মাল্টি-ফ্যাক্টর RSI রিভার্সাল স্ট্র্যাটেজি

সংক্ষিপ্ত বিবরণ

এই কৌশলটি RSI নির্দেশক ব্যবহার করে অতিরিক্ত ক্রয় ও অতিরিক্ত বিক্রয় শনাক্ত করে এবং MACD, Stochastic নির্দেশকের মতো একাধিক সহায়ক ফ্যাক্টরের সঙ্গে মিলিয়ে প্রবেশ করে। এই কৌশলটি স্বল্পমেয়াদী বিপরীতমুখী সুযোগ ধরা এবং এটি একটি বিপরীত কৌশল।

কৌশলের মূলনীতি

এই কৌশলটি মূলত RSI নির্দেশক ব্যবহার করে বাজার অতিরিক্ত ক্রয় বা অতিরিক্ত বিক্রয় অবস্থায় আছে কিনা তা বিচার করে। যখন RSI নির্দেশক নির্ধারিত অতিরিক্ত ক্রয় রেখা অতিক্রম করে, তখন বাজার সম্ভবত অতিরিক্ত ক্রয় অবস্থায় থাকে, তখন কৌশলটি শর্ট করার পছন্দ করে; যখন RSI নির্দেশক নির্ধারিত অতিরিক্ত বিক্রয় রেখার নিচে চলে যায়, তখন বাজার সম্ভবত অতিরিক্ত বিক্রয় অবস্থায় থাকে, তখন কৌশলটি লং করার পছন্দ করে। এইভাবে বাজার যখন একটি চরম অবস্থা থেকে অন্য চরম অবস্থায় বিপরীতমুখী পরিবর্তনের সময়ে উৎপন্ন স্বল্পমেয়াদী ট্রেডিং সুযোগ ধরে লাভ করা হয়।

এছাড়াও, কৌশলটি MACD, Stochastic এর মতো একাধিক সহায়ক ফ্যাক্টরও অন্তর্ভুক্ত করে। এই সহায়ক ফ্যাক্টরগুলির ভূমিকা হলো কিছু সম্ভাব্য ভুল ইতিবাচক ট্রেডিং সিগন্যাল ফিল্টার করা। শুধুমাত্র যখন RSI নির্দেশক একটি সিগন্যাল দেয় এবং সহায়ক ফ্যাক্টরও সেই সিগন্যালকে সমর্থন করে, তখনই কৌশলটি প্রকৃত ট্রেডিং পদক্ষেপ নেয়। এই বহু-ফ্যাক্টর সমন্বয় পদ্ধতি কৌশলের সিগন্যালের নির্ভরযোগ্যতা বাড়াতে পারে, ফলে কৌশলের স্থিতিশীলতাও উন্নত হয়।

সুবিধা বিশ্লেষণ

এই কৌশলের সবচেয়ে বড় সুবিধা হলো ক্যাপচারের দক্ষতা বেশি এবং বহু-ফ্যাক্টর যাচাইয়ের মাধ্যমে সিগন্যালের গুণমান উন্নত হয়েছে। বিশেষভাবে নিম্নলিখিত দিকগুলিতে প্রকাশ পায়:

- RSI নির্দেশক নিজেই বাজারের বিভিন্ন অবস্থা শনাক্ত করার ক্ষমতা较强, কার্যকরভাবে অতিরিক্ত ক্রয় ও অতিরিক্ত বিক্রয় শনাক্ত করতে পারে।

- একাধিক সহায়ক টুল ব্যবহার করে বহু-ফ্যাক্টর যাচাই, সিগন্যালের গুণমান উন্নত করে এবং প্রচুর ভুল ইতিবাচক সিগন্যাল ফিল্টার করে।

- কৌশলটি প্যারামিটারের প্রতি সংবেদনশীল নয়, সহজেই অপ্টিমাইজ করা যায়।

ঝুঁকি ও সমাধান

এই কৌশলটি কিছু নির্দিষ্ট ঝুঁকিরও মুখোমুখি হয়, প্রধানত দুটি দিকে:

- বিপরীতমুখী পরিবর্তন ব্যর্থ হওয়ার ঝুঁকি। বিপরীতমুখী সিগন্যাল নিজেই পরিসংখ্যানগত আর্ভিট্রেজ সুযোগের উপর নির্ভর করে, কিছু বিপরীতমুখী পরিবর্তন ব্যর্থ হওয়ার সম্ভাবনা থাকে না তা নয়। পজিশনের আকার কমিয়ে বা স্টপ লস সেট করে ঝুঁকি নিয়ন্ত্রণ করা যায়।

- বুলিশ বাজারে লোকসানের ঝুঁকি। কৌশলটি সামগ্রিকভাবে এখনও কাউন্টার-ট্রেন্ড অপারেশন প্রধান, বুলিশ বাজারে কিছু লোকসান অনিবার্য। এর জন্য আমাদের বড় প্রবণতা সম্পর্কে সঠিক বিচার করতে হবে, প্রয়োজন হলে মানব হস্তক্ষেপের মাধ্যমে প্রতিকূল বাজার পরিবেশ এড়িয়ে যেতে হবে।

অপ্টিমাইজেশনের দিকনির্দেশনা

এই কৌশলটি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করতে হবে:

- বিভিন্ন পণ্য পরীক্ষা করে সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করা। কৌশলটি প্যারামিটারের প্রতি সংবেদনশীল নয়, তবে বিভিন্ন পণ্যের জন্য সর্বোত্তম প্যারামিটার খুঁজে বের করার পরামর্শ দেওয়া হয়।

- অভিযোজিত প্রস্থান প্রক্রিয়া যোগ করা। ডায়নামিক স্টপ লস, টাইম-আউট প্রস্থান ইত্যাদি পদ্ধতি পরীক্ষা করা যেতে পারে, যাতে কৌশলটি বাজারের পরিবর্তনের সাথে আরও খাপ খাইয়ে নিতে পারে।

- মেশিন লার্নিং অ্যালগরিদম অন্তর্ভুক্ত করা। মডেলকে বিপরীতমুখী পরিবর্তনের সাফল্যের সম্ভাবনা বিচার করতে শেখানোর চেষ্টা করা যেতে পারে, ফলে কৌশলের জয়ের হার বাড়ে।

সারসংক্ষেপ

সামগ্রিকভাবে এই কৌশলটি একটি স্বল্পমেয়াদী বিপরীতমুখী কৌশল। RSI নির্দেশকের অতিরিক্ত ক্রয় ও বিক্রয় শনাক্ত করার ক্ষমতা ব্যবহার করে এবং একাধিক সহায়ক টুলের মাধ্যমে বহু-ফ্যাক্টর যাচাই করে, ফলে সিগন্যালের গুণমান উন্নত হয়। এই কৌশলের ক্যাপচারের দক্ষতা বেশি এবং স্থিতিশীলতাও ভালো। আরও পরীক্ষা ও অপ্টিমাইজেশন করে শেষ পর্যন্ত লাভজনক করা যেতে পারে।

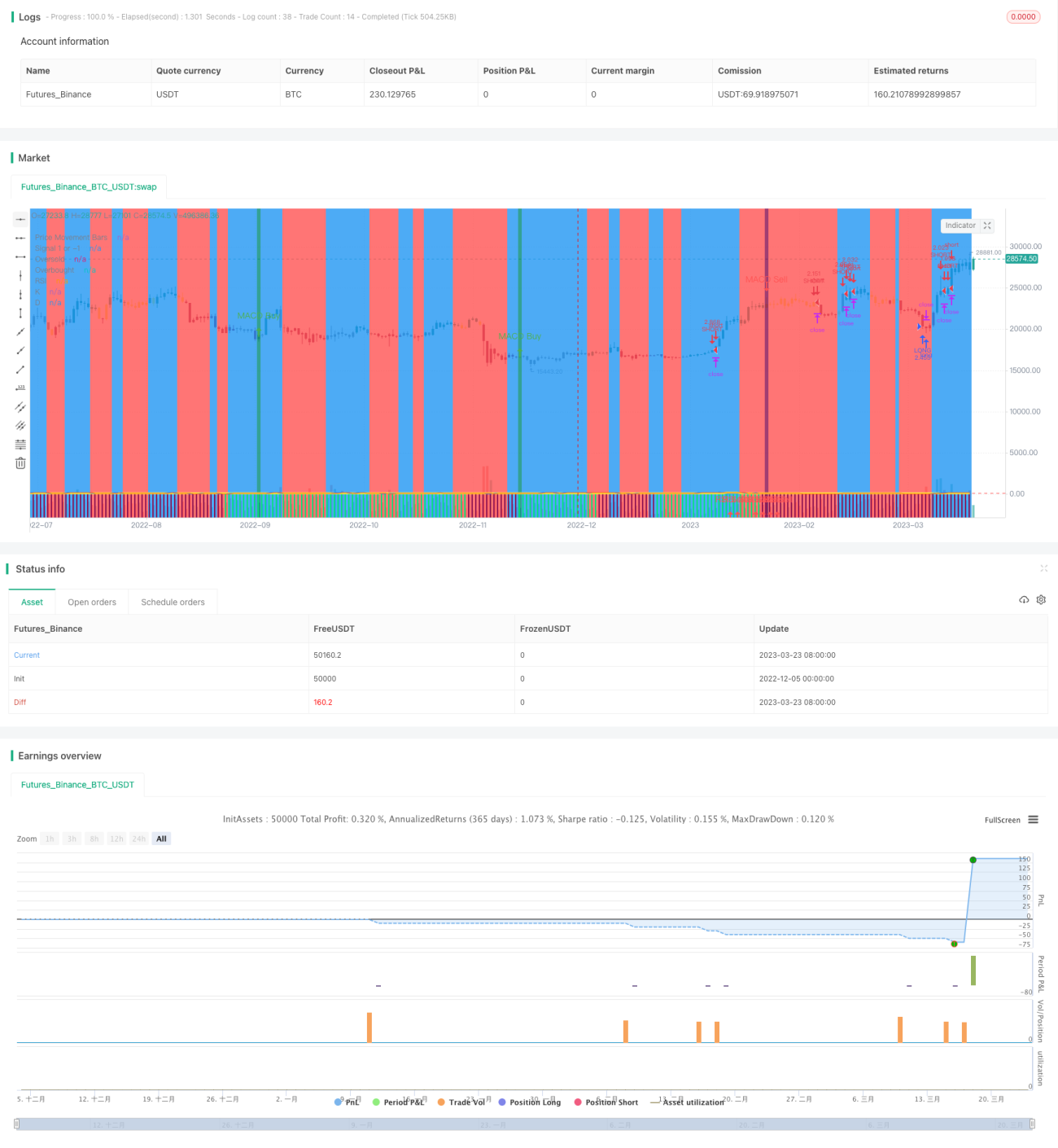

/*backtest

start: 2022-12-05 00:00:00

end: 2023-03-24 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='Ain1',title='All in One Strategy', overlay=true, initial_capital = 1000, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.18, calc_on_every_tick=true)- 1