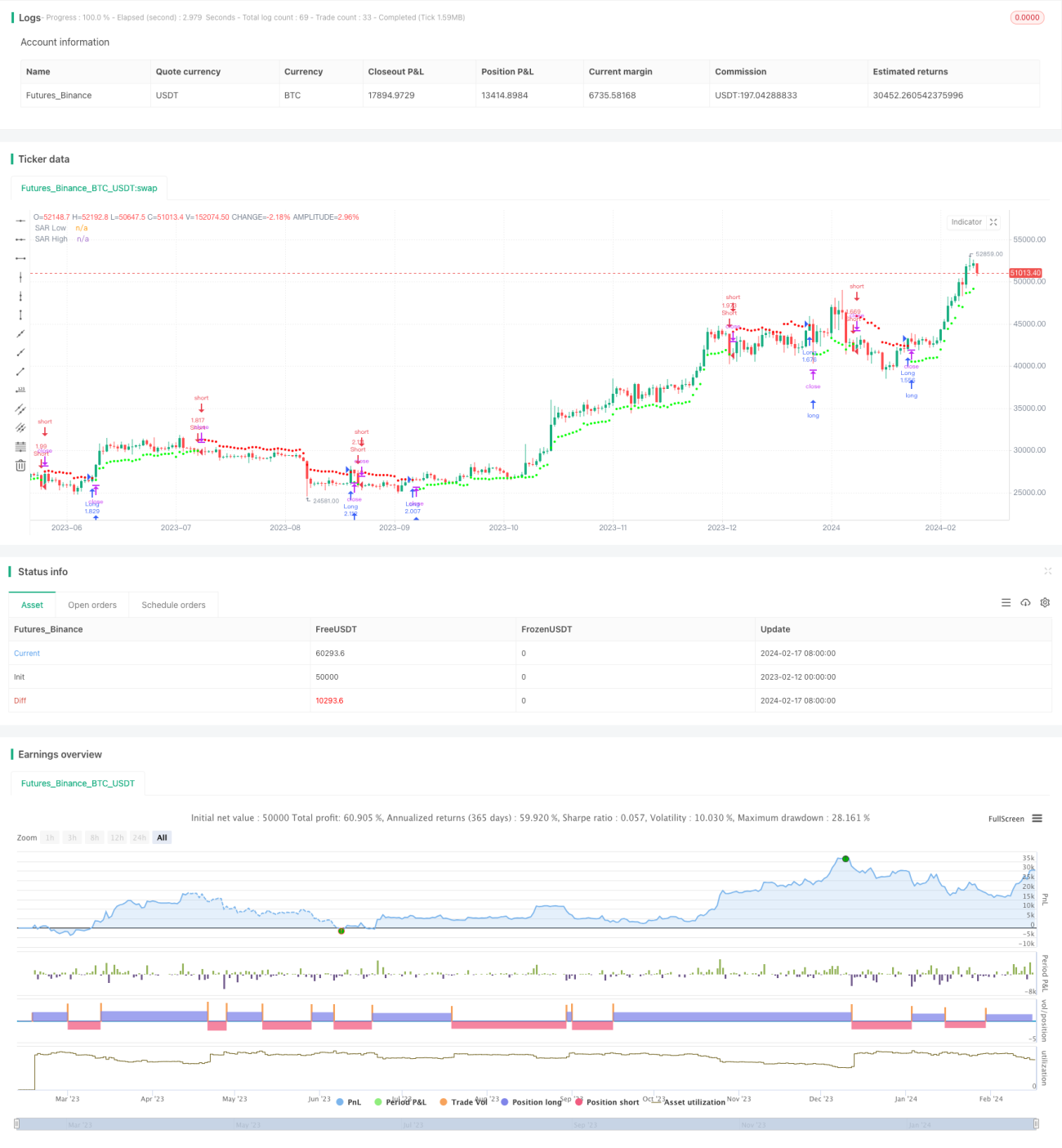

চ্যানেল ব্রেকআউট রিভার্সাল ট্রেডিং কৌশল

সারসংক্ষেপ

চ্যানেল ব্রেকআউট রিভার্সাল ট্রেডিং স্ট্র্যাটেজি হল একটি রিভার্সাল ট্রেডিং কৌশল যা মূল্য চ্যানেল ট্র্যাক করে চলমান টেক-প্রফিট এবং স্টপ-লস পয়েন্ট নির্ধারণ করে। এটি ওয়েটেড মুভিং অ্যাভারেজ পদ্ধতি ব্যবহার করে মূল্য চ্যানেল গণনা করে এবং মূল্য চ্যানেল ভেঙে গেলে লং বা শর্ট পজিশন খোলে।

কৌশলের মূলনীতি

কৌশলটি প্রথমে ওয়াইল্ডার অ্যাভারেজ ট্রু রেঞ্জ (ATR) ইন্ডিকেটর ব্যবহার করে মূল্যের অস্থিরতা গণনা করে। তারপর ATR মানের ভিত্তিতে অ্যাভারেজ রেঞ্জ কনস্ট্যান্ট (ARC) নির্ধারণ করা হয়। ARC হলো মূল্য চ্যানেলের অর্ধেক প্রস্থ। এরপর চ্যানেলের উপরের এবং নিচের সীমানা, অর্থাৎ টেক-প্রফিট এবং স্টপ-লস পয়েন্টগুলি SAR পয়েন্ট নামে গণনা করা হয়। যখন মূল্য উপরের সীমানা ভেঙে যায়, তখন শর্ট করা হয়; যখন নিচের সীমানা ভেঙে যায়, তখন লং করা হয়।

বিস্তারিতভাবে, প্রথমে সাম্প্রতিক Nটি ক্যান্ডেলের ATR গণনা করা হয়। তারপর একটি গুণাঙ্ক দ্বারা ATR গুণ করে ARC পাওয়া যায়। ARC কে গুণাঙ্ক দিয়ে গুণ করলে চ্যানেলের প্রস্থ নিয়ন্ত্রণ করা যায়। ARC কে সাম্প্রতিক Nটি ক্যান্ডেলের সর্বোচ্চ ক্লোজিং মূল্যের সাথে যোগ করে চ্যানেলের উপরের সীমানা (হাই SAR) পাওয়া যায়। ARC-কে সর্বনিম্ন ক্লোজিং মূল্য থেকে বিয়োগ করে চ্যানেলের নিচের সীমানা (লো SAR) পাওয়া যায়। যদি ক্লোজিং মূল্য উপরের সীমানা ভেঙে যায়, তাহলে শর্ট করা হয়; যদি ক্লোজিং মূল্য নিচের সীমানা ভেঙে যায়, তাহলে লং করা হয়।

কৌশলের সুবিধা

- মূল্যের অস্থিরতা ব্যবহার করে স্বতঃসংশোধনযোগ্য চ্যানেল তৈরি করে যা বাজারের পরিবর্তনের সাথে মানিয়ে নিতে পারে।

- রিভার্সাল ট্রেডিং, যা ট্রেন্ড রিভার্সাল বাজারের জন্য উপযুক্ত।

- চলমান টেক-প্রফিট এবং স্টপ-লস, যা মুনাফা লক করতে এবং ঝুঁকি নিয়ন্ত্রণ করতে পারে।

কৌশলের ঝুঁকি

- রিভার্সাল ট্রেডিং সহজেই ফাঁদে পড়তে পারে, তাই প্যারামিটার যথাযথভাবে সমন্বয় করতে হবে।

- বড় মূল্যের ওঠানামার বাজারে পজিশন বন্ধ হয়ে যেতে পারে।

- ভুল প্যারামিটার সেটিং অতিরিক্ত ট্রেডিংয়ের কারণ হতে পারে।

সমাধান:

- ATR পিরিয়ড এবং ARC গুণাঙ্ক অপ্টিমাইজ করে চ্যানেলের প্রস্থ যুক্তিসঙ্গত করা।

- ট্রেন্ড ইন্ডিকেটর যুক্ত করে প্রবেশের সময় ফিল্টার করা।

- ATR পিরিয়ড বাড়িয়ে ট্রেডিং ফ্রিকোয়েন্সি কমানো।

কৌশল উন্নতির দিকনির্দেশ

- ATR পিরিয়ড এবং ARC গুণাঙ্ক অপ্টিমাইজ করা।

- পজিশন খোলার শর্ত যোগ করা, যেমন MACD ইন্ডিকেটর যুক্ত করা।

- স্টপ-লস কৌশল যোগ করা।

সারসংক্ষেপ

চ্যানেল ব্রেকআউট রিভার্সাল ট্রেডিং কৌশল মূল্য চ্যানেল ট্র্যাক করে মূল্যের পরিবর্তন পর্যবেক্ষণ করে, অস্থিরতা বাড়লে বিপরীত দিকে পজিশন খোলে এবং চলমান টেক-প্রফিট ও স্টপ-লস নির্ধারণ করে। এই কৌশলটি মূলত রিভার্সাল-প্রধান সাইডওয়ে বাজারের জন্য উপযুক্ত, যদি রিভার্সাল পয়েন্ট সঠিকভাবে চিহ্নিত করা যায় তবে ভালো বিনিয়োগ রিটার্ন পাওয়া সম্ভব। তবে স্টপ-লস পয়েন্ট খুব শিথিল করা এবং প্যারামিটার অপ্টিমাইজেশনের বিষয়গুলিতে সতর্ক থাকা প্রয়োজন।

- 1