ট্র্যাকিং ব্রেকআউট কৌশল

সংক্ষিপ্ত বিবরণ

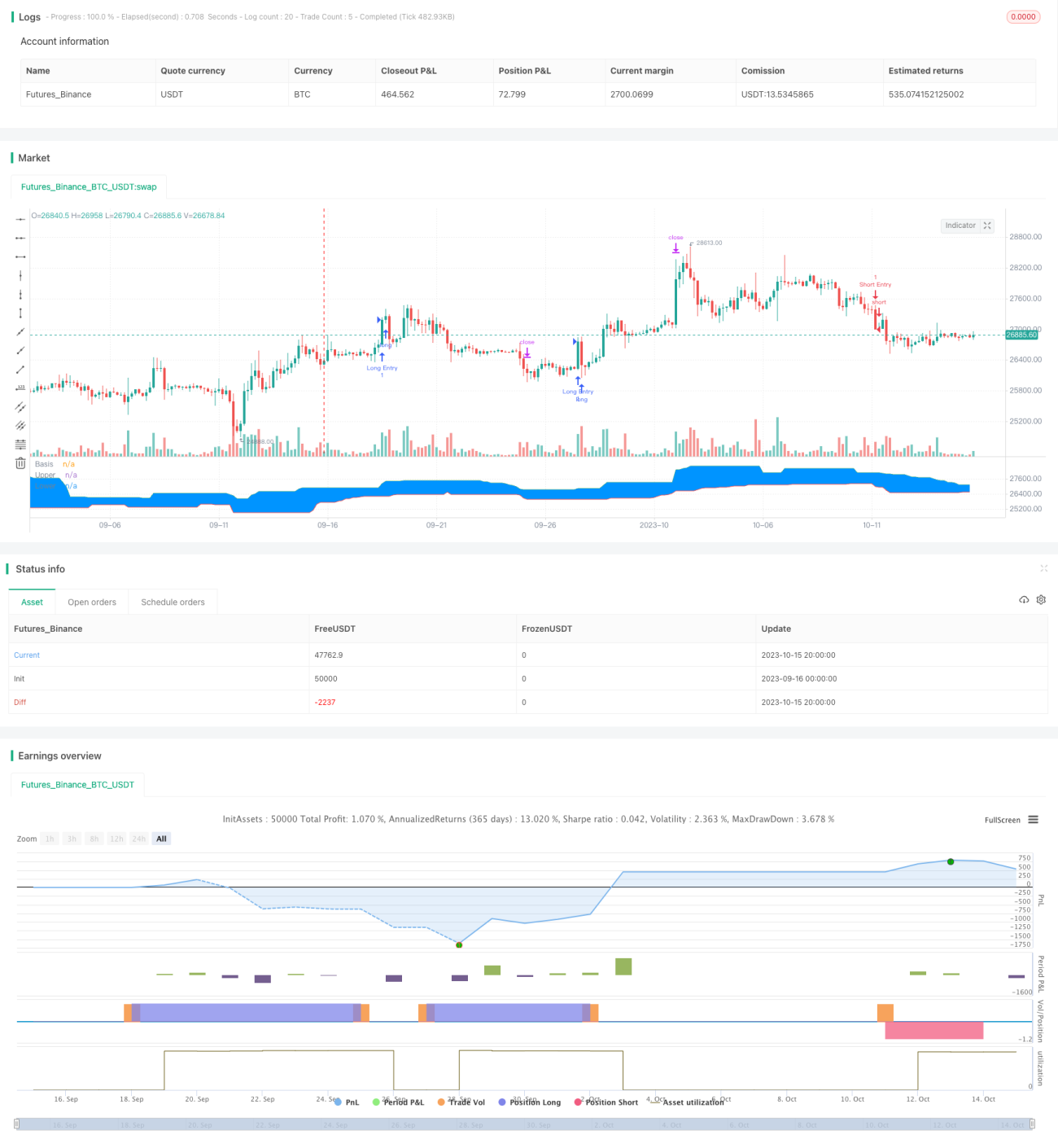

এই কৌশলটি মূলত "ডোনচিয়ান চ্যানেল" সূচকের মাধ্যমে ট্র্যাকিং-ভিত্তিক ব্রেকআউট ট্রেডিং কৌশল বাস্তবায়ন করে। কৌশলটি ট্রেন্ড এবং ব্রেকআউট উভয় ট্রেডিং ধারণাকে একত্রিত করে, দীর্ঘমেয়াদী ট্রেন্ড বিচারের ভিত্তিতে স্বল্পমেয়াদী ব্রেকআউট পয়েন্ট খুঁজে এন্ট্রি করে, যার ফলে ট্রেন্ডিং মার্কেটে ট্রেন্ড অনুযায়ী ট্রেড করা সম্ভব হয়। এছাড়াও, কৌশলটি স্টপ লস এবং টেক প্রফিট স্তর নির্ধারণ করে, যাতে প্রতিটি ট্রেডের ঝুঁকি-পুরস্কার অনুপাত নিয়ন্ত্রণ করা যায়। সামগ্রিকভাবে, এই কৌশলটির ট্রেন্ড অনুসরণের সুবিধা রয়েছে, যা ট্রেন্ডের সাথে সঙ্গতি রেখে দীর্ঘমেয়াদী ট্রেন্ডের সুযোগ গ্রহণ করতে পারে।

কৌশলের মূলনীতি

-

"ডোনচিয়ান চ্যানেল" সূচকের প্যারামিটার সেট করা, ডিফল্ট সময়কাল 20;

-

EMA (এক্সপোনেনশিয়াল মুভিং এভারেজ) সেট করা, ডিফল্ট সময়কাল 200;

-

ঝুঁকি-পুরস্কার অনুপাত সেট করা, ডিফল্ট 1.5;

-

ব্রেকআউট রিট্রেসমেন্ট প্যারামিটার সেট করা, যথাক্রমে লং এবং শর্টের জন্য;

-

পূর্ববর্তী ব্রেকআউটটি উচ্চ বা নিম্ন ছিল কিনা তা রেকর্ড করা;

-

লং সিগন্যাল: যদি পূর্ববর্তী ব্রেকআউ�টি নিম্ন হয়, এবং দাম ডোনচিয়ান উপরের রেখার উপরে এবং EMA এর উপরে থাকে, তাহলে লং সিগন্যাল তৈরি হয়;

-

শর্ট সিগন্যাল: যদি পূর্ববর্তী ব্রেকআউটটি উচ্চ হয়, এবং দাম ডোনচিয়ান নিচের রেখার নিচে এবং EMA এর নিচে থাকে, তাহলে শর্ট সিগন্যাল তৈরি হয়;

-

লং পজিশনে প্রবেশের পর, স্টপ লস সেট করা হয় ডোনচিয়ান নিচের রেখা থেকে 5 পয়েন্ট রিট্রেসমেন্টে, এবং টেক প্রফিট সেট করা হয় ঝুঁকি-পুরস্কার অনুপাত × স্টপ লস দূরত্ব;

-

শর্ট পজিশনে প্রবেশের পর, স্টপ লস সেট করা হয় ডোনচিয়ান উপরের রেখা থেকে 5 পয়েন্ট রিট্রেসমেন্টে, এবং টেক প্রফিট সেট করা হয় ঝুঁকি-পুরস্কার অনুপাত × স্টপ লস দূরত্ব।

এইভাবে, কৌশলটি ট্রেন্ড বিচার এবং ব্রেকআউট অপারেশনকে একত্রিত করে, ট্রেন্ডের সাথে সঙ্গতি রেখে দীর্ঘমেয়াদী ট্রেন্ডে স্বল্পমেয়াদী সুযোগ ধরতে পারে। একইসাথে, স্টপ লস এবং টেক প্রফিট সেটিংস প্রতিটি ট্রেডের ঝুঁকি-পুরস্কার পরিস্থিতি নিয়ন্ত্রণ করতে পারে।

সুবিধা বিশ্লেষণ

-

দীর্ঘমেয়াদী ট্রেন্ড অনুসরণ করে, ট্রেন্ডের সাথে সঙ্গতি রেখে, বিপরীত ট্রেন্ডে ট্রেড এড়ানো যায়।

-

ডোনচিয়ান চ্যানেল একটি দীর্ঘমেয়াদী সূচক হিসেবে, EMA এর সাথে ফিল্টারিং করে, ট্রেন্ডের দিক ভালোভাবে বিচার করতে পারে।

-

স্টপ লস এবং টেক প্রফিট মেকানিজম প্রতিটি ট্রেডের ঝুঁকি নিয়ন্ত্রণ করে, সম্ভাব্য ক্ষতি সীমিত করতে পারে।

-

ঝুঁকি-পুরস্কার অনুপাত অপ্টিমাইজ করে লাভ-ক্ষতির অনুপাত বাড়ানো যায়, অতিরিক্ত রিটার্ন অর্জন করা যায়।

-

ব্যাকটেস্টিং প্যারামিটার সেটিংস নমনীয়, বিভিন্ন বাজারের জন্য সেরা প্যারামিটার কম্বিনেশন সামঞ্জস্য করা যায়।

ঝুঁকি বিশ্লেষণ

-

ডোনচিয়ান চ্যানেল এবং EMA ফিল্টারিং সূচক হিসেবে ভুল সংকেত দিতে পারে।

-

ব্রেকআউট ট্রেডে সহজেই ফাঁদে পড়া যায়, স্পষ্ট ট্রেন্ড প্রসঙ্গ চিহ্নিত করা প্রয়োজন।

-

স্টপ লস এবং টেক প্রফিট দূরত্ব নির্দিষ্ট, বাজারের ওঠানামার মাত্রা অনুযায়ী সামঞ্জস্য করা যায় না।

-

প্যারামিটার অপ্টিমাইজেশনের সম্ভাবনা সীমিত, বাস্তব ট্রেডিংয়ে কার্যকারিতা নিশ্চিত করা কঠিন।

-

ট্রেডিং সিস্টেম অনেক এলোমেলো ঘটনার পরীক্ষা সহ্য করতে পারে না, কালো রাজহাঁসের ঘটনায় বড় ক্ষতি হতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

-

আরও বেশি সূচক যোগ করে ফিল্টারিং বিবেচনা করা যেতে পারে, যেমন অসিলেটর সূচক, সংকেতের মান উন্নত করতে।

-

স্মার্ট স্টপ লস এবং টেক প্রফিট সেট করা যেতে পারে, বাজারের ওঠানামার মাত্রা এবং ATR সূচকের ভিত্তিতে লাভ-ক্ষতির অবস্থান গতিশীলভাবে সামঞ্জস্য করা।

-

মেশিন লার্নিংয়ের মতো পদ্ধতি ব্যবহার করে প্যারামিটার পরীক্ষা এবং অপ্টিমাইজ করা যেতে পারে, যাতে বাস্তব বাজারের কাছাকাছি হয়।

-

এন্ট্রি লজিক অপ্টিমাইজ করা যেতে পারে, VOLUME বা অস্থিরতা সূচক সহায়ক শর্ত হিসেবে ব্যবহার করে ফাঁদ এড়ানো যায়।

-

ট্রেন্ড ফলোয়িং কৌশল বা মেশিন লার্নিংয়ের সাথে একত্রিত করে হাইব্রিড কৌশল তৈরি করা যেতে পারে, স্থিতিশীলতা বাড়াতে।

সারসংক্ষেপ

এই কৌশলটি একটি ট্র্যাকিং-ভিত্তিক ব্রেকআউট কৌশল হিসেবে, মূল ধারণা হলো দীর্ঘমেয়াদী ট্রেন্ড নির্ণয় করার পর, ব্রেকআউটকে সংকেত হিসেবে ব্যবহার করে ট্রেন্ডের দিকে ট্রেড করা, এবং প্রতিটি ট্রেডের ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ লস ও টেক প্রফিট নির্ধারণ করা। এই কৌশলটির কিছু সুবিধা রয়েছে, তবে কিছু উন্নতির জায়গাও রয়েছে। সামগ্রিকভাবে, প্যারামিটার সেটিং, এন্ট্রি সময় নির্বাচন ইত্যাদি ভালোভাবে পরিচালনা করলে এবং অন্যান্য প্রযুক্তির মাধ্যমে উন্নত করলে, এই কৌশলটি একটি ব্যবহারিক ট্রেন্ড ফলোয়িং কৌশল হতে পারে। তবে বিনিয়োগকারীদের মনে রাখতে হবে, কোনো ট্রেডিং সিস্টেমই বাজারের ঝুঁকি সম্পূর্ণভাবে এড়াতে পারে না, তাই ঝুঁকি ব্যবস্থাপনা করা প্রয়োজন।

/*backtest

start: 2023-09-16 00:00:00

end: 2023-10-16 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Welcome to my second script on Tradingview with Pinescript

// First of, I'm sorry for the amount of comments on this script, this script was a challenge for me, fun one for sure, but I wanted to thoroughly go through every step before making the script public

// Glad I did so because I fixed some weird things and I ended up forgetting to add the EMA into the equation so our entry signals were a mess- 1