Trenddurchbruch-Gleitender-Durchschnitt-Verfolgungsstrategie

Überblick

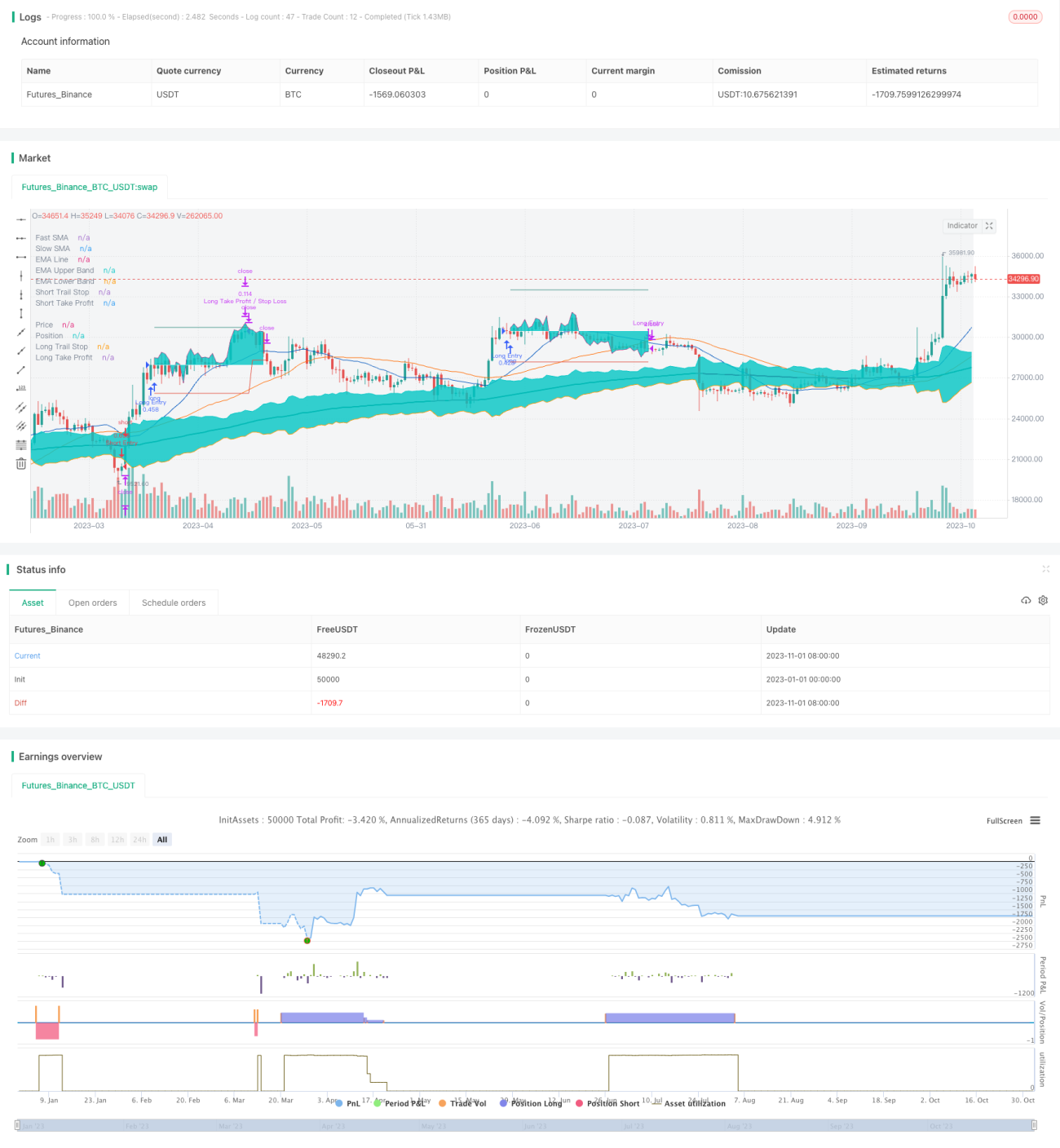

Diese Strategie nutzt Golden Cross und Dead Cross von einfachen gleitenden Durchschnitten (SMA), um die Trendrichtung zu bestimmen. Zu Beginn eines Trends wird die gesamte Position long oder short eröffnet, und es werden Stop-Loss- und Take-Profit-Orders zur Risikokontrolle gesetzt. Nach dem Einstieg wird der Trend mithilfe des gleitenden Durchschnitts kontinuierlich verfolgt; bei Trendumkehr wird rechtzeitig der Stop-Loss ausgelöst. Die Strategie verfügt über konfigurierbare Module für Stop-Loss, Take-Profit und Positionsmanagement, sodass die Parameter flexibel an verschiedene Instrumente angepasst werden können.

Strategieprinzip

Die Strategie erkennt den Beginn und das Ende eines Trends hauptsächlich durch Golden Cross und Dead Cross der einfachen gleitenden Durchschnitte. Zunächst wird die Trendrichtung anhand der Beziehung zwischen dem schnellen SMA (z. B. 21-Tage-Linie) und dem langsamen SMA (z. B. 49-Tage-Linie) bestimmt. Wenn der schnelle SMA den langsamen SMA von unten nach oben kreuzt, wird ein Aufwärtstrend angenommen und eine Long-Position eröffnet. Wenn der schnelle SMA den langsamen SMA von oben nach unten kreuzt, wird ein Abwärtstrend angenommen und eine Short-Position eröffnet.

Nach dem Einstieg überwacht die Strategie in Echtzeit die Beziehung zwischen dem Preis und dem SMA. Wenn der Preis den SMA von oben nach unten durchbricht, wird der Aufwärtstrend als beendet angesehen und die Long-Position geschlossen. Wenn der Preis den SMA von unten nach oben durchbricht, wird der Abwärtstrend als beendet angesehen und die Short-Position geschlossen.

Zur Risikokontrolle werden bei der Eröffnung einer Position gleichzeitig Stop-Loss- und Take-Profit-Orders gesetzt. Der Stop-Loss-Abstand wird auf Basis des ATR (Average True Range) festgelegt, während der Take-Profit-Abstand wahlweise als Prozentsatz oder auf Basis des ATR eingestellt werden kann. Nach der Eröffnung verfolgt der Stop-Loss den Preis in Echtzeit, um einen Trendfolgeeffekt zu erzielen. Wenn der Take-Profit erreicht wird, wird ein Teil der Position geschlossen; die verbleibende Position wird weiterverfolgt, bis die gesamte Position geschlossen ist.

Die Strategie verfügt außerdem über ein Positionsmanagement-Modul, das die Kapitalnutzung pro Trade begrenzt, um das Risiko pro Einzelposition zu kontrollieren. Gleichzeitig kann eine maximale Verlustbegrenzung (Max Drawdown) das Gesamtrisiko der Strategie steuern.

Vorteile der Strategie

- Verwendung von gleitenden Durchschnitten zur Trendbestimmung, einfaches und verständliches Prinzip

- Echtzeit-Trailing-Stop-Loss nach dem Einstieg, um einen Großteil der Gewinne zu sichern

- Konfigurierbare Stop-Loss- und Take-Profit-Methoden, anpassbar an verschiedene Instrumente

- Kontrolliertes Risiko pro Trade, keine Vollpositions-Transaktionen

- Maximale Verlustbegrenzung, um Gesamtverluste der Strategie zu begrenzen

Risiken und Lösungen

- Der Crossover zweier gleitender Durchschnitte hat eine gewisse Verzögerung, sodass der optimale Einstiegspunkt zu Beginn eines Trends möglicherweise verpasst wird

- Parameter müssen wiederholt angepasst werden, um verschiedene Kombinationen von SMA-Zeiträumen zu testen

- Der SMA-Crossover weist eine gewisse Fehlerquote auf, die Einstiegsgenauigkeit kann nicht 100% betragen

- Der Trailing-Stop-Loss kann leicht durchbrochen werden und nicht den gesamten Gewinn sichern

- Der Stop-Loss-Abstand sollte angemessen weit gewählt werden, um dem Preis eine gewisse Korrekturspanne zu geben

- Die maximale Verlustbegrenzung könnte zu konservativ sein und Gewinnchancen einschränken

- Die maximale Verlustquote kann etwas gelockert werden, um der Strategie mehr Fehlertoleranz zu geben

Optimierungsmöglichkeiten

- Testen verschiedener Parameterkombinationen, um die optimalen SMA-Zeiträume zu finden

- Hinzufügen von Trendstärkeindikatoren zur Verbesserung der Einstiegsgenauigkeit

- Optimierung der Stop-Loss-Strategie, um im Trend möglichst gewinnbringend nachzuziehen

- Testen verschiedener Take-Profit-Strategien zur Auswahl des optimalen Gewinnziels

- Optimierung des Positionsmanagements zur Steigerung der Kapitalnutzungseffizienz

- Anpassung der maximalen Verlustbegrenzung, um Ertrag und Risiko auszugleichen

Zusammenfassung

Insgesamt ist diese Strategie eine sehr geeignete Einstiegsstrategie für Anfänger – das Prinzip ist einfach, leicht zu verstehen und zu erlernen. Gleichzeitig verfügt sie über angemessene Risikokontrollfähigkeiten, die die Wahrscheinlichkeit großer Verluste verringern. Durch Parameteroptimierung können gute Ergebnisse erzielt werden. Allerdings führen ihre grundlegenden Defekte dazu, dass sie keine hochpräzisen Operationen ermöglicht. Es wird empfohlen, sie als Übungsstrategie für Anfänger zu nutzen, aber sie ist nicht geeignet für Trader, die hohe Effizienz und eine hohe Gewinnrate anstreben. Um bessere Handelsergebnisse zu erzielen, sollte man nach Strategien mit stärkerer Prognosefähigkeit suchen.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1