দ্বৈত প্রবণতা অনুসরণ কৌশল

সারসংক্ষেপ

দ্বৈত প্রবণতা ট্র্যাকিং কৌশল একটি পরিমাণগত ট্রেডিং কৌশল যা একই সাথে দ্বৈত সূচক ব্যবহার করে প্রবণতা নির্ধারণ করে। এই কৌশলটি প্রথমে ১২৩ রিভার্সাল ইনডিকেটর ব্যবহার করে মূল্যের রিভার্সাল সিগন্যাল নির্ণয় করে এবং তারপর দিকনির্দেশক প্রবণতা সূচক (DTI) এর সাথে মিলিয়ে মূল্য প্রবণতার দিক নির্ধারণ করে, ফলে অর্ডার দেওয়ার সিগন্যালের দ্বৈত নিশ্চিতকরণ পাওয়া যায়।

কৌশলের মূলনীতি

এই কৌশলটি মূলত দুটি অংশ নিয়ে গঠিত:

-

১২৩ রিভার্সাল ইনডিকেটর

১২৩ রিভার্সাল ইনডিকেটরের নির্ণয় নীতি হল:

-

যখন ক্লোজিং প্রাইস টানা ২ দিন বেড়ে যায় এবং ৯ দিনের স্লো কে লাইন ৫০ এর নিচে থাকে, তখন লং পজিশন নিতে হবে;

-

যখন ক্লোজিং প্রাইস টানা ২ দিন কমে যায় এবং ৯ দিনের ফাস্ট কে লাইন ৫০ এর উপরে থাকে, তখন শর্ট পজিশন নিতে হবে।

এভাবে মূল্য রিভার্সালের সময় পয়েন্ট ক্যাপচার করা যায়।

-

-

দিকনির্দেশক প্রবণতা সূচক (DTI)

DTI সূচকের নির্ণয় নীতি: একটি নির্দিষ্ট সময়ের মধ্যে মূল্য ওঠানামার পরম মানের মুভিং এভারেজ বের করে, তারপর তা মূল্যের গড় বিস্তার দিয়ে ভাগ করা হয়।

-

যখন DTI ওভারবট লাইনের উপরে থাকে, তখন বোঝায় বর্তমানে নিম্নমুখী প্রবণতা চলছে;

-

যখন DTI ওভারসোল্ড লাইনের নিচে থাকে, তখন বোঝায় বর্তমানে ঊর্ধ্বমুখী প্রবণতা চলছে।

-

-

উভয়ের সমন্বয়

প্রথমে ১২৩ রিভার্সাল ইনডিকেটর ব্যবহার করে নির্ণয় করা হয় মূল্যে রিভার্সাল সিগন্যাল এসেছে কিনা। তারপর DTI সূচকের সাথে যুক্ত করে রিভার্সালের পর মূল্যের সামগ্রিক প্রবণতার দিক নির্ধারণ করা হয়।

এভাবে শুধুমাত্র রিভার্সাল সিগন্যালের উপর নির্ভর করে ভুয়া রিভার্সালের সমস্যা এড়ানো যায়, ফলে কৌশলের স্থিতিশীলতা এবং লাভজনকতা বৃদ্ধি পায়।

কৌশলের সুবিধা

-

দ্বৈত সূচক নিশ্চিতকরণ, ভুয়া রিভার্সালের ঝুঁকি এড়ানো যায়

-

রিভার্সাল ও প্রবণতা নির্ণয়ের সমন্বয়, অপারেশনাল নমনীয়তা ও স্থিতিশীলতা উভয়ই বজায় থাকে

-

প্যারামিটার অপ্টিমাইজেশনের সুযোগ অনেক বেশি, বিভিন্ন সম্পদের সাথে মানানসই করে নমনীয়ভাবে সামঞ্জস্য করা যায়

ঝুঁকি বিশ্লেষণ

-

DTI প্যারামিটার সেটিংয়ে অভিজ্ঞতা প্রয়োজন, ভুল হলে প্রবণতার দিক ভুলভাবে নির্ধারিত হতে পারে

-

রিভার্সাল সবসময় নতুন প্রবণতার সূচনা নয়, রেঞ্জ মার্কেটে দোদুল্যমান অবস্থা দেখা দিতে পারে

-

কার্যকর স্টপ-লস প্রয়োজন, একক ট্রেডের ক্ষতি নিয়ন্ত্রণ করতে হবে

সমাধান: প্যারামিটার অপ্টিমাইজেশন পরীক্ষা + যুক্তিসঙ্গত স্টপ-লস + অন্যান্য সূচকের সাথে একত্রীকরণ

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

DTI প্যারামিটার পরীক্ষা করে সর্বোত্তম প্যারামিটার কম্বিনেশন খুঁজে বের করা

-

অন্যান্য সূচকের সাথে একত্রিত করে ভুয়া রিভার্সাল সিগন্যাল ফিল্টার করা

-

স্টপ-লস কৌশল অপ্টিমাইজ করে সর্বোত্তম স্টপ-লস পয়েন্ট নির্ণয় করা

উপসংহার

দ্বৈত প্রবণতা ট্র্যাকিং কৌশল ১২৩ রিভার্সাল ও DTI এর দ্বৈত সূচক নিশ্চিতকরণের মাধ্যমে কার্যকরভাবে মূল্যের প্রকৃত রিভার্সাল নির্ণয় করতে পারে এবং নতুন প্রবণতার দিক ক্যাপচার করতে পারে, ফলে কৌশলের লাভের সম্ভাবনা বৃদ্ধি পায়। তবে প্যারামিটার সেটিং ও স্টপ-লস কৌশল এখনও ক্রমাগত পরীক্ষা ও অপ্টিমাইজেশন প্রয়োজন, যাতে কৌশলের লাভের সম্ভাবনা সর্বাধিক করা যায়। সামগ্রিকভাবে, এই কৌশলটি প্রবণতা ও রিভার্সাল ট্রেডিং উভয়ের সুবিধাকে একত্রিত করে, এটি একটি সুপারিশযোগ্য পরিমাণগত কৌশল।

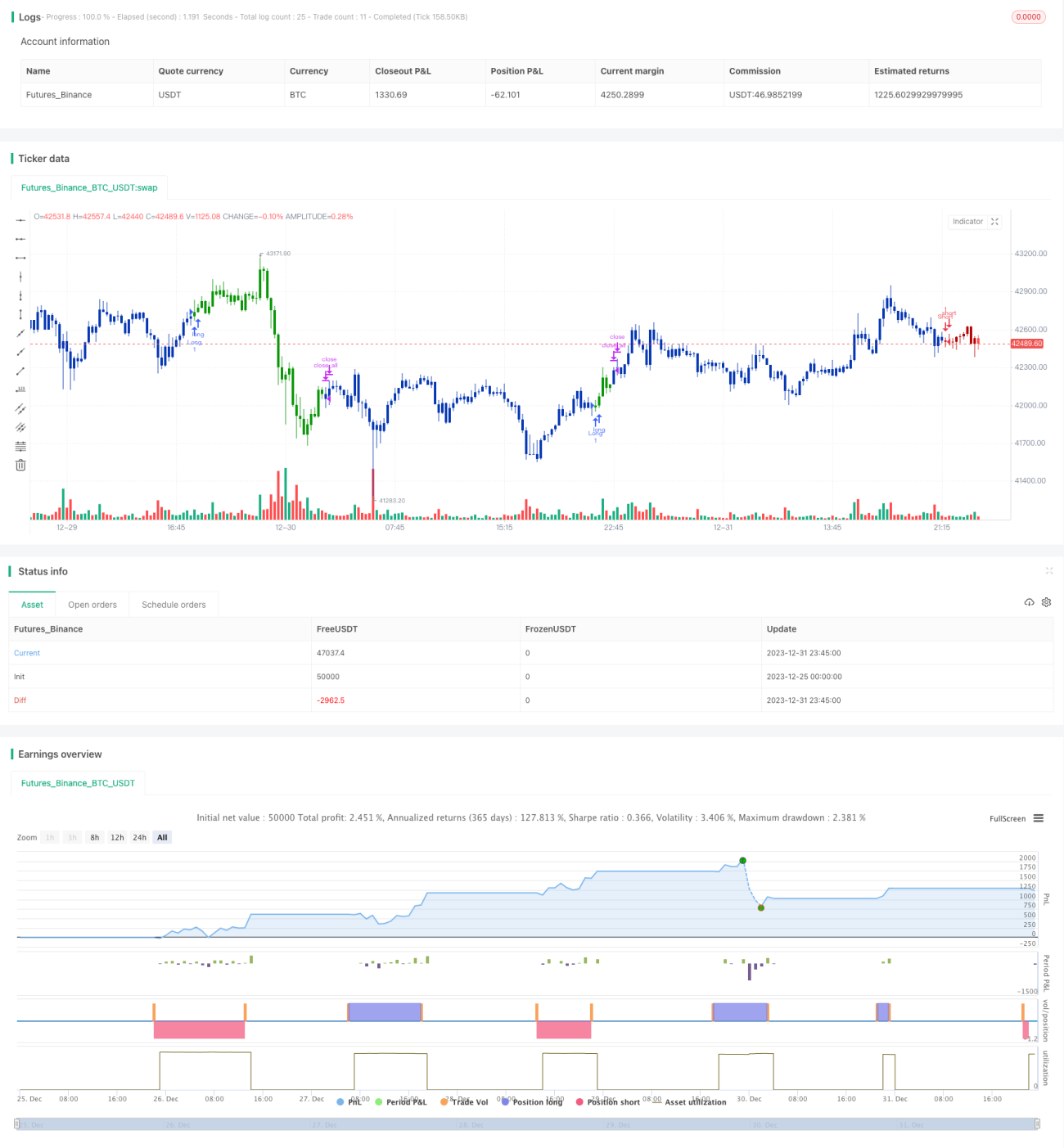

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-01 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 19/02/2020

// This is combo strategies for get a cumulative signal. - 1