(-3)=0 6.Combine the above two formulas and solve for the values of a,b: a=(y(1)+y(2)+y(3))/3-b(i(1)+i(2)+i(3))/3 b=(y(1)*i(1)+y(2)*i(2)+y(3)*i(3)-(3*((i(1)+i(2)+i(3))/3)*((y(1)+y(2)+y(3))/3))/((i(1)^2+i(2)^2+i(3)^2)-3*((i(1)+i(2)+i(3))/3)^2) 7.Bring the values of a, b, and i to 1 to find the value of y. The above formula can be expressed in terms of a MyLanguage function as follows: BB:=(3*C+2*REF(C,1)+REF(C,2)-(3*((1+2+3)/3)*MA(C,3)))/((SQUARE(1)+SQUARE(2)+SQUARE(3))-3*SQUARE((1+2+3)/3)); AA:=MA(C,3)-BB*(1+2+3)/3; YY:=AA+BB*3; Example: FORCAST(CLOSE,5); // Means to calculate the predicted value of 5-period linear regression -

KURTOSIS

Kurtosis coefficient.

mylangKURTOSIS(X,N), find the kurtosis coefficient of X over N periods. Remarks: 1.N contains the current K-line. 2.N is valid, but the current number of K-lines is less than N, the function returns null. 3.When N is 0, the function returns null. 4.N is null, the function returns null. 5.N can be a variable. 6.N is at least 4, if less than 4, returns null. Example of algorithm: Calculate KURTOSIS(C,4); the value on the nearest K-line. In terms of a MyLanguage function, it can be expressed as follows: ((POW(C-MA(C,4),4)+POW(REF(C,1)-MA(C,4),4)+POW(REF(C,2)-MA(C,4),4)+POW(REF(C,3)-MA(C,4),4)) /POW(STD(C,4),4))*(4*(4+1)/((4-1)*(4-2)*(4-3)))-3*SQUARE(4-1)/((4-2)*(4-3)); Example: KURTOSIS(C,10); // Indicates the 10-period peak of the closing price. The peak reflects the sharpness or flatness of a distribution compared to a normal distribution. Positive peaks indicate a relatively sharp distribution. Negative peaks indicate a relatively flat distribution -

NORMPDF

Normal distribution probability density.

mylangNORMPDF(X,MU,SIGMA), the return parameter is the value of the normal distribution density function of MU and SIGMA at X. Remarks: 1.If MU or SIGMA is null, the function returns null. 2.MU and SIGMA support variables. Example of algorithm: The random variable X obeys a probability distribution with location parameter MU and scale parameter SIGMA, and its probability density is NORMPDF(X,MU,SIGMA). It can be approximately expressed as follows by using MyLanguage function: (1/(SQRT(2*3.14)*SIGMA))*EXP((-SQUARE(X-MU))/(2*SQUARE(SIGMA))); Example: TR:=MAX(MAX((HIGH-LOW),ABS(REF(CLOSE,1)-HIGH)),ABS(REF(CLOSE,1)-LOW)); ATR:=MA(TR,26); // Find the simple moving average of TR over 26 periods ZZ..NORMPDF(ATR,0,1); // Define the variable ZZ and return the probability density of ATR following the standard normal distribution -

SKEWNESS

Skewness coefficient.