RSI দ্বৈত ট্র্যাক অসিলেশন লাইন দীর্ঘ-সংক্ষিপ্ত দ্বিমুখী ট্রেডিং কৌশল

সারসংক্ষেপ

RSI ডুয়েল-রেল অসিলেটর দীর্ঘ-সংক্ষিপ্ত দ্বি-মুখী ট্রেডিং স্ট্র্যাটেজি হল একটি কৌশল যা RSI সূচক ব্যবহার করে দ্বি-মুখী ট্রেডিং পরিচালনা করে। এই কৌশলটি RSI সূচকের ওভারবট/ওভারসল্ড নীতি, ডুয়েল-রেল সেটিং এবং চলমান গড় ট্রেডিং সিগন্যালের সমন্বয়ে কার্যকরভাবে দ্বি-মুখী পজিশন খোলা ও বন্ধ করে।

কৌশলের নীতি

এই কৌশলটি প্রধানত RSI সূচকের ওভারবট/ওভারসল্ড নীতির উপর ভিত্তি করে ট্রেডিং সিদ্ধান্ত নেয়। কৌশলটি প্রথমে RSI সূচকের মান vrsi এবং ডুয়েল-রেলের উপরের রেল sn ও নিচের রেল ln গণনা করে। যখন RSI মান নিচের রেল ln কে নিচে ভেদ করে, তখন লং সিগন্যাল তৈরি হয়, এবং যখন RSI মান উপরের রেল sn কে উপরে ভেদ করে, তখন শর্ট সিগন্যাল তৈরি হয়।

কৌশলটি ক্যান্ডেলস্টিকের উত্থান-পতনও শনাক্ত করে, যার ফলে আরও লং/শর্ট সিগন্যাল তৈরি হয়। বিশেষত, যখন ক্যান্ডেলটি নিচ থেকে উপরে ভেদ করে, তখন লং সিগন্যাল longLogic তৈরি হয়, এবং যখন ক্যান্ডেলটি উপরে থেকে নিচে ভেদ করে, তখন শর্ট সিগন্যাল shortLogic তৈরি হয়। এছাড়াও, কৌশলটি প্যারামিটার সুইচ সরবরাহ করে, যার মাধ্যমে শুধু লং, শুধু শর্ট বা সিগন্যাল ফ্লিপ করা যায়।

লং/শর্ট সিগন্যাল তৈরি হওয়ার পর, কৌশলটি সিগন্যালের সংখ্যা গণনা করে এবং পজিশন খোলার সংখ্যা নিয়ন্ত্রণ করে। প্যারামিটারের মাধ্যমে বিভিন্ন অ্যাডিং নিয়ম সেট করা যায়। বন্ধ করার শর্তগুলির মধ্যে রয়েছে টেক প্রফিট, স্টপ লস, ট্রেইলিং স্টপ লস ইত্যাদি, এবং বিভিন্ন টেক প্রফিট/স্টপ লস শতাংশ সেট করা যায়।

সংক্ষেপে, কৌশলটি RSI সূচক, মুভিং অ্যাভারেজ ক্রসওভার, পরিসংখ্যানগত অ্যাডিং, টেক প্রফিট/স্টপ লস ইত্যাদি বিভিন্ন প্রযুক্তিগত পদ্ধতি সমন্বয় করে স্বয়ংক্রিয় দীর্ঘ-সংক্ষিপ্ত দ্বি-মুখী ট্রেডিং পরিচালনা করে।

কৌশলের সুবিধা

- RSI সূচকের ওভারবট/ওভারসল্ড নীতি ব্যবহার করে যুক্তিসঙ্গত অবস্থানে লং ও শর্ট পজিশন তৈরি করে।

- ডুয়েল-রেল সেটিং ভুল সিগন্যাল এড়াতে সাহায্য করে। উপরের রেল লং পজিশনের অকাল বন্ধ রোধ করে, নিচের রেল শর্ট পজিশনের অকাল বন্ধ রোধ করে।

- মুভিং অ্যাভারেজ ট্রেডিং সিগন্যাল মিথ্যা ব্রেকআউট ফিল্টার করে। দাম শুধুমাত্র মুভিং অ্যাভারেজ ভেদ করলেই সিগন্যাল তৈরি হয়, যা মিথ্যা সিগন্যাল এড়ায়।

- সিগন্যালের সংখ্যা এবং অ্যাডিং সংখ্যা গণনা করে, ঝুঁকি নিয়ন্ত্রণ করে।

- কাস্টমাইজযোগ্য টেক প্রফিট/স্টপ লস শতাংশ, লাভ-ঝুঁকি নিয়ন্ত্রণযোগ্য।

- ট্রেইলিং স্টপ লস লাভ আরও লক করতে সহায়তা করে।

- শুধু লং, শুধু শর্ট বা সিগন্যাল ফ্লিপ করার বিকল্প, বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নেওয়া যায়।

- স্বয়ংক্রিয় ট্রেডিং সিস্টেম, মানুষের হস্তক্ষেপ কমায়।

কৌশলের ঝুঁকি

- RSI সূচকের বিপরীতমুখী হওয়ার ব্যর্থতার ঝুঁকি রয়েছে। RSI ওভারবট/ওভারসল্ড জোনে প্রবেশ করলেও বিপরীতমুখী নাও হতে পারে।

- নির্দিষ্ট টেক প্রফিট/স্টপ লস পয়েন্ট ফাঁদে পড়ার ঝুঁকি রয়েছে। ভুল সেটিং অকাল স্টপ লস বা টেক প্রফিটের কারণ হতে পারে।

- প্রযুক্তিগত সূচকের উপর নির্ভরশীল, প্যারামিটার অপ্টিমাইজেশনের ঝুঁকি বিদ্যমান। সূচক প্যারামিটারের ভুল সেটিং কৌশলের কার্যকারিতা প্রভাবিত করতে পারে।

- একাধিক শর্ত একসাথে ট্রিগার হলে, মিসড অর্ডারের ঝুঁকি থাকে।

- স্বয়ংক্রিয় ট্রেডিং সিস্টেমে অস্বাভাবিক ত্রুটির ঝুঁকি থাকে।

উপরের ঝুঁকিগুলো মোকাবেলায় প্যারামিটার সেটিং অপ্টিমাইজ করা, টেক প্রফিট/স্টপ লস কৌশল সামঞ্জস্য করা, লিকুইডিটি ফিল্টার যোগ করা, সিগন্যাল জেনারেশন লজিক অপ্টিমাইজ করা এবং অস্বাভাবিক ত্রুটি পর্যবেক্ষণ বৃদ্ধি করে উন্নতি করা যেতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- বিভিন্ন সময়কালের প্যারামিটার পরীক্ষা করে RSI সূচকের প্যারামিটার অপ্টিমাইজ করা।

- বিভিন্ন টেক প্রফিট/স্টপ লস শতাংশ সেটিং পরীক্ষা করা।

- ট্রেডিং ভলিউম বা রিটার্ন রেট ফিল্টার যোগ করে লিকুইডিটির অভাব এড়ানো।

- সিগন্যাল জেনারেশন লজিক অপ্টিমাইজ করা, মুভিং অ্যাভারেজ ক্রসওভার পদ্ধতি উন্নত করা।

- বিভিন্ন সময়ফ্রেমের ব্যাকটেস্টিং যোগ করে স্থিতিশীলতা যাচাই করা।

- অন্যান্য সূচক যোগ করে সিগন্যালের কার্যকারিতা অপ্টিমাইজ করার কথা বিবেচনা করা।

- পজিশন ম্যানেজমেন্ট কৌশল যোগ করা।

- অস্বাভাবিক ত্রুটি পর্যবেক্ষণ বৃদ্ধি করা।

- স্বয়ংক্রিয় স্টপ লস ট্র্যাকিং অ্যালগরিদম অপ্টিমাইজ করা।

- কৌশল উন্নত করতে মেশিন লার্নিং যুক্ত করার কথা বিবেচনা করা।

সারসংক্ষেপ

RSI ডুয়েল-রেল অসিলেটর দীর্ঘ-সংক্ষিপ্ত দ্বি-মুখী ট্রেডিং স্ট্র্যাটেজি RSI সূচক, পরিসংখ্যানগত পজিশন ওপেনিং এবং স্টপ লস নীতি ইত্যাদি বিভিন্ন প্রযুক্তিগত উপায়ের সমন্বয়ে স্বয়ংক্রিয় দ্বি-মুখী ট্রেডিং বাস্তবায়ন করে। এই কৌশলটি অত্যন্ত কাস্টমাইজযোগ্য; ব্যবহারকারীরা প্রয়োজন অনুযায়ী প্যারামিটার সামঞ্জস্য করে বিভিন্ন বাজার পরিবেশের সাথে খাপ খাইয়ে নিতে পারেন। তবে, কৌশলটির উন্নতির জায়গাও আছে; প্যারামিটার সেটিং, ঝুঁকি নিয়ন্ত্রণ কৌশল, সিগন্যাল জেনারেশন লজিক ইত্যাদি অপ্টিমাইজ করে কৌশলটিকে আরও স্থিতিশীল ও নির্ভরযোগ্য করা যেতে পারে। সামগ্রিকভাবে, কৌশলটি ব্যবহারকারীদের অপেক্ষাকৃত দক্ষ কোয়ান্টিটেটিভ ট্রেডিং সমাধান সরবরাহ করে।

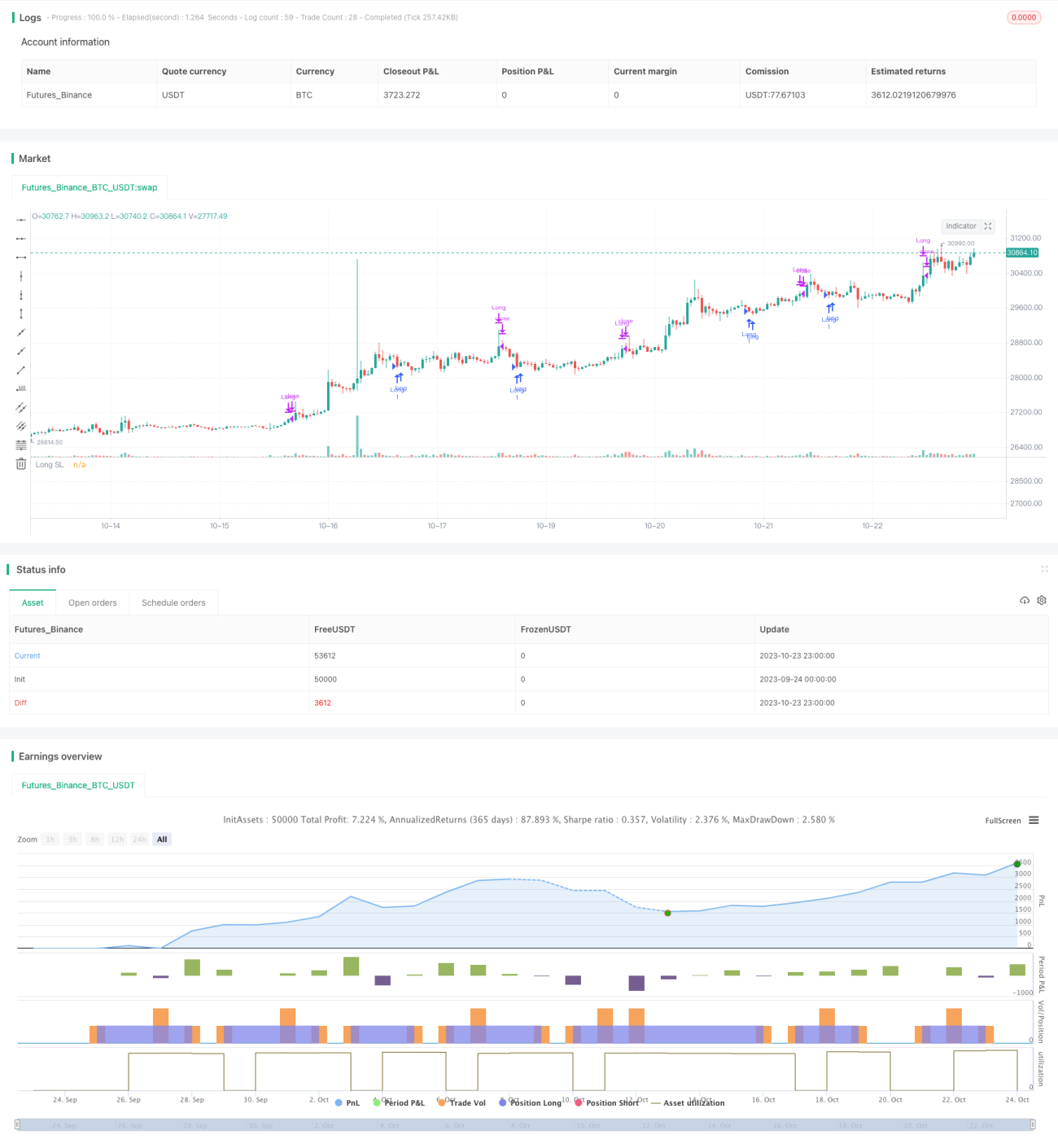

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1