সময় ও স্থান অতিক্রমকারী মফেই সূচক কৌশল

সারসংক্ষেপ

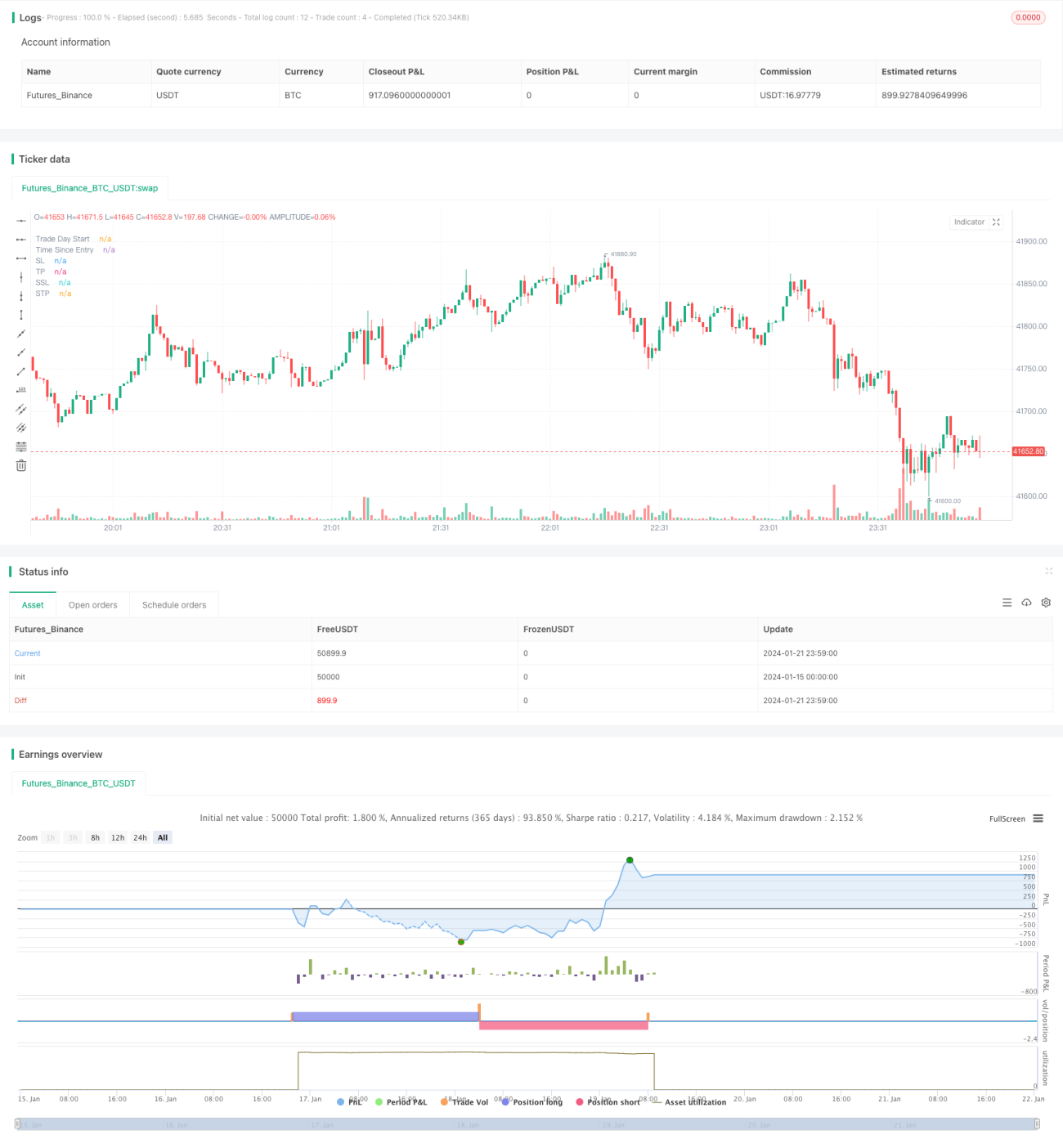

এটি একটি সরল পরিমাণগত কৌশল যা মোফি সূচক ব্যবহার করে বাজারে "বড় হাঙর" চিহ্নিত করে। এটি 5 মিনিটের টাইমফ্রেমে প্রযোজ্য এবং প্রধানত ক্রিপ্টোকারেন্সি ট্রেডিংয়ের জন্য ব্যবহৃত হয়।

কৌশলের মূলনীতি

এই কৌশলটি দৈর্ঘ্য ৩-এর মোফি সূচক ব্যবহার করে, ওভারবট লাইন ১০০ এবং ওভারসেল্ড লাইন ০ এ নির্ধারণ করে। কৌশলটি মোফি সূচকের ওভারবট স্তরে পৌঁছানোর জন্য অপেক্ষা করে, যা বাজারে "বড় হাঙরের" উপস্থিতি নির্দেশ করে। যদি সেই দিনের প্রথম দুটি মোফি সূচকের ওভারবট পয়েন্টের পরেও দাম ঊর্ধ্বমুখী থাকে, তাহলে এটি একটি লং এন্ট্রি সংকেত।

যখন মোফি সূচক = ১০০ এবং পরবর্তী ক্যান্ডেলটি একটি বড় সবুজ ক্যান্ডেল হয়, তখন লং পজিশনে প্রবেশ করুন। স্টপ লস সেই ট্রেডিং দিনের সর্বনিম্ন পয়েন্টে সেট করা হয়, এবং টেক প্রফিট এন্ট্রির ৬০ মিনিটের মধ্যে নেওয়া হয়।

শর্ট ট্রেডের জন্য, বিপরীত লজিক ব্যবহার করা যেতে পারে। অর্থাৎ, মোফি সূচক ওভারসেল্ড হওয়ার পর যদি পরবর্তী ক্যান্ডেলটি একটি বড় লাল ক্যান্ডেল হয়, তাহলে শর্ট পজিশনে প্রবেশ করুন।

কৌশলের সুবিধা

-

মোফি সূচক ব্যবহার করে বাজারে "বড় হাঙরের" সম্ভাব্য স্টক জমা করার আচরণ কার্যকরভাবে শনাক্ত করা যায়, যেগুলোর আরও ঊর্ধ্বমুখী হওয়ার সম্ভাবনা থাকে।

-

ক্যান্ডেলের বডি ব্যবহার করে শক্তিশালী ব্রেকআউট পয়েন্ট চিহ্নিত করায় অনেক মিথ্যা ব্রেকআউট ফিল্টার করা যায়।

-

এসএমএ ফিল্টার যুক্ত করার কারণে পড়ন্ত ট্রেন্ডের স্টক কেনা এড়ানো যায়, যা ট্রেডিং ঝুঁকি হ্রাস করে।

-

ইন্ট্রাডে অল্প সময়ের ট্রেডিং পদ্ধতি ব্যবহার করে ৬০ মিনিটের টেক প্রফিট দ্রুত লাভ লক করতে সাহায্য করে এবং ড্রডাউনের সম্ভাবনা কমায়।

কৌশলের ঝুঁকি

-

মোফি সূচক মিথ্যা সংকেত তৈরি করতে পারে, ফলে অপ্রয়োজনীয় ক্ষতি হতে পারে। প্যারামিটার যথাযথভাবে সামঞ্জস্য করে বা অন্য সূচক যুক্ত করে ফিল্টার করা যেতে পারে।

-

৬০ মিনিটের অতি-স্বল্পমেয়াদী পদ্ধতি খুবই আক্রমণাত্মক হতে পারে এবং উচ্চ অস্থিরতার স্টকের জন্য উপযুক্ত নয়। টেক প্রফিট সময় পরিবর্তন করে অথবা ট্রেইলিং স্টপ লস ব্যবহার করে অপ্টিমাইজ করা যেতে পারে।

-

বড় আর্থ-সামাজিক ঘটনার সময় বাজারের প্রভাব বিবেচনা করা হয়নি। এসব ক্ষেত্রে কৌশল বন্ধ রেখে বাজার স্থিতিশীল হওয়ার পর আবার ট্রেডিং শুরু করা উচিত।

কৌশলের অপ্টিমাইজেশনের দিকনির্দেশনা

-

বিভিন্ন প্যারামিটার কম্বিনেশন পরীক্ষা করা যায়, যেমন মোফি সূচকের দৈর্ঘ্য পরিবর্তন, এসএমএ পিরিয়ড অপ্টিমাইজ করা ইত্যাদি।

-

অন্যান্য সূচক যেমন বোলিঞ্জার ব্যান্ড, কেডি সূচক ইত্যাদি যুক্ত করে সিগন্যালের নির্ভুলতা বাড়ানো যায় কিনা তা পরীক্ষা করা।

-

স্টপ লসের পরিধি কিছুটা বাড়িয়ে দেওয়ার ফলে একক লেনদেনে বেশি মুনাফা পাওয়া যায় কিনা তা পরীক্ষা করা।

-

এই কৌশলের ভিত্তিতে অন্যান্য টাইমফ্রেমের জন্য (যেমন ১৫ মিনিট বা ৩০ মিনিট) সংস্করণ তৈরি করে পরীক্ষা করা।

সারসংক্ষেপ

সামগ্রিকভাবে কৌশলটি অত্যন্ত সরল এবং বোঝা সহজ, এর মূল ধারণা ক্লাসিক "বড় হাঙর" অনুসরণের পদ্ধতির সাথে মেলে। মোফি সূচকের ওভারবট/ওভারসেল্ড মূল পয়েন্ট চিহ্নিত করে এবং ক্যান্ডেলের বডি দিয়ে ফিল্টার করে অনেক নয়েজ কমানো যায়। এসএমএ ফিল্টার যুক্ত করায় কৌশলের স্থিতিশীলতা আরও বেড়েছে।

৬০ মিনিটের অতি-স্বল্পমেয়াদী পদ্ধতি দ্রুত লাভ করতে সাহায্য করে, তবে উচ্চ ট্রেডিং ঝুঁকি নিয়ে আসে। সামগ্রিকভাবে এটি একটি অত্যন্ত ব্যবহারিক মূল্যের পরিমাণগত কৌশল টেমপ্লেট, যা গভীরভাবে গবেষণা ও অপ্টিমাইজেশনের যোগ্য, এবং আমাদের মূল্যবান কৌশল উন্নয়নের ধারণা প্রদান করে।

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1