মূল্য পরিবর্তনের হার ও মুভিং এভারেজের উপর ভিত্তি করে কোয়ান্টিটেটিভ স্ট্রাটেজি

সারসংক্ষেপ

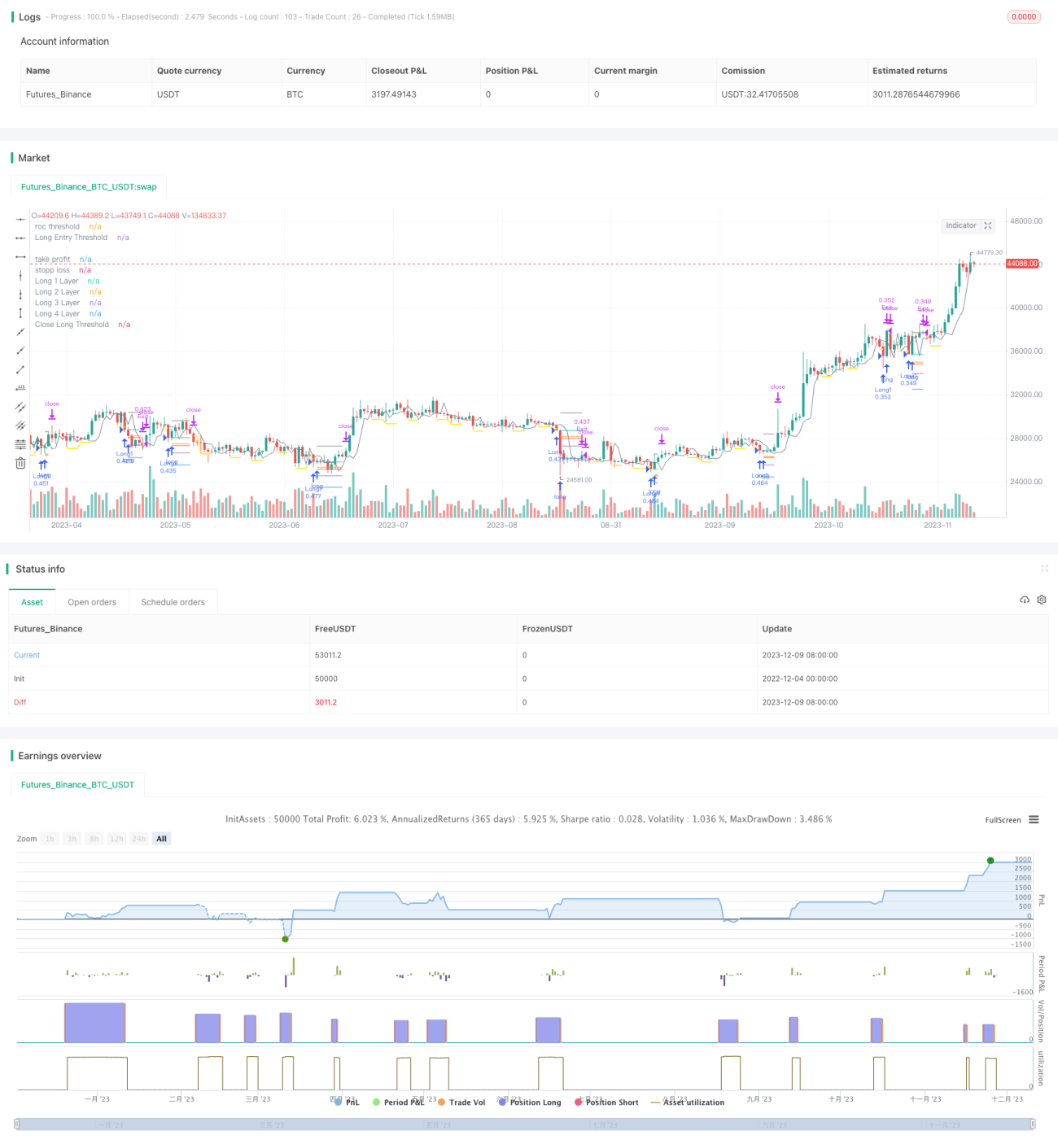

এই কৌশলটি মূল্য পরিবর্তনের হার এবং মুভিং এভারেজের প্রযুক্তিগত সূচকগুলিকে একত্রিত করে ক্রয় ও বিক্রয় পয়েন্টের সঠিক অবস্থান নির্ধারণ করে। যখন মূল্য উল্লেখযোগ্যভাবে হ্রাস পায়, তখন একটি ক্রয় থ্রেশহোল্ড স্থাপন করা হয় এবং আরও পতনের সময় লং পজিশন খোলা হয়; যখন মূল্য বৃদ্ধি পায়, তখন একটি বিক্রয় থ্রেশহোল্ড স্থাপন করা হয় এবং ক্রমাগত বৃদ্ধির সময় অবস্থান বন্ধ করা হয়। এছাড়াও, কৌশলটি পিরামিডিং পদ্ধতি ব্যবহার করে, একাধিকবার ক্রয় করে খরচ কমায়।

কৌশলের নীতি

ক্রয় লজিক

- মূল্য পরিবর্তনের হার (ROC) গণনা করুন এবং ক্রয় থ্রেশহোল্ড লাইন নির্ধারণ করুন।

- যখন মূল্য ক্রয় থ্রেশহোল্ড লাইনের নিচে নেমে যায়, তখন সেই পয়েন্টটি রেকর্ড করুন এবং ক্রয় সীমিত লাইন শুরু করুন।

- ক্রয় সীমিত লাইন ইনপুট প্যারামিটার অনুযায়ী একটি নির্দিষ্ট সময়কালের জন্য সক্রিয় থাকে, মেয়াদ শেষ হলে বন্ধ হয়ে যায়।

- যখন মূল্য আরও হ্রাস পেয়ে ক্রয় সীমিত লাইনের নিচে নেমে যায়, তখন প্রথম লং পজিশন খোলা হয়।

বিক্রয় লজিক

- মূল্য পরিবর্তনের হার (ROC) গণনা করুন এবং বিক্রয় থ্রেশহোল্ড লাইন নির্ধারণ করুন।

- যখন মূল্য বিক্রয় থ্রেশহোল্ড লাইনের উপরে উঠে যায়, তখন সেই পয়েন্টটি রেকর্ড করুন এবং বিক্রয় সীমিত লাইন শুরু করুন।

- বিক্রয় সীমিত লাইন ইনপুট প্যারামিটার অনুযায়ী একটি নির্দিষ্ট সময়কালের জন্য সক্রিয় থাকে, মেয়াদ শেষ হলে বন্ধ হয়ে যায়।

- যখন মূল্য আরও বৃদ্ধি পেয়ে বিক্রয় সীমিত লাইনের উপরে উঠে যায়, তখন সমস্ত লং পজিশন বন্ধ করা হয়।

ঝুঁকি নিয়ন্ত্রণ

কৌশলটিতে অন্তর্নির্মিত স্টপ-লস এবং টেক-প্রফিট ফিচার রয়েছে, যা কাস্টমাইজযোগ্য প্যারামিটার ব্যবহার করে খোলা অবস্থানের ঝুঁকি নিয়ন্ত্রণ করে।

পিরামিডিং পদ্ধতি

প্রতিটি ট্রেডিং পজিশন খোলার সময়, ইনপুট প্যারামিটার অনুযায়ী একটি নির্দিষ্ট অনুপাতে পরবর্তী ক্রয় মূল্য নির্ধারণ করা হয়, যা ধাপে ধাপে ক্রয় এবং পিরামিডিংয়ের প্রভাব তৈরি করে।

সুবিধা বিশ্লেষণ

- মূল্য পরিবর্তনের হার সূচক (ROC) ব্যবহার করে ক্রয়-বিক্রয় পয়েন্ট খুঁজে পাওয়া যায়; ROC মূল্য পরিবর্তনের প্রতি অত্যন্ত সংবেদনশীল, ফলে পয়েন্ট নির্ধারণে নির্ভুলতা আসে।

- সীমিত লাইন পদ্ধতি ব্যবহার করে ক্রয়-বিক্রয়ের সময় আরও নিশ্চিত করা হয়, মিথ্যা ব্রেকআউট এড়ানো যায়।

- পিরামিডিং পদ্ধতি ঝুঁকি নিয়ন্ত্রণের পাশাপাশি বাজারের মূল্য অনুসরণ করতে সাহায্য করে।

- অন্তর্নির্মিত স্টপ-লস এবং টেক-প্রফিট প্রতিটি অবস্থানের ঝুঁকি কঠোরভাবে নিয়ন্ত্রণ করে।

ঝুঁকি এবং সমাধান

- বাজারে তীব্র ওঠানামা দেখা দিলে কৌশলটি অতিরিক্ত পজিশন খুলতে পারে। সমাধান: পিরামিডিং প্যারামিটার সঠিকভাবে সেট করে মোট পজিশনের সংখ্যা নিয়ন্ত্রণ করা।

- যখন মূল্য দিকনির্দেশনাহীনভাবে ওঠানামা করে, তখন স্টপ-লস বা টেক-প্রফিট ঘন ঘন ট্রিগার হতে পারে। স্টপ-লস ও টেক-প্রফিটের ব্যবধান বাড়িয়ে দেওয়া বা ফিচারটি বন্ধ করে দেওয়া যেতে পারে।

অপটিমাইজেশন পরামর্শ

- অন্যান্য সূচকের সাথে সমন্বয় করে এন্ট্রি টাইম ফিল্টার করা। যেমন, মুভিং এভারেজের সাথে মিলিয়ে, কেবল মূল্য মুভিং এভারেজের নিচে নামলে ROC সূচক গ্রহণ করা।

- পিরামিডিং লজিক অপটিমাইজ করা, নির্দিষ্ট শর্ত পূরণ হলেই পিরামিডিং শুরু করা। যেমন, কেবলমাত্র মূল্য আরও নির্দিষ্ট পরিমাণে হ্রাস পেলে পিরামিডিং করা।

- বিভিন্ন প্রোডাক্টের জন্য প্যারামিটার সেটিংসে বড় পার্থক্য থাকতে পারে; সর্বোত্তম প্যারামিটার কম্বিনেশন পেতে পর্যাপ্ত ব্যাকটেস্টিং এবং সিমুলেটেড রিয়েল ট্রেডিং প্রয়োজন।

- অ্যাডাপটিভ স্টপ-লস এবং টেক-প্রফিট সেট করা যেতে পারে, বাজারের ওঠানামার মাত্রা অনুযায়ী ভিন্ন স্টপ-লস ব্যবধান নির্ধারণ করা।

সারসংক্ষেপ

এই কৌশলটি ROC সূচকের সঠিক অবস্থান নির্ণয়, সীমিত লাইন পদ্ধতি দ্বারা সিগন্যাল ফিল্টারিং, অন্তর্নির্মিত স্টপ-লস ও টেক-প্রফিট দ্বারা ঝুঁকি প্রতিরোধ এবং পিরামিডিং দ্বারা লাভ বৃদ্ধি করে। সঠিক প্যারামিটার সেটিংসের অধীনে, এটি ঝুঁকি নিয়ন্ত্রণের মধ্যে রেখে অতিরিক্ত লাভ অর্জন করতে পারে। ভবিষ্যতে সিগন্যাল ফিল্টারিং ও ঝুঁকি নিয়ন্ত্রণ প্রক্রিয়া আরও উন্নত করে কৌশলটিকে আরও বেশি বাজার পরিবেশের উপযোগী করা যেতে পারে।

- 1