আরএসআই নির্দেশকের লং-শর্ট বিভাজন ট্রেডিং কৌশল

সারসংক্ষেপ

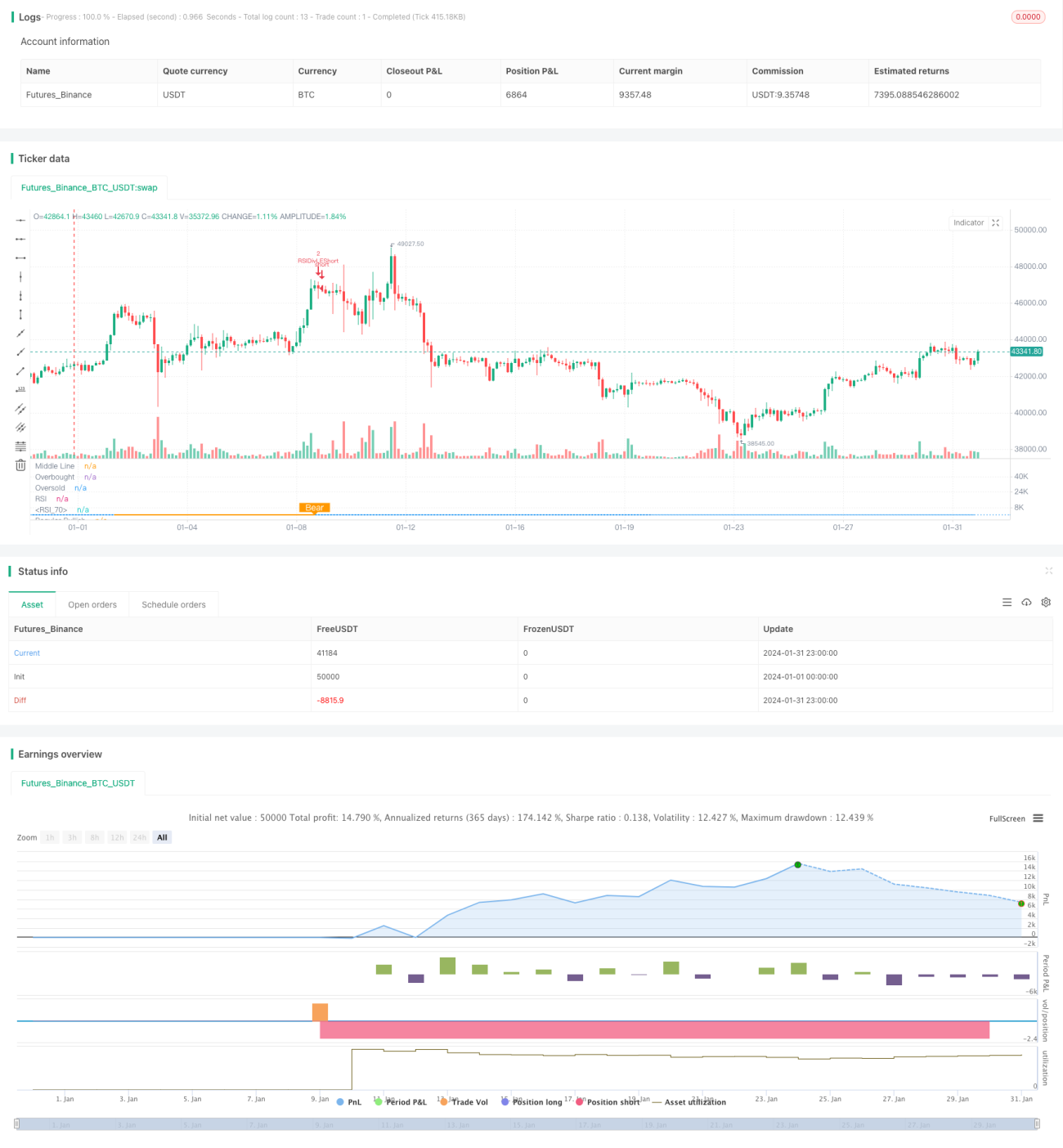

এই কৌশলটি RSI নির্দেশকের মাধ্যমে মাল্টি-শর্ট বিভাজন (মাল্টি এবং শর্ট ডাইভারজেন্স) শনাক্ত করে এবং সেই অনুযায়ী ট্রেডিং সিদ্ধান্ত নেয়। এর মূল ধারণা হলো যখন দাম নতুন নিম্ন তৈরি করে কিন্তু RSI নির্দেশক নতুন উচ্চ তৈরি করে, তখন এটি "মাল্টি বিভাজন" (বুলিশ ডাইভারজেন্স) সংকেত গঠন করে, যা ইঙ্গিত দেয় যে নিচের দিকের স্তর তৈরি হয়েছে, তাই লং পজিশন নেওয়া হয়। অন্যদিকে, যখন দাম নতুন উচ্চ তৈরি করে কিন্তু RSI নির্দেশক নতুন নিম্ন তৈরি করে, তখন এটি "শর্ট বিভাজন" (বেয়ারিশ ডাইভারজেন্স) সংকেত গঠন করে, যা ইঙ্গিত দেয় যে উপরের দিকের স্তর তৈরি হয়েছে, তাই শর্ট পজিশন নেওয়া হয়।

কৌশলের নীতি

এই কৌশলটি প্রধানত RSI নির্দেশক ব্যবহার করে দাম এবং RSI-এর মধ্যে মাল্টি-শর্ট বিভাজন শনাক্ত করে। নির্দিষ্ট পদ্ধতি নিম্নরূপ:

- RSI নির্দেশকের প্যারামিটার ১৩ এবং উৎস ডেটা হলো ক্লোজিং প্রাইস।

- মাল্টি বিভাজনের জন্য বামদিকে রেট্রোস্পেক্ট রেঞ্জ ১৪ দিন এবং ডানদিকে রেট্রোস্পেক্ট রেঞ্জ ২ দিন নির্ধারণ করা হয়।

- শর্ট বিভাজনের জন্য বামদিকে রেট্রোস্পেক্ট রেঞ্জ ৪৭ দিন এবং ডানদিকে রেট্রোস্পেক্ট রেঞ্জ ১ দিন নির্ধারণ করা হয়।

- যখন দাম আরও কম লো তৈরি করে কিন্তু RSI নির্দেশক আরও বেশি লো তৈরি করে, তখন মাল্টি বিভাজনের শর্ত পূর্ণ হয় এবং লং সংকেত তৈরি হয়।

- যখন দাম আরও বেশি হাই তৈরি করে কিন্তু RSI নির্দেশক আরও কম হাই তৈরি করে, তখন শর্ট বিভাজনের শর্ত পূর্ণ হয় এবং শর্ট সংকেত তৈরি হয়।

দাম এবং RSI নির্দেশকের মধ্যে মাল্টি-শর্ট বিভাজন শনাক্ত করার মাধ্যমে দামের প্রবণতার পরিবর্তনের পয়েন্ট আগে থেকেই ধরা যায় এবং সেই অনুযায়ী ট্রেডিং সিদ্ধান্ত নেওয়া যায়।

কৌশলের সুবিধা

এই কৌশলের প্রধান সুবিধাগুলো হলো:

- দাম এবং RSI নির্দেশকের মধ্যে মাল্টি-শর্ট বিভাজন শনাক্ত করে দামের প্রবণতার পরিবর্তনের পয়েন্ট আগে থেকেই নির্ণয় করা যায় এবং ট্রেডিং সুযোগ কাজে লাগানো যায়।

- যেহেতু এটি নির্দেশক বিশ্লেষণের উপর ভিত্তি করে কাজ করে, তাই ব্যক্তিগত আবেগের প্রভাব থাকে না।

- নির্দিষ্ট রেট্রোস্পেক্ট রেঞ্জ ব্যবহার করে বিভাজন শনাক্ত করা হয়, ফলে প্যারামিটার ঘন ঘন পরিবর্তনের প্রয়োজন হয় না।

- ডেইলি RSI-এর মতো অতিরিক্ত শর্ত যুক্ত করলে ভুল ট্রেডের সম্ভাবনা কমে যায়।

ঝুঁকি ও সমাধান

এই কৌশলের কিছু ঝুঁকি রয়েছে:

-

RSI নির্দেশকের ডাইভারজেন্স সবসময় দামের তাৎক্ষণিক বিপরীতমুখী পরিবর্তন নির্দেশ করে না; সময়ের ব্যবধান থাকতে পারে, যার ফলে স্টপ লস ট্রিগার হওয়ার ঝুঁকি থাকে। সমাধান হলো স্টপ লসের পরিমাণ কিছুটা বাড়িয়ে দেওয়া, যাতে দামের ডাইভারজেন্স সংকেত নিশ্চিত করার জন্য যথেষ্ট সময় থাকে।

-

ডাইভারজেন্স দীর্ঘ সময় ধরে চলতে থাকলে ঝুঁকি বাড়ে। সমাধান হলো দীর্ঘমেয়াদী ডেইলি বা উইকলি RSI নির্দেশক ফিল্টার হিসেবে ব্যবহার করা।

-

ডাইভারজেন্সের পরিমাণ খুব ছোট হলে প্রবণতা পরিবর্তন নিশ্চিত করা যায় না; তাই আরও স্পষ্ট RSI ডাইভারজেন্স খুঁজে পেতে রেট্রোস্পেক্ট রেঞ্জ বাড়ানো প্রয়োজন।

কৌশলের উন্নতির সম্ভাবনা

এই কৌশলটি নিম্নলিখিত দিক থেকে আরও উন্নত করা যেতে পারে:

- RSI প্যারামিটার অপ্টিমাইজ করে সর্বোত্তম প্যারামিটার কম্বিনেশন খোঁজা।

- MACD, KDJ-এর মতো অন্যান্য প্রযুক্তিগত নির্দেশক ব্যবহার করে মাল্টি-শর্ট বিভাজন শনাক্ত করার চেষ্টা করা।

- রেঞ্জ ট্রেডিংয়ের সময় অতিরিক্ত ফিল্টার যোগ করে ভুল ট্রেডের সংখ্যা কমানো।

- আরও বেশি টাইমফ্রেমের RSI নির্দেশক যুক্ত করে সর্বোত্তম কম্বিনেশন সংকেত খোঁজা।

সারসংক্ষেপ

RSI মাল্টি-শর্ট ডাইভারজেন্স ট্রেডিং কৌশলটি RSI নির্দেশক এবং দামের মধ্যে মাল্টি-শর্ট বিভাজন শনাক্ত করে দামের প্রবণতার পরিবর্তনের পয়েন্ট নির্ণয় করে এবং সেই অনুযায়ী ট্রেডিং সংকেত তৈরি করে। এই কৌশলটি সহজ এবং ব্যবহারিক; প্যারামিটার সেটিং অপ্টিমাইজ করে এবং ফিল্টার শর্ত যোগ করে লাভের সম্ভাবনা আরও বাড়ানো যায়। সামগ্রিকভাবে, RSI মাল্টি-শর্ট ডাইভারজেন্স কৌশলটি একটি অত্যন্ত কার্যকর কোয়ান্টিটেটিভ ট্রেডিং কৌশল।

- 1