SAR-ভিত্তিক ট্রেন্ড ফলোয়িং কোয়ান্টিটেটিভ স্ট্র্যাটেজি

সংক্ষিপ্ত বিবরণ

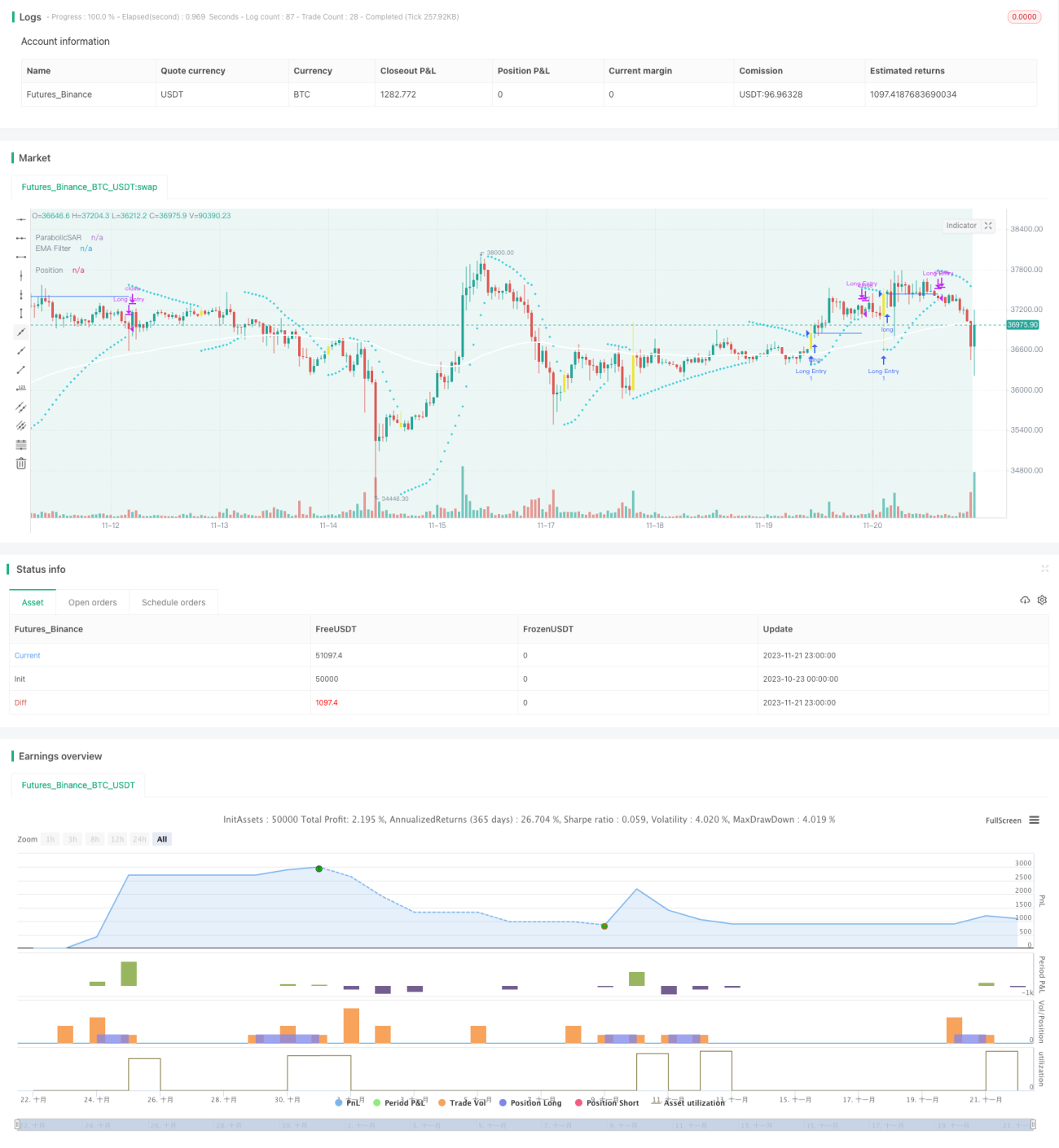

স্পেকুলেটিভ গ্যাপ কৌশলটি একটি ট্রেন্ড অনুসরণকারী কোয়ান্টিটেটিভ ট্রেডিং কৌশল। এটি প্রধান ট্রেডিং সিগন্যাল হিসেবে SAR স্মুথ (মসৃণ) কার্ভ ব্যবহার করে, সাথে EMA, স্কুইজ মোমেন্টাম এবং ভোলাটিলিটি অসিলেটরের মতো বিভিন্ন ফিল্টার ব্যবহার করা হয়। SAR প্যারামিটার কনফিগার করে ট্রেন্ড রিভার্সাল পয়েন্ট শনাক্ত করে এবং কম ঝুঁকিতে ট্রেন্ড অনুসরণ করে। এটি মধ্যম থেকে দীর্ঘমেয়াদী বিনিয়োগের জন্য একটি অত্যন্ত উপযোগী কৌশল।

কৌশলের নীতি

এই কৌশলটি প্রধান ট্রেডিং সিগন্যাল ইন্ডিকেটর হিসেবে প্যারাবোলিক SAR ব্যবহার করে। SAR কার্যকরভাবে দামের ট্রেন্ডের রিভার্সাল পয়েন্ট নির্ধারণ করতে পারে। যখন SAR চিহ্ন পরিবর্তিত হয়, তখন এর অর্থ ট্রেন্ডের দিক পরিবর্তন ঘটছে। এই কৌশল সাধারণত SAR উল্টে যাওয়ার সময় কেনা বা বিক্রির সিগন্যাল দেয়।

এছাড়াও, কৌশলটি SAR ব্রেকআউট অপশনও প্রদান করে। অর্থাৎ, SAR সম্পূর্ণভাবে উল্টে যাওয়ার আগেই যদি দাম শেষ SAR মান ভেঙে ফেলে, তাহলেও সিগন্যাল তৈরি হয়। এটি কৌশলের সংবেদনশীলতা আরও বাড়াতে সাহায্য করে।

ভুয়া সিগন্যাল ফিল্টার করার জন্য এই কৌশলে EMA, স্কুইজ মোমেন্টাম এবং ভোলাটিলিটি অসিলেটর – এই তিনটি সহায়ক ফিল্টার অন্তর্ভুক্ত আছে। এগুলি পৃথকভাবে বা একত্রে ব্যবহার করা যেতে পারে, যাতে দামের ট্রেন্ড এবং ট্রেডিং সিগন্যালের নির্ভরযোগ্যতা নিশ্চিত করা যায়।

অবশেষে, কৌশলটি তিন ধরনের স্টপ-লস ও টেক-প্রফিট পদ্ধতি প্রদান করে: ফিক্সড স্টপ-লস, ফিক্সড টেক-প্রফিট এবং রিস্ক-রিওয়ার্ড রেশিও স্টপ-লস।这使得 kৌশলটি বিভিন্ন ধরণের ট্রেডিং পণ্যের বৈশিষ্ট্যের সাথে নমনীয়ভাবে খাপ খাইয়ে নিতে পারে।

সুবিধা বিশ্লেষণ

-

SAR সঠিকভাবে দামের ট্রেন্ড রিভার্সাল নির্ধারণ করতে পারে এবং নতুন দামের ট্রেন্ড দ্রুত ধরে নিতে পারে, যা মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড অনুসরণের জন্য উপযুক্ত।

-

একাধিক ফিল্টার সেটিং ভুয়া ব্রেকআউটের সম্ভাবনা কমায় এবং সিগন্যালের নির্ভরযোগ্যতা বাড়ায়।

-

কনফিগারেশন সহজ এবং নমনীয়, বিভিন্ন ট্রেডিং পণ্যের জন্য কাস্টমাইজযোগ্য প্যারামিটার ব্যবহার করা যায়।

-

একাধিক টেক-প্রফিট ও স্টপ-লস পদ্ধতি প্রদান করে, যা ঝুঁকি-প্রত্যাশার সমতা বজায় রাখতে সাহায্য করে।

-

সরাসরি ট্রেডিং বটের সাথে সংযোগ করে স্বয়ংক্রিয় ট্রেডিং সম্পন্ন করা যায়।

ঝুঁকি বিশ্লেষণ

-

নন-ট্রেন্ডিং বাজারে, ভুয়া সিগন্যাল এবং অকার্যকর ট্রেডের সংখ্যা বাড়তে পারে।

-

SAR প্যারামিটার ভুল সেট করলে সিগন্যাল নির্ণয়ের নির্ভুলতা প্রভাবিত হতে পারে।

-

ট্রেন্ড অনুসরণকারী কৌশল হওয়ায়, তীব্র ওঠানামার বাজারে স্টপ-লসে আঘাত লাগার সম্ভাবনা বেশি।

উপরোক্ত ঝুঁকিগুলি মোকাবেলায়, SAR প্যারামিটার বা ফিল্টার প্যারামিটার যথাযথভাবে সামঞ্জস্য করে অকার্যকর ট্রেডের সম্ভাবনা কমানো যেতে পারে। অথবা স্টপ-লস সীমা কিছুটা শিথিল করে বড় বাজার ওঠানামা সহ্য করা যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

-

SAR প্যারামিটার অপ্টিমাইজেশন। ঐতিহাসিক ব্যাকটেস্ট ডেটার মাধ্যমে SAR-এর স্টেপ এবং ইনক্রিমেন্ট প্যারামিটার অপ্টিমাইজ করে আরও স্থিতিশীল ও কার্যকর ট্রেডিং কৌশল পাওয়া যেতে পারে।

-

ট্রেন্ড নির্ধারণকারী ইন্ডিকেটর যোগ করা। কৌশলে MACD, DMI ইত্যাদি সহায়ক ইন্ডিকেটর যুক্ত করে ট্রেন্ড নির্ণয়ের ক্ষমতা বাড়ানো যেতে পারে।

-

ঝুঁকি-প্রত্যাশা অনুপাত অপ্টিমাইজ করা। ফিক্সড টেক-প্রফিট ও স্টপ-লস শতাংশ এবং ঝুঁকি-প্রত্যাশা অনুপাত প্যারামিটার সামঞ্জস্য করে উচ্চতর লাভের জন্য適當 বেশি ঝুঁকি নেওয়া যেতে পারে।

-

ফরেক্স পণ্য যোগ করা। বর্তমানে কৌশলটি শুধুমাত্র ক্রিপ্টোকারেন্সি ট্রেডিং সমর্থন করে, যা ফরেক্স, কমোডিটি এবং সিকিউরিটিজ বাজারেও সম্প্রসারিত করা যেতে পারে।

উপসংহার

স্পেকুলেটিভ গ্যাপ একটি অত্যন্ত কার্যকর ট্রেন্ড-ফলোয়িং কোয়ান্ট কৌশল। এটি দ্রুত সাড়া দেয়, সিগন্যাল নির্ভরযোগ্য হয় এবং স্টপ-লস ও টেক-প্রফিট ব্যবস্থাপনার মাধ্যমে দীর্ঘমেয়াদী স্থিতিশীল লাভ অর্জন করা যায়। উপযুক্ত প্যারামিটার ও নিয়ম অপ্টিমাইজেশন কৌশলটির কার্যকারিতা আরও বাড়াতে পারে। এটি দীর্ঘমেয়াদী ব্যবহারের জন্য একটি দক্ষ কোয়ান্ট কৌশল।

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//VERSION =================================================================================================================

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// This strategy is intended to study.- 1