সমন্বয় আকৃতির পতনে কেনার কৌশল

সারমর্ম

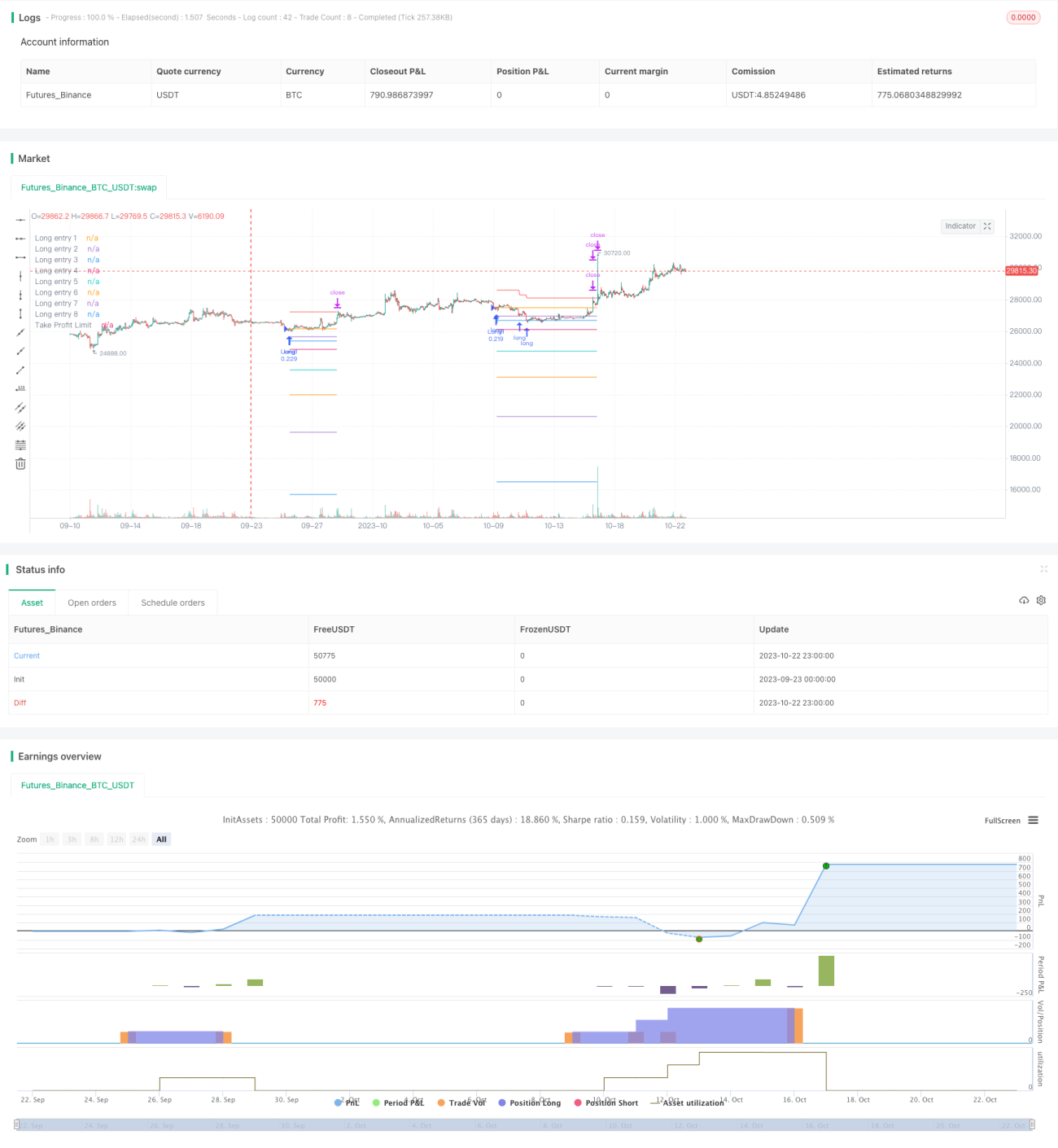

এই কৌশলটি RSI সূচক এবং দামের মুভিং এভারেজের সমন্বয়ে, শেয়ারের দাম মুভিং এভারেজের নিচে নেমে গেলে ওভারসোল্ড অবস্থায় লং পজিশন খোলার সুযোগ খোঁজে। দাম আরও কমলে, পূর্বনির্ধারিত শতাংশ অনুযায়ী স্তরে স্তরে পজিশন বাড়ানো হয়, যাতে গড় ক্রয়মূল্য কমানো যায়। যখন পজিশন লাভজনক হয় এবং নির্ধারিত টেক প্রফিট শতাংশে পৌঁছায়, তখন পজিশন বন্ধ করা হয়। একই সাথে, কৌশলটিতে প্রগ্রেসিভ টেক প্রফিট মেকানিজম রয়েছে, যা ইতিমধ্যে অর্জিত প্রতিটি লটের লাভের ভিত্তিতে সামগ্রিক পজিশনের টেক প্রফিট মূল্য গতিশীলভাবে সামঞ্জস্য করে। এটি কার্যকরভাবে লোকসানের ঝুঁকি কমায় এবং ধীরে ধীরে বেরিয়ে আসতে সাহায্য করে।

কৌশলের নীতি

- যখন RSI সূচক ওভারসোল্ড লাইন ২৯ এর নিচে থাকে এবং ক্লোজিং প্রাইস মুভিং এভারেজের নিচে থাকে, তখন প্রথম লং অর্ডার খোলা হয়।

- প্রথম অর্ডারের তুলনায় দাম ২% কমলে দ্বিতীয় লং অর্ডার যোগ করা হয়; ৩% কমলে তৃতীয়বার যোগ করা হয়, এবং এভাবে সর্বোচ্চ ৮ বার পর্যন্ত যোগ করা যায়। এটি পর্যায়ক্রমে পজিশন গঠনের প্রভাব ফেলে।

- প্রতিবার পজিশন খোলার সময়, সেই সময়ের খোলার মূল্য রেকর্ড করা হয়। এই মূল্যবিন্দুগুলো এন্ট্রির রেফারেন্স মূল্য হিসেবে কাজ করে। চার্টে এই মূল্যরেখাগুলো আঁকা হয়।

- পজিশন খোলার পর, পজিশনের গড় মূল্য গণনা করা হয়। গড় মূল্যের ৩% প্রতিটি লটের টেক প্রফিট মূল্য এবং ৪% সামগ্রিক পজিশনের টেক প্রফিট মূল্য হিসেবে নির্ধারিত হয়।

- যখন দাম কোনো নির্দিষ্ট লটের টেক প্রফিট মূল্যের উপরে উঠে যায়, তখন সেই লটটি বন্ধ করার সিদ্ধান্ত নেওয়া হয়।

- প্রগ্রেসিভ টেক প্রফিটের গণনা পদ্ধতি: প্রতিবার একটি লট বন্ধ করার সময়, সেই লটের অর্জিত লাভ সামগ্রিক টেক প্রফিট মূল্য থেকে বাদ দেওয়া হয়। এর ফলে টেক প্রফিট লাইন ধীরে ধীরে নিচে নামে, এবং কেবল যখন সব লটের লাভ সর্বোচ্চ লোকসান পূরণ করতে সক্ষম হয়, তখনই সম্পূর্ণ পজিশন বন্ধ হয়।

- যখন দাম প্রগ্রেসিভ টেক প্রফিট লাইন স্পর্শ করে, তখন সম্পূর্ণ পজিশন বন্ধ করা হয়।

সুবিধা বিশ্লেষণ

- RSI সূচক ওভারসোল্ড এলাকা যথাযথভাবে চিহ্নিত করতে পারে, যা রিভার্সালের সুযোগ ধরতে সহায়তা করে।

- বারবার স্তরে স্তরে পজিশন যোগ করে নিম্ন মূল্যে গড় ক্রয়মূল্য কমানো যায়।

- প্রগ্রেসিভ টেক প্রফিট লোকসানের ঝুঁকি কমায় এবং ধীরে ধীরে বেরিয়ে আসতে সাহায্য করে। লোকসান হলেও তা নির্দিষ্ট সীমার মধ্যে রাখা যায়।

- কনফিগারযোগ্য টেক প্রফিট শতাংশ এবং পজিশন যোগের শতাংশ বাজারের সাথে কৌশলের ঝুঁকি সামঞ্জস্য করতে দেয়।

- চার্টে খোলার রেফারেন্স লাইন এবং টেক প্রফিট লাইন আঁকায় পজিশন বিতরণ সহজেই বোঝা যায়।

ঝুঁকি বিশ্লেষণ

- অস্থির বাজারে বারবার পজিশন খোলা ও বন্ধ হতে পারে, যার ফলে স্লিপেজে ক্ষতি হতে পারে। RSI প্যারামিটার কিছুটা শিথিল করে ট্রেডের সংখ্যা কমানো যেতে পারে।

- পজিশন যোগের সংখ্যা ও শতাংশের ভুল সেটিং অতিরিক্ত ট্রেডিংয়ের কারণ হতে পারে, তাই পুঁজি অনুযায়ী সাবধানে কনফিগার করা উচিত।

- বাজার যদি আরও কমতে থাকে এবং পজিশন যোগ করতে থাকে, তাহলে অসীম লোকসানের ঝুঁকি থাকতে পারে। পজিশন যোগের সর্বোচ্চ সংখ্যা আগেই নির্ধারণ করা উচিত এবং শেষ স্তরের যোগের শতাংশ রক্ষণশীল হওয়া উচিত।

- টেক প্রফিট শতাংশ খুব ছোট হলে অকালে টেক প্রফিট হতে পারে। ঐতিহাসিক ব্যাকটেস্ট ডেটার ভিত্তিতে উপযুক্ত টেক প্রফিট শতাংশ নির্ধারণ করা উচিত।

উন্নতির দিক

- MACD ইত্যাদি সূচক যোগ করে RSI সংকেত ফিল্টার করা যেতে পারে, ফলে অকার্যকর ট্রেড কমে।

- ATR ভিত্তিতে স্টপ লস সেট করা যেতে পারে, চরম বাজারের সময় বড় ক্ষতি এড়াতে।

- পজিশন যোগের সংখ্যা, শতাংশ, টেক প্রফিট শতাংশ ইত্যাদি প্যারামিটার অপ্টিমাইজ করে কৌশলটিকে বিভিন্ন সম্পদের জন্য আরও উপযোগী করা যেতে পারে।

- অস্থিরতার ভিত্তিতে টেক প্রফিট শতাংশ বুদ্ধিমত্তার সাথে সামঞ্জস্য করা যেতে পারে, উচ্চ অস্থিরতায় কিছুটা শিথিল করা।

সারসংক্ষেপ

কৌশলটি RSI সূচকের মাধ্যমে ওভারসোল্ড এলাকা চিহ্নিত করে এবং মুভিং এভারেজের সাথে মিলিয়ে রিভার্সাল ট্রেড করে। একই সাথে বুদ্ধিমত্তার সাথে পজিশন যোগ এবং প্রগ্রেসিভ টেক প্রফিট মেকানিজম ব্যবহার করে ঝুঁকি নিয়ন্ত্রণে রেখে দক্ষ লং কৌশল বাস্তবায়ন করে। সূচক প্যারামিটার, টেক প্রফিট মেকানিজম ইত্যাদি অপ্টিমাইজ করলে কৌশলটি আরও স্থিতিশীল ও দক্ষ হয়। এই কৌশলটি স্টক ইনডেক্স ফিউচার, ক্রিপ্টোকারেন্সি ইত্যাদি ট্রেন্ড রিভার্সাল বৈশিষ্ট্যযুক্ত আর্থিক সম্পদে ব্যাপকভাবে প্রয়োগ করা যেতে পারে এবং এর বাস্তব বিনিয়োগ মূল্য রয়েছে।

- 1