দ্বৈত MA মোমেন্টাম ব্রেকআউট কৌশল

সারসংক্ষেপ

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজি একটি কোয়ান্টিটেটিভ ট্রেডিং স্ট্র্যাটেজি যা ডুয়াল মুভিং এভারেজ এবং আরএসআই ইনডিকেটরকে একত্রিত করে। এই স্ট্র্যাটেজিটি দ্রুত মুভিং এভারেজ, ধীর মুভিং এভারেজ এবং আরএসআই ইনডিকেটর গণনা করে, আরএসআই-এর ওভারবট ও ওভারসোল্ড থ্রেশহোল্ড নির্ধারণ করে এবং ডুয়াল এমএ-তে গোল্ডেন ক্রস হলে লং পজিশন নেয়, আর ডেথ ক্রস হলে শর্ট পজিশন নেয়, যাতে বাজারের ট্রেন্ড অনুযায়ী লাভ করা যায়।

স্ট্র্যাটেজির মূলনীতি

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজি মূলত ডুয়াল মুভিং এভারেজ এবং আরএসআই ইনডিকেটরের উপর ভিত্তি করে তৈরি। প্রথমে একটি দ্রুত এবং একটি ধীর—দুটি মুভিং এভারেজ গণনা করা হয়; দ্রুত লাইনটি ১০-দিনের ওয়েটেড মুভিং এভারেজ এবং ধীর লাইনটি ১০০-দিনের লিনিয়ার অ্যাডাপ্টিভ মুভিং এভারেজ। তারপর ১৪-দিনের আরএসআই ইনডিকেটর গণনা করে ওভারবট ও ওভারসোল্ড থ্রেশহোল্ড নির্ধারণ করা হয়। যখন দ্রুত লাইন ধীর লাইনকে উপরে ছেদ করে, তখন তা বুলিশ মার্কেট হিসাবে চিহ্নিত হয়, আর যখন দ্রুত লাইন ধীর লাইনের নিচে চলে যায়, তখন তা বিয়ারিশ মার্কেট হিসাবে চিহ্নিত হয়। বুলিশ বা বিয়ারিশ মার্কেট নির্ধারণের পাশাপাশি, আরএসআই ইনডিকেটরকে ওভারবট লাইনের উপরে বা ওভারসোল্ড লাইনের নিচে থাকতে হয়, যাতে মিথ্যা ব্রেকআউট কার্যকরভাবে ফিল্টার করা যায়।

নির্দিষ্টভাবে বলতে গেলে, যখন বুলিশ মার্কেট নির্ধারিত হয় এবং সেই সময় আরএসআই ইনডিকেটর ওভারবট লাইনের উপরে থাকে, তখন লং পজিশন খোলা হয়; যখন বিয়ারিশ মার্কেট নির্ধারিত হয় এবং আরএসআই ইনডিকেটর ওভারসোল্ড লাইনের নিচে থাকে, তখন শর্ট পজিশন খোলা হয়। পজিশন খোলার পর, ট্রেডিং সিগন্যাল উল্টে গেলে বিপরীত পজিশন খোলা হয়।

স্ট্র্যাটেজির সুবিধা

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজি ডুয়াল এমএ এবং আরএসআই ইনডিকেটরকে একত্রিত করে বাজারের ট্রেন্ড কার্যকরভাবে শনাক্ত করতে পারে এবং আরএসআই ইনডিকেটর ব্যবহার করে মিথ্যা ব্রেকআউট ফিল্টার করতে পারে, ফলে ট্রেডিং সিগন্যালের নির্ভরযোগ্যতা বৃদ্ধি পায়। একক এমএ সিস্টেমের তুলনায়, এই স্ট্র্যাটেজিটি অকার্যকর ট্রেডের সংখ্যা উল্লেখযোগ্যভাবে কমাতে পারে। উপরন্তু, আরএসআই ইনডিকেটরের প্যারামিটার অপ্টিমাইজেশনও স্ট্র্যাটেজিটিকে নমনীয়তা দেয়।

স্ট্র্যাটেজির ঝুঁকি

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজির কিছু ঝুঁকিও রয়েছে। ডুয়াল এমএ সিস্টেম প্যারামিটারের প্রতি অত্যন্ত সংবেদনশীল, তাই বিভিন্ন বাজারে প্যারামিটার কম্বিনেশন সাবধানে পরীক্ষা করা প্রয়োজন। উপরন্তু, আরএসআই ইনডিকেটরের থ্রেশহোল্ড ঠিকমতো নির্ধারণ না করলে ট্রেডিং সুযোগ হাতছাড়া হতে পারে। শেষ পর্যন্ত, আক্রমনাত্মক ট্রেইলিং স্টপ নির্দিষ্ট বাজারের পরিস্থিতিতে ভেঙে যেতে পারে, তাই ব্যাকটেস্ট ফলাফলের ভিত্তিতে স্টপ-লস পয়েন্ট সামঞ্জস্য করা উচিত।

স্ট্র্যাটেজির অপ্টিমাইজেশন

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

- দ্রুত ও ধীর এমএ-র প্যারামিটার অপ্টিমাইজ করে সেরা প্যারামিটার কম্বিনেশন খোঁজা;

- আরএসআই প্যারামিটার অপ্টিমাইজ করে ওভারবট ও ওভারসোল্ড থ্রেশহোল্ড সামঞ্জস্য করা;

- অ্যাডাপ্টিভ ট্রেইলিং স্টপ মেকানিজম যুক্ত করে ঝুঁকি নিয়ন্ত্রণ করা;

- পজিশন সাইজ অপ্টিমাইজেশন মডিউল যুক্ত করে মূলধন ব্যবহারের দক্ষতা বাড়ানো।

উপসংহার

ডুয়াল এমএ মোমেন্টাম ব্রেকআউট স্ট্র্যাটেজি ডুয়াল এমএ সিস্টেমের মাধ্যমে ট্রেন্ডের দিক নির্ধারণ করে এবং আরএসআই ইনডিকেটর দিয়ে সিগন্যাল ফিল্টার করে, যা একক এমএ সিস্টেমের ত্রুটিগুলি কার্যকরভাবে দূর করে। এই স্ট্র্যাটেজিতে প্যারামিটার অপ্টিমাইজেশনের যথেষ্ট সুযোগ রয়েছে এবং এটি অ্যাডাপ্টিভ অ্যাডজাস্টমেন্ট করতে পারে, তাই এটি একটি চমৎকার ট্রেন্ড ফলোয়িং স্ট্র্যাটেজি।

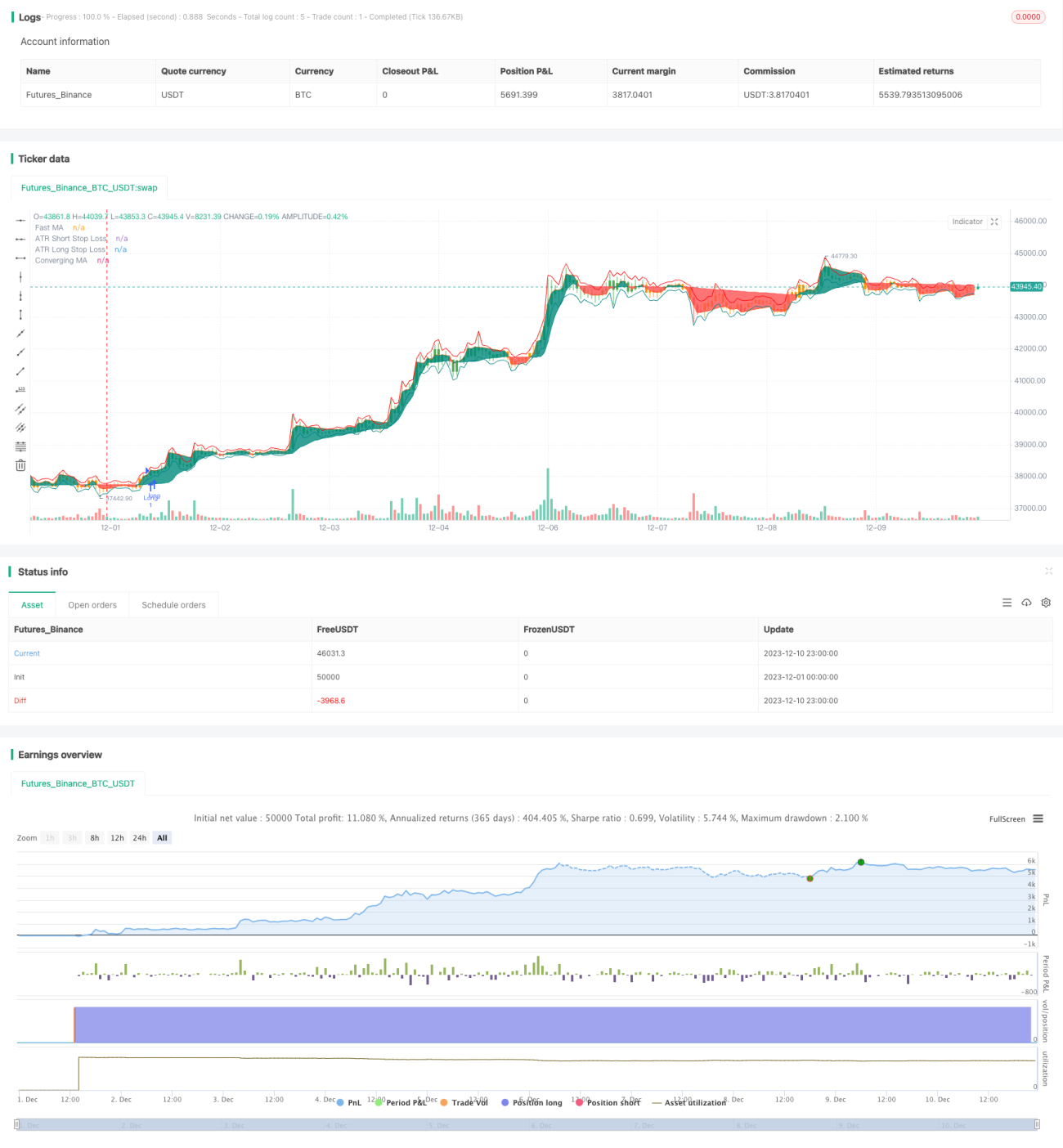

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-10 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © Salman4sgd

//@version=5- 1