## হাল সূচক এবং এলএসএমএ সূচকের উপর ভিত্তি করে ট্রেন্ড ফলোয়িং কোয়ান্টিটেটিভ স্ট্র্যাটেজি

সারসংক্ষেপ

এই কৌশলটি হুল নির্দেশক এবং এলএসএমএ (Least Squares Moving Average) নির্দেশককে একত্রিত করে ট্রেন্ডের দিক এবং ট্রেন্ড রিভার্সাল পয়েন্ট চিহ্নিত করে, যার মাধ্যমে ট্রেন্ড অনুসরণ করা হয়। যখন হুল নির্দেশক ঊর্ধ্বমুখী ট্রেন্ড দেখায় এবং এলএসএমএ হুল নির্দেশকের উপরে উঠে যায়, তখন লং পজিশন নেওয়া হয়; যখন হুল নির্দেশক নিম্নমুখী ট্রেন্ড দেখায় এবং এলএসএমএ হুল নির্দেশকের নিচে নেমে যায়, তখন শর্ট পজিশন নেওয়া হয়। এই কৌশলটি মাঝারি-নিম্ন ফ্রিকোয়েন্সি ট্রেডিংয়ের জন্য উপযোগী এবং ১ মিনিটের টাইমফ্রেমে ব্যবহার করা যেতে পারে।

কৌশলের নীতি

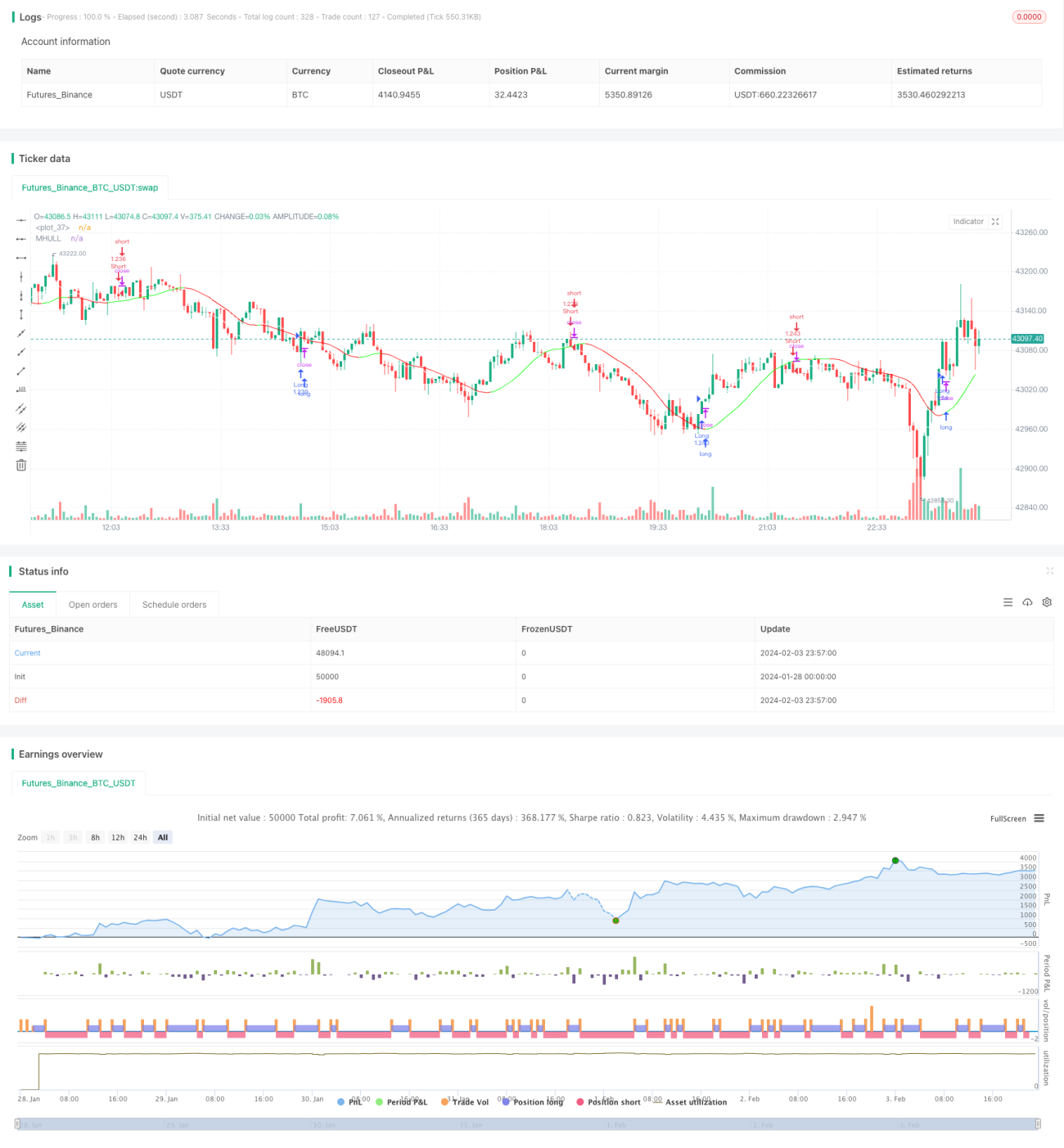

- হুল নির্দেশক মানের ট্রেন্ডের দিক নির্ধারণে ব্যবহৃত হয়। যখন মিডল লাইন (MHULL) লোয়ার লাইন (LHULL) এর উপরে থাকে, তখন তা ঊর্ধ্বমুখী ট্রেন্ড নির্দেশ করে; বিপরীত হলে নিম্নমুখী ট্রেন্ড নির্দেশ করে।

- এলএসএমএ নির্দেশক ট্রেন্ড রিভার্সাল পয়েন্ট চিহ্নিত করতে ব্যবহৃত হয়। যখন এলএসএমএ নির্দেশক MHULL এর উপরে উঠে যায়, তখন তা ঊর্ধ্বমুখী ট্রেন্ডের সৃষ্টি বা ত্বরণ নির্দেশ করে; যখন এলএসএমএ নির্দেশক MHULL এর নিচে নেমে যায়, তখন তা নিম্নমুখী ট্রেন্ডের সৃষ্টি বা ত্বরণ নির্দেশ করে।

- উভয়কে একত্রিত করে, যখন হুল নির্দেশক ঊর্ধ্বমুখী ট্রেন্ড দেখায় (MHULL > LHULL) এবং এলএসএমএ MHULL এর উপরে উঠে যায়, তখন লং করা হয়; যখন হুল নির্দেশক নিম্নমুখী ট্রেন্ড দেখায় (MHULL < LHULL) এবং এলএসএমএ MHULL এর নিচে নেমে যায়, তখন শর্ট করা হয়।

- স্টপ লস নিকটতম সুইং পয়েন্টে নির্ধারণ করা হয়। লং পজিশনের স্টপ লস নিকটতম সর্বনিম্ন পয়েন্টে এবং শর্ট পজিশনের স্টপ লস নিকটতম সর্বোচ্চ পয়েন্টে।

সুবিধা বিশ্লেষণ

১. হুল নির্দেশক দ্রুত প্রতিক্রিয়া দেখায় এবং সময়মতো ট্রেন্ড পরিবর্তন ধরতে পারে; এলএসএমএ-র মসৃণতা বেশি, রিভার্সাল সিগন্যাল শনাক্তকরণে নির্ভুল ও নির্ভরযোগ্য। উভয়ের সমন্বয় ভালো ফল দেয়।

২. এলএসএমএ-র ক্রসওভারের মাধ্যমে হুল নির্দেশকের মিথ্যা সংকেত ফিল্টার করা হয়, যা ভুল ট্রেডের সম্ভাবনা কমায়।

৩. সুইং পয়েন্টকে স্টপ লস হিসেবে ব্যবহার করে মূলধনের সর্বোচ্চ সুরক্ষা নিশ্চিত করা হয়।

৪. মাঝারি-নিম্ন ফ্রিকোয়েন্সি ট্রেডিংয়ের জন্য উপযোগী, ১ মিনিট বা তার চেয়েও কম সময়ের ফ্রেমে ব্যবহার করা যেতে পারে, ফলে ব্যাপক প্রযোজ্যতা।

ঝুঁকি বিশ্লেষণ

১. ওঠানামা প্রবণ বাজারে হুল নির্দেশক এবং এলএসএমএ-র মধ্যে একাধিক ক্রসওভার হতে পারে, যার ফলে অতিরিক্ত ট্রেডিং হতে পারে। ট্রেডিং ফ্রিকোয়েন্সি কমানোর জন্য যথাযথভাবে প্যারামিটার সমন্বয় করা উচিত।

২. সুইং পয়েন্টে স্টপ লস নির্ধারণ করলে স্বল্পমেয়াদী মূল্য সমন্বয়ের কারণে তা ট্রিগার হতে পারে, তাই স্টপ লসের ব্যবধান যথাযথভাবে বাড়ানো উচিত।

৩. এলএসএমএ নির্দেশকের পশ্চাদগামী প্রকৃতির কারণে সামান্য ভুল সিদ্ধান্তের ঝুঁকি থাকতে পারে। এটি নিশ্চিত করতে ক্যান্ডেলস্টিক প্যাটার্নের মতো অন্যান্য নির্দেশকের সাথে সমন্বয় করা উচিত।

অপ্টিমাইজেশনের দিকনির্দেশনা

১. হুল নির্দেশক এবং এলএসএমএ-র প্যারামিটার অপ্টিমাইজ করা, যাতে তাদের সমন্বয় বিভিন্ন সম্পদ এবং টাইমফ্রেমের সাথে আরও ভালোভাবে মানিয়ে নেওয়া যায়।

২. অস্থিরতা, ট্রেডিং ভলিউম ইত্যাদির ভিত্তিতে ফিল্টারিং শর্ত যোগ করা, যাতে ওঠানামা প্রবণ বাজারে ভুল ট্রেড এড়ানো যায়।

৩. ট্রেন্ডের প্রবণতা নির্ধারণে মেশিন লার্নিং অ্যালগরিদম যোগ করা সহায়ক হিসেবে।

৪. কী সাপোর্ট এবং রেজিস্ট্যান্স এলাকা নির্ধারণে ডিপ লার্নিংয়ের মতো প্রযুক্তি ব্যবহার করা, যাতে স্টপ লস আরও যুক্তিসঙ্গত হয়।

উপসংহার

এই কৌশলটি হুল নির্দেশক এবং এলএসএমএ-র সমন্বয় প্রয়োগের মাধ্যমে ট্রেন্ডের দিক পরিবর্তন বিচার করে এবং ট্রেন্ড অনুসরণকারী ট্রেডিং বাস্তবায়ন করে। সুবিধাগুলো হলো অপারেশন সহজ, দ্রুত প্রতিক্রিয়া, এবং মাঝারি-নিম্ন ফ্রিকোয়েন্সি কোয়ান্টিটেটিভ ট্রেডিংয়ে ব্যাপকভাবে প্রযোজ্য। ফিল্টারিং শর্ত, সহায়ক বিচার এবং স্টপ লস অ্যালগরিদম ইত্যাদি আরও অপ্টিমাইজ করে আরও ভালো কৌশল ফলাফল অর্জন করা সম্ভব।

- 1