বহুমুখী ট্রেন্ড কৌশল

সারসংক্ষেপ

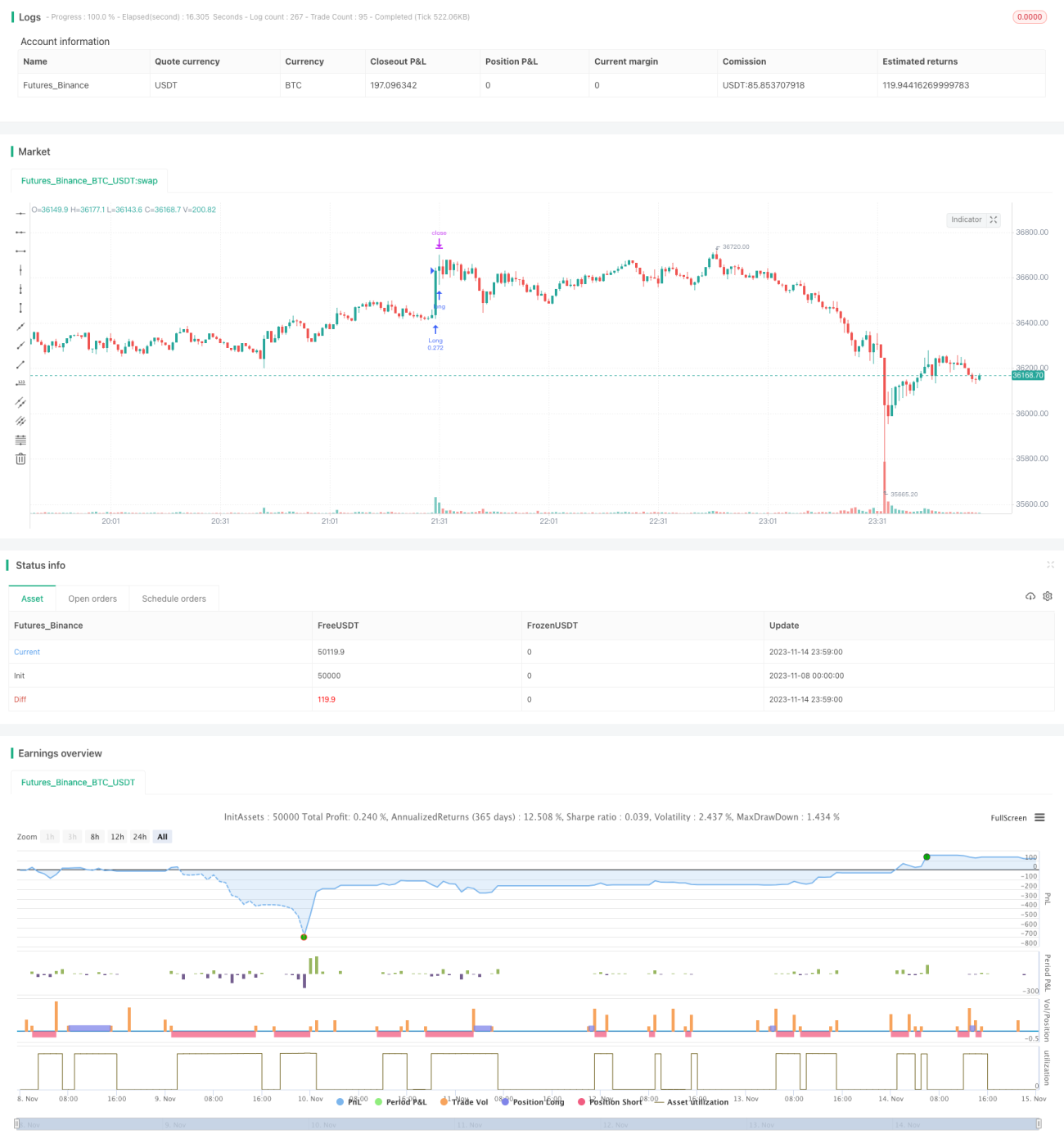

এই কৌশলটি বিভিন্ন সূচক ব্যবহার করে প্রবণতার দিক নির্ধারণ করে এবং মিড-শর্ট টার্মে ট্রেন্ড ফলোয়ার পদ্ধতিতে সুযোগ ধরার চেষ্টা করে। কৌশলটি বিশেষভাবে ট্রেন্ড অনুসরণের জন্য ডিজাইন করা হয়েছে, যার লক্ষ্য জয়ের হার বৃদ্ধি এবং ড্রডাউন কমানো।

কৌশলের নীতি

-

মূল্যের অনুপাত নির্ধারণ করতে WVAP সূচক ব্যবহার করা;

-

মাল্টি-বিয়ারিশ মোমেন্টাম নির্ধারণ করতে RSI সূচক;

-

মূল্যের ব্রেকআউট শনাক্ত করতে QQE সূচক;

-

ট্রেন্ডের শক্তি নির্ধারণ করতে ADX সূচক;

-

মৌলিক প্রবণতা নির্ধারণ করতে Coral Trend Indicator;

-

ট্রেন্ড সহায়তা নির্ধারণ করতে LSMA সূচক;

-

একাধিক সূচকের সংকেত একত্রিত করে ট্রেডিং সিগন্যাল জারি করা।

এই কৌশলটি প্রধানত RSI, QQE, ADX এর মতো একাধিক সূচকের মাধ্যমে ট্রেন্ডের দিক এবং শক্তি নির্ধারণ করে এবং Coral Trend Indicator-এর কার্ভকে মৌলিক প্রবণতার মানদণ্ড হিসাবে ব্যবহার করে। যখন RSI-এর মতো সূচকগুলি ক্রয় সংকেত দেয় এবং Coral Trend Indicator-ও ঊর্ধ্বগামী কার্ভ দেখায়, তখন উচ্চ সম্ভাবনায় ট্রেন্ড ঊর্ধ্বমুখী হওয়ায় কৌশলটি ক্রয়ের সিদ্ধান্ত নেয়। WVAP-এর মতো সূচকগুলি মূলত মূল্য যুক্তিসঙ্গত কিনা তা নির্ধারণ করতে ব্যবহৃত হয়, যাতে উচ্চ মূল্যে ক্রয় এড়ানো যায়।

কৌশলের সুবিধা

-

একাধিক সূচকের সমন্বয়, নির্ধারণের যথার্থতা বৃদ্ধি;

-

ট্রেন্ড ফলোয়ার পদ্ধতির উপর জোর, লাভের সম্ভাবনা বাড়ানো;

-

ব্রেকআউট চিন্তাভাবনা ব্যবহার করে ট্রেডিং রেঞ্জের বাজার ফিল্টার করা;

-

মৌলিক সূচক অন্তর্ভুক্ত করে কনট্রারিয়ান ট্রেডিং এড়ানো;

-

ট্রেডিং সময় এবং লট সাইজ যুক্তিসঙ্গতভাবে নির্ধারণ, ঝুঁকি কমানো;

-

কৌশলটির চিন্তাভাবনা পরিষ্কার, সহজে বোঝা এবং অপ্টিমাইজ করা যায়।

এই কৌশলের সবচেয়ে বড় সুবিধা হলো একাধিক সূচকের সমন্বয়, যা কিছু পরিমাণে একক সূচকের ভুল নির্ধারণের সম্ভাবনা কমাতে পারে এবং নির্ধারণের যথার্থতা বাড়াতে পারে। একইসাথে ট্রেন্ড ফলোয়ার এবং ব্রেকআউট চিন্তাভাবনার উপর জোর দেওয়ার ফলে নির্ভরযোগ্য মিড-শর্ট টার্ম সুযোগ চিহ্নিত করতে সহায়তা করে। তাছাড়া, কৌশলে মৌলিক সূচক যুক্ত থাকায় কনট্রারিয়ান কার্যক্রম এড়ানো যায়। এই সব নকশা কৌশলের স্থিতিশীলতা এবং লাভের সম্ভাবনা বাড়ায়।

কৌশলের ঝুঁকি

-

লং-শর্ট নির্ধারণে সময় লেগে যেতে পারে, ফলে সেরা এন্ট্রির সময় হাতছাড়া হতে পারে;

-

ড্রডাউন নিয়ন্ত্রণ যথাযথ নয়, বড় ড্রডাউনের ঝুঁকি থাকে;

-

যখন মৌলিক অবস্থায় পরিবর্তন আসে, কৌশলটি সংকেত মিস করতে পারে;

-

ট্রেডিং খরচ বিবেচনা করা হয়নি, বাস্তব প্রয়োগে মুনাফা কমার ঝুঁকি থাকে।

এই কৌশলের সবচেয়ে বড় ঝুঁকি হলো একাধিক সূচকের সমন্বয়ের ফলে নির্ধারণে দেরি হতে পারে, যার ফলে সেরা এন্ট্রির সময় হাতছাড়া হতে পারে এবং লাভের সম্ভাবনা কমে যায়। তাছাড়া, কৌশলের ড্রডাউন নিয়ন্ত্রণ আদর্শ নয়, বড় ড্রডাউনের ঝুঁকি থাকে। যখন বাজারের মৌলিক অবস্থায় পরিবর্তন আসে কিন্তু সূচকগুলি তা এখনো প্রতিফলিত করেনি, তখনও লোকসানের সম্ভাবনা থাকে। বাস্তব প্রয়োগে, ট্রেডিং খরচও মুনাফায় প্রভাব ফেলতে পারে।

কৌশল অপ্টিমাইজেশনের দিক

-

স্টপ-লস কৌশল যুক্ত করে ড্রডাউন নিয়ন্ত্রণ উন্নত করা;

-

প্যারামিটার সেটিংস অপ্টিমাইজ করে সূচক বিলম্ব কমানো;

-

মৌলিক সূচকের প্রয়োগ বাড়িয়ে যথার্থতা বৃদ্ধি;

-

মেশিন লার্নিং অ্যালগরিদম যুক্ত করে ডায়নামিক প্যারামিটার অপ্টিমাইজেশন বাস্তবায়ন।

এই কৌশলের অপ্টিমাইজেশনের মূল ফোকাস ড্রডাউন নিয়ন্ত্রণে হওয়া উচিত, যাতে ট্রেলিং স্টপ-লস কৌশল যুক্ত করে লাভ লক করা এবং ড্রডাউন কমানো যায়। একইসাথে প্যারামিটার সেটিংস অপ্টিমাইজ করে সূচক বিলম্ব কমানো এবং বাজারের পরিবর্তনের প্রতি সংবেদনশীলতা বাড়ানো সম্ভব। তাছাড়া, মৌলিক নির্ধারণের জন্য আরও সূচক অন্তর্ভুক্ত করে যথার্থতা বাড়ানো যায়। যদি মেশিন লার্নিং পদ্ধতি ব্যবহার করে প্যারামিটারের ডায়নামিক অপ্টিমাইজেশন বাস্তবায়ন করা যায়, তাহলে কৌশলের স্থিতিশীলতা ব্যাপকভাবে বৃদ্ধি পাবে।

উপসংহার

এই কৌশলটি বিভিন্ন সূচকের মাধ্যমে প্রবণতার দিক নির্ধারণ করে এবং ট্রেন্ড ফলোয়ার চিন্তাভাবনা অনুসরণ করে ডিজাইন করা হয়েছে, যার লক্ষ্য নির্ধারণের যথার্থতা বৃদ্ধি এবং লাভের সম্ভাবনা বাড়ানো। কৌশলটিতে একাধিক সূচকের সমন্বয়, ট্রেন্ড ফলোয়ারের উপর জোর, মৌলিক সূচক অন্তর্ভুক্তি ইত্যাদি সুবিধা থাকলেও ভুল নির্ধারণের বিলম্ব এবং ড্রডাউন নিয়ন্ত্রণের ঘাটতি ইত্যাদি সমস্যা রয়েছে। ভবিষ্যতে প্যারামিটার সেটিংস অপ্টিমাইজ করে, স্টপ-লস কৌশল উন্নত করে এবং মৌলিক সূচক বাড়িয়ে কৌশলটি সংশোধন করা যেতে পারে, যাতে বাস্তব প্রয়োগে আরও ভালো ফল পাওয়া যায়।

- 1