দ্বৈত চলমান গড় চান থিওরি কৌশল

সারসংক্ষেপ

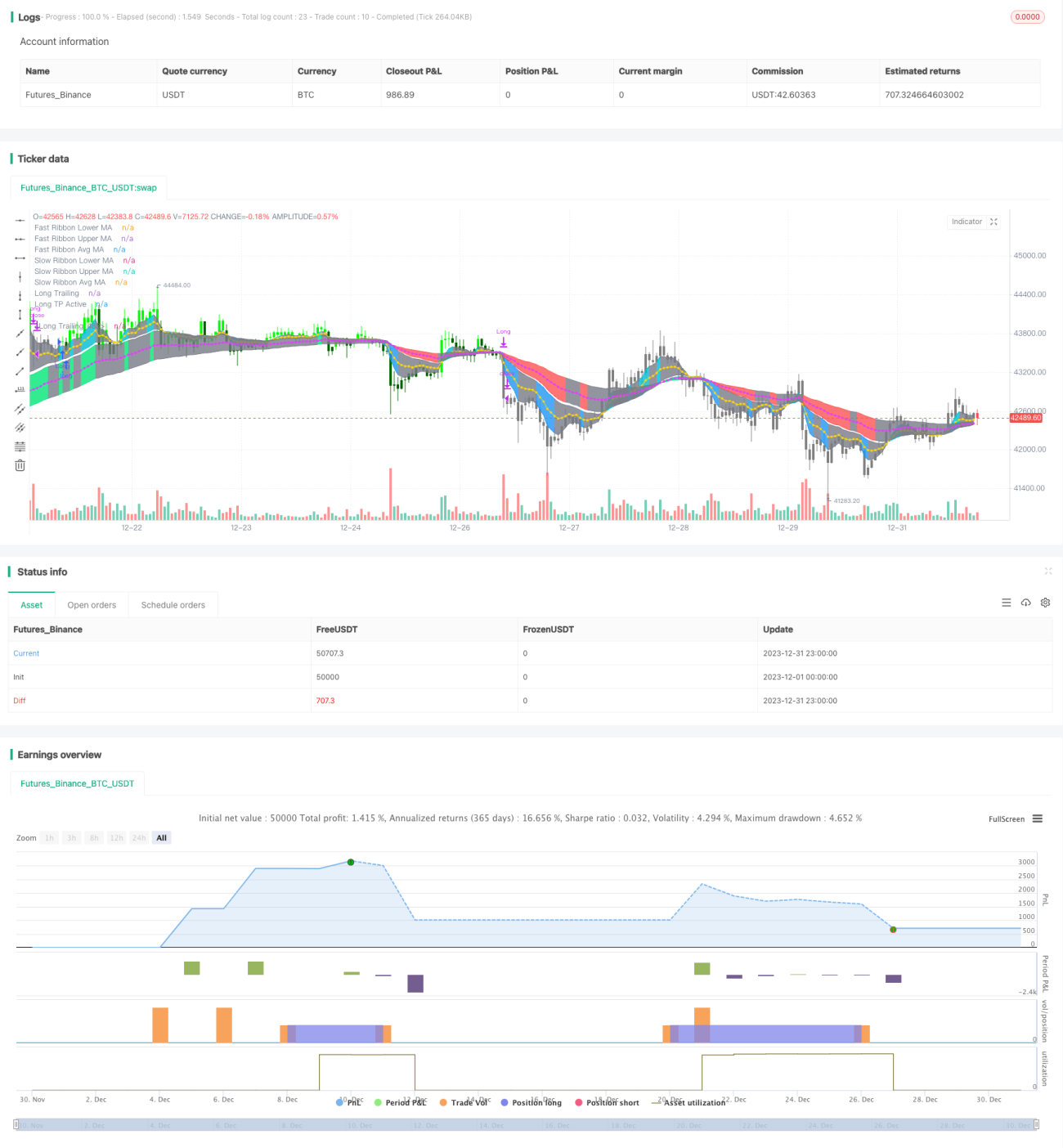

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলটি একটি ট্রেন্ড অনুসরণকারী কৌশল। এটি দুটি সেট মুভিং এভারেজ গণনা করে দ্রুত লাইন গ্রুপ এবং ধীর লাইন গ্রুপ তৈরি করে এবং দামের সাথে মুভিং এভারেজের সম্পর্কের মাধ্যমে ট্রেন্ডের দিক নির্ণয় করে।

যখন দ্রুত লাইন ধীর লাইনের উপরে উঠে যায়, এটি বুলিশ সংকেত। যখন দ্রুত লাইন ধীর লাইনের নিচে নেমে যায়, এটি বেয়ারিশ সংকেত। এই কৌশলটি দ্রুত ও ধীর মুভিং এভারেজের দিক, দাম ব্রেকআউটের ক্যান্ডেল সংখ্যা ইত্যাদি শর্তের ভিত্তিতে নির্দিষ্ট এন্ট্রি এবং এক্সিটের সময় নির্ধারণ করে।

কৌশলের নীতি

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলটি দুটি সেট মুভিং এভারেজ গণনা করে, যা স্বল্পমেয়াদী এবং দীর্ঘমেয়াদী ট্রেন্ড নির্ধারণের মানদণ্ড উপস্থাপন করে। বিশেষ করে, কৌশলে নিম্নলিখিতগুলি সংজ্ঞায়িত করা হয়েছে:

- দ্রুত মুভিং এভারেজ গ্রুপ, যাতে দ্রুত নিম্ন রেখা এবং দ্রুত ঊর্ধ্ব রেখা রয়েছে, যা স্বল্পমেয়াদী ট্রেন্ডকে প্রতিনিধিত্ব করে;

- ধীর মুভিং এভারেজ গ্রুপ, যাতে ধীর নিম্ন রেখা এবং ধীর ঊর্ধ্ব রেখা রয়েছে, যা দীর্ঘমেয়াদী ট্রেন্ডকে প্রতিনিধিত্ব করে।

কৌশলটি দ্রুত মুভিং এভারেজ গ্রুপ এবং ধীর মুভিং এভারেজ গ্রুপের মধ্যে মূল্যের সম্পর্ক ব্যবহার করে স্বল্পমেয়াদী ও দীর্ঘমেয়াদী ট্রেন্ডের যৌক্তিকতা এবং নির্দিষ্ট এন্ট্রি ও এক্সিটের সময় নির্ধারণ করে।

এন্ট্রি শর্ত নিম্নরূপ:

- দ্রুত ঊর্ধ্ব রেখা যখন ধীর ঊর্ধ্ব রেখাকে উপরের দিকে ভেঙে ২টি বা তার বেশি ক্যান্ডেল ধরে রাখে, তখন লং এন্ট্রি হয়।

- দ্রুত নিম্ন রেখা যখন ধীর নিম্ন রেখাকে নিচের দিকে ভেঙে ২টি বা তার বেশি ক্যান্ডেল ধরে রাখে, তখন শর্ট এন্ট্রি হয়।

এক্সিট শর্ত নিম্নরূপ:

- লং পজিশন ধারণকালে, দ্রুত মুভিং এভারেজ যখন ধীর মুভিং এভারেজকে নিচের দিকে ক্রস করে, তখন লং এক্সিট হয়।

- শর্ট পজিশন ধারণকালে, দ্রুত মুভিং এভারেজ যখন ধীর মুভিং এভারেজকে উপরের দিকে ক্রস করে, তখন শর্ট এক্সিট হয়।

এছাড়াও, কৌশলে টেক প্রফিট, স্টপ লস এবং ট্রেইলিং স্টপ লসের মতো ফিচার রয়েছে ঝুঁকি নিয়ন্ত্রণের জন্য।

সুবিধা বিশ্লেষণ

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলের প্রধান সুবিধাগুলি হল:

- ডাবল মুভিং এভারেজ ব্যবহার করে বাজারের নয়েজ কার্যকরভাবে ফিল্টার করে ট্রেন্ডের দিক নির্ধারণ করা যায়।

- দ্রুত ও ধীর মুভিং এভারেজ এবং মূল্যের সম্পর্কের মাধ্যমে সংকেতের নির্ভরযোগ্যতা বেশি।

- কৌশলের নিয়ম সহজ ও স্পষ্ট, সহজে বোঝা ও বাস্তবায়নযোগ্য, কোয়ান্টিটেটিভ ট্রেডিংয়ের জন্য উপযুক্ত।

- টেক প্রফিট, স্টপ লস, ট্রেইলিং স্টপ লসের মতো ঝুঁকি নিয়ন্ত্রণের ব্যবস্থা রয়েছে, যা ট্রেডিং ঝুঁকি কার্যকরভাবে নিয়ন্ত্রণ করতে পারে।

ঝুঁকি বিশ্লেষণ

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলের কিছু ঝুঁকি রয়েছে, প্রধানত:

- রেঞ্জবাউন্ড (সাইডওয়ে) বাজারে মিথ্যা সংকেত তৈরি হতে পারে, ফলে অপ্রয়োজনীয় ট্রেড হতে পারে।

- মুভিং এভারেজ সিস্টেম আকস্মিক ঘটনা (যেমন গুরুত্বপূর্ণ নেতিবাচক/ইতিবাচক সংবাদ প্রকাশ) প্রতি বিলম্বে প্রতিক্রিয়া দেখাতে পারে, ফলে বড় ক্ষতি হতে পারে।

- ট্রেইলিং স্টপ লস নির্দিষ্ট বাজার পরিস্থিতিতে ভেঙে পড়তে পারে, ফলে ক্ষতি বাড়তে পারে।

উপরোক্ত ঝুঁকি নিয়ন্ত্রণের জন্য, মুভিং এভারেজ প্যারামিটার অপ্টিমাইজ করা বা অন্যান্য ইন্ডিকেটর দিয়ে ফিল্টার করার মতো উন্নতি করা যেতে পারে।

অপ্টিমাইজেশন দিকনির্দেশনা

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলটি নিম্নলিখিত মাত্রা থেকে অপ্টিমাইজ করা যেতে পারে:

- মুভিং এভারেজ প্যারামিটার অপ্টিমাইজ করা, মুভিং এভারেজ সময়কাল সামঞ্জস্য করে বিভিন্ন সময় ফ্রেমের বাজারের সাথে খাপ খাওয়ানো।

- অন্যান্য ইন্ডিকেটর ফিল্টার যুক্ত করে একটি মাল্টি-ইন্ডিকেটর কম্বিনেশন কৌশল তৈরি করা, সংকেতের নির্ভুলতা বৃদ্ধি করা।

- স্টপ লস ও টেক প্রফিট সেটিং অপ্টিমাইজ করা, ড্রডাউন থ্রেশহোল্ড সেট করে সর্বোচ্চ ক্ষতি নিয়ন্ত্রণ করা।

- মেশিন লার্নিং মডেল ব্যবহার করে ট্রেন্ড পূর্বাভাস দেওয়া, এন্ট্রি টাইমিং নির্ধারণে সহায়তা করা।

সারসংক্ষেপ

ডাবল মুভিং এভারেজ চ্যান তত্ত্ব কৌশলটি সামগ্রিকভাবে একটি খুবই ব্যবহারিক ট্রেন্ড অনুসরণকারী কৌশল। এর বিচার নিয়ম সহজ, যুক্তি স্পষ্ট, ডাবল মুভিং এভারেজ সিস্টেমের মাধ্যমে ঝুঁকি নিয়ন্ত্রণ করে এবং তাত্ত্বিক ভিত্তি শক্তিশালী। পরবর্তী পদক্ষেপে প্যারামিটার অপ্টিমাইজেশন, ঝুঁকি নিয়ন্ত্রণ ইত্যাদি বিভিন্ন দিক থেকে উন্নতি করে কৌশলটির লাভজনকতা ও স্থিতিশীলতা আরও বাড়ানো যেতে পারে।

- 1