সুপ্ত রেঞ্জ বিপরীতকরণ কৌশল

সারসংক্ষেপ

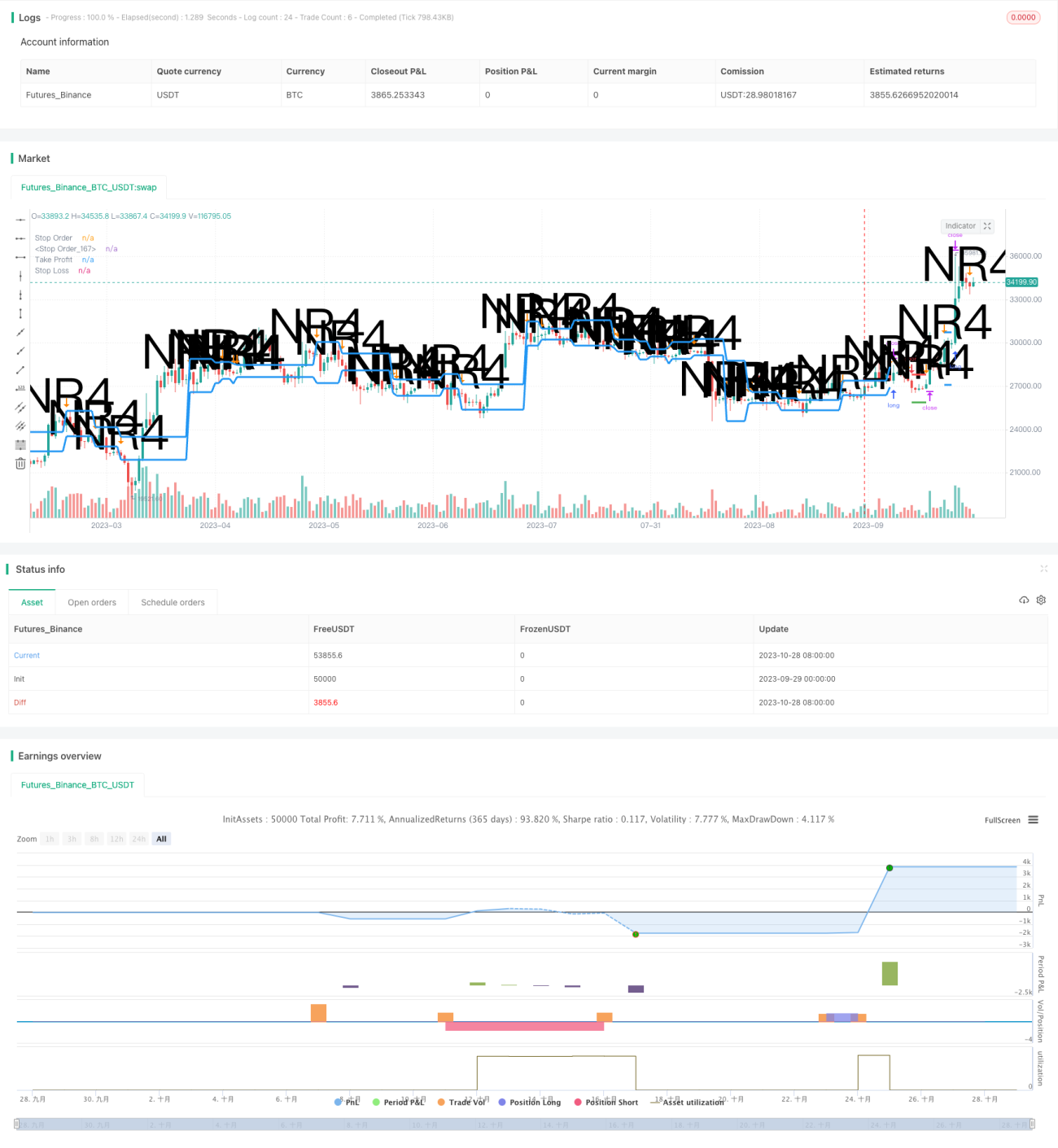

স্লিপিং রেঞ্জ রিভার্সাল স্ট্র্যাটেজি দামের অস্থিরতা হ্রাসের সময়কালকে পজিশন খোলার সংকেত হিসাবে ব্যবহার করে এবং দামের অস্থিরতা যখন পুনরায় বাড়তে শুরু করে তখন লাভের জন্য পজিশন বন্ধ করে। এটি সংকীর্ণ সীমার মধ্যে দাম সীমাবদ্ধ থাকার সময় (স্লিপিং রেঞ্জ) চিহ্নিত করে আসন্ন মূল্য প্রবণতা ধারণ করার চেষ্টা করে। এই কৌশলটি সাধারণত তখন প্রযোজ্য হয় যখন বর্তমান অস্থিরতা কম কিন্তু ভবিষ্যতে বিস্ফোরণের সম্ভাবনা থাকে।

কৌশলের মূলনীতি

কৌশলটি প্রথমে স্লিপিং রেঞ্জ শনাক্ত করে, অর্থাৎ এমন পরিস্থিতি যেখানে দাম পূর্ববর্তী ট্রেডিং দিনের মূল্য পরিসরের মধ্যে সীমাবদ্ধ থাকে। এটি নির্দেশ করে যে বর্তমান অস্থিরতা আগের কয়েক দিনের তুলনায় কমে গেছে। আমরা বর্তমান ট্রেডিং দিনের সর্বোচ্চ দাম n দিন আগের (সাধারণত 4 দিন) সর্বোচ্চ দামের সাথে এবং বর্তমান ট্রেডিং দিনের সর্বনিম্ন দাম n দিন আগের সর্বনিম্ন দামের সাথে তুলনা করে স্লিপিং রেঞ্জের শর্ত পূরণ হয়েছে কিনা তা নির্ধারণ করি।

স্লিপিং রেঞ্জ নিশ্চিত হওয়ার পরে, কৌশলটি একই সাথে দুটি পেন্ডিং অর্ডার রাখে: একটি ক্রয় অর্ডার রেঞ্জের উচ্চ পয়েন্টের কাছাকাছি এবং একটি বিক্রয় অর্ডার রেঞ্জের নিম্ন পয়েন্টের কাছাকাছি। এরপর অপেক্ষা করা হয় দাম স্লিপিং রেঞ্জ ভেঙে উপরে বা নিচে চলতে থাকবে কিনা। যদি দাম উপরের দিকে ভেঙে যায়, ক্রয় অর্ডার ট্রিগার হয়ে লং পজিশন স্থাপন করে; যদি নিচের দিকে ভেঙে যায়, বিক্রয় অর্ডার ট্রিগার হয়ে শর্ট পজিশন স্থাপন করে।

পজিশন স্থাপনের পর, কৌশলটি স্টপ-লস এবং টেক-প্রফিট অর্ডার সেট করে। স্টপ-লস নিচের দিকের ঝুঁকি সীমিত করে, এবং টেক-প্রফিট লাভ হওয়ার পর পজিশন বন্ধ করতে ব্যবহৃত হয়। স্টপ-লস এন্ট্রি মূল্য থেকে একটি নির্দিষ্ট অনুপাত দূরে থাকে, যা ঝুঁকি ব্যবস্থাপনা প্যারামিটার দ্বারা নির্ধারিত হয়; টেক-প্রফিট এন্ট্রি মূল্য থেকে স্লিপিং রেঞ্জের আকার সমান দূরে থাকে, কারণ আমরা আশা করি দামের চলাচলের পরিমাণ পূর্বের অস্থিরতার সমান হবে।

পরিশেষে, কৌশলটিতে একটি অর্থ ব্যবস্থাপনা মডিউল অন্তর্ভুক্ত রয়েছে। ফিক্সড ফ্র্যাকশনাল পদ্ধতি ব্যবহার করে অর্ডারের ট্রেডিং মূলধনের পরিমাণ সমন্বয় করা হয়, যাতে লাভের সময় মূলধনের ব্যবহার বাড়ে এবং ক্ষতির সময় ঝুঁকি কমে।

সুবিধা বিশ্লেষণ

এই কৌশলটির নিম্নলিখিত সুবিধা রয়েছে:

- অস্থিরতা হ্রাসের সময়কে পজিশন খোলার সংকেত হিসাবে ব্যবহার করে দামের প্রবণতা শুরু হওয়ার আগেই সুযোগ গ্রহণ করা যায়।

- একই সময়ে লং এবং শর্ট উভয় দিকের ট্রেড অর্ডার সেট করে, ঊর্ধ্বগামী বা নিম্নগামী উভয় প্রবণতাই ক্যাপচার করা যায়।

- স্টপ-লস এবং টেক-প্রফিট কৌশল ব্যবহার করে একক ট্রেডের ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করা যায়।

- ফিক্সড ফ্র্যাকশনাল মানি ম্যানেজমেন্ট পদ্ধতি প্রয়োগ করে মূলধনের ব্যবহার দক্ষতা বাড়ানো যায়।

- কৌশলটির যুক্তি সহজ ও স্পষ্ট, বাস্তবায়ন করা সহজ।

ঝুঁকি বিশ্লেষণ

কৌশলটির কিছু ঝুঁকি সম্পর্কেও সচেতন থাকা প্রয়োজন:

- স্লিপিং রেঞ্জ ভাঙার দিক ভুল হওয়ার ঝুঁকি। দাম স্পষ্টভাবে উপর বা নিচে ভাঙতে পারে না, ফলে ভুল দিকে পজিশন খোলা হতে পারে।

- ভাঙার পর দিকনির্দেশনামূলক চলাচল অব্যাহত না থাকার ঝুঁকি। ভাঙনটি শুধুমাত্র স্বল্পমেয়াদী রিভার্সাল হতে পারে।

- স্টপ-লস ভেঙে যাওয়ার ঝুঁকি। বড় মূল্য আন্দোলন সরাসরি স্টপ-লস লাইন অতিক্রম করতে পারে।

- ফিক্সড ফ্র্যাকশনাল পদ্ধতিতে পজিশন বাড়ালে ক্ষতি বড় হওয়ার ঝুঁকি। ফিক্সড ফ্র্যাকশন মান কমিয়ে ঝুঁকি কমানো যায়।

- প্যারামিটার অনুপযুক্ত সেটিং করলে কৌশলের কার্যকারিতা কমে যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

কৌশলটি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

- ভুল ভাঙন এড়াতে ভাঙন ডাইভারজেন্সের মতো ফিল্টার সিগন্যাল যুক্ত করা।

- স্টপ-লস কৌশল উন্নত করা, যেমন ট্রেলিং স্টপ-লস, পেন্ডিং অর্ডার স্টপ-লস ইত্যাদি।

- ট্রেন্ড নির্ধারণের সূচক যোগ করা, ভুল রিভার্সাল এন্ট্রি এড়ানো।

- ফিক্সড ফ্র্যাকশন মান অপ্টিমাইজ করা, লাভ-ক্ষতির অনুপাত ভারসাম্য রাখা।

- একাধিক টাইমফ্রেম বিশ্লেষণ যুক্ত করে লাভের সম্ভাবনা বাড়ানো।

- মেশিন লার্নিং পদ্ধতি ব্যবহার করে প্যারামিটার স্বয়ংক্রিয়ভাবে অপ্টিমাইজ করা।

সারমর্ম

স্লিপিং রেঞ্জ রিভার্সাল স্ট্র্যাটেজির সামগ্রিক ধারণা স্পষ্ট এবং এটি কিছু লাভজনক সম্ভাবনা রাখে। প্যারামিটার অপ্টিমাইজেশন, ঝুঁকি ব্যবস্থাপনা, সিগন্যাল ফিল্টারিং ইত্যাদি মাধ্যমে কৌশলের স্থিতিশীলতা আরও বাড়ানো যেতে পারে। তবে যেকোনো ট্রেন্ড রিভার্সাল কৌশলেরই কিছু ঝুঁকি থাকে, তাই সাবধানতার সাথে ব্যবহার করতে হবে এবং পজিশনের আকার যথাযথভাবে সামঞ্জস্য করতে হবে। এই কৌশলটি রিভার্সাল অপারেশনে অভিজ্ঞ এবং ঝুঁকি সচেতন ট্রেডারদের জন্য উপযুক্ত।

- 1