Multiple-MA-Momentum-Handelsstrategie

Übersicht

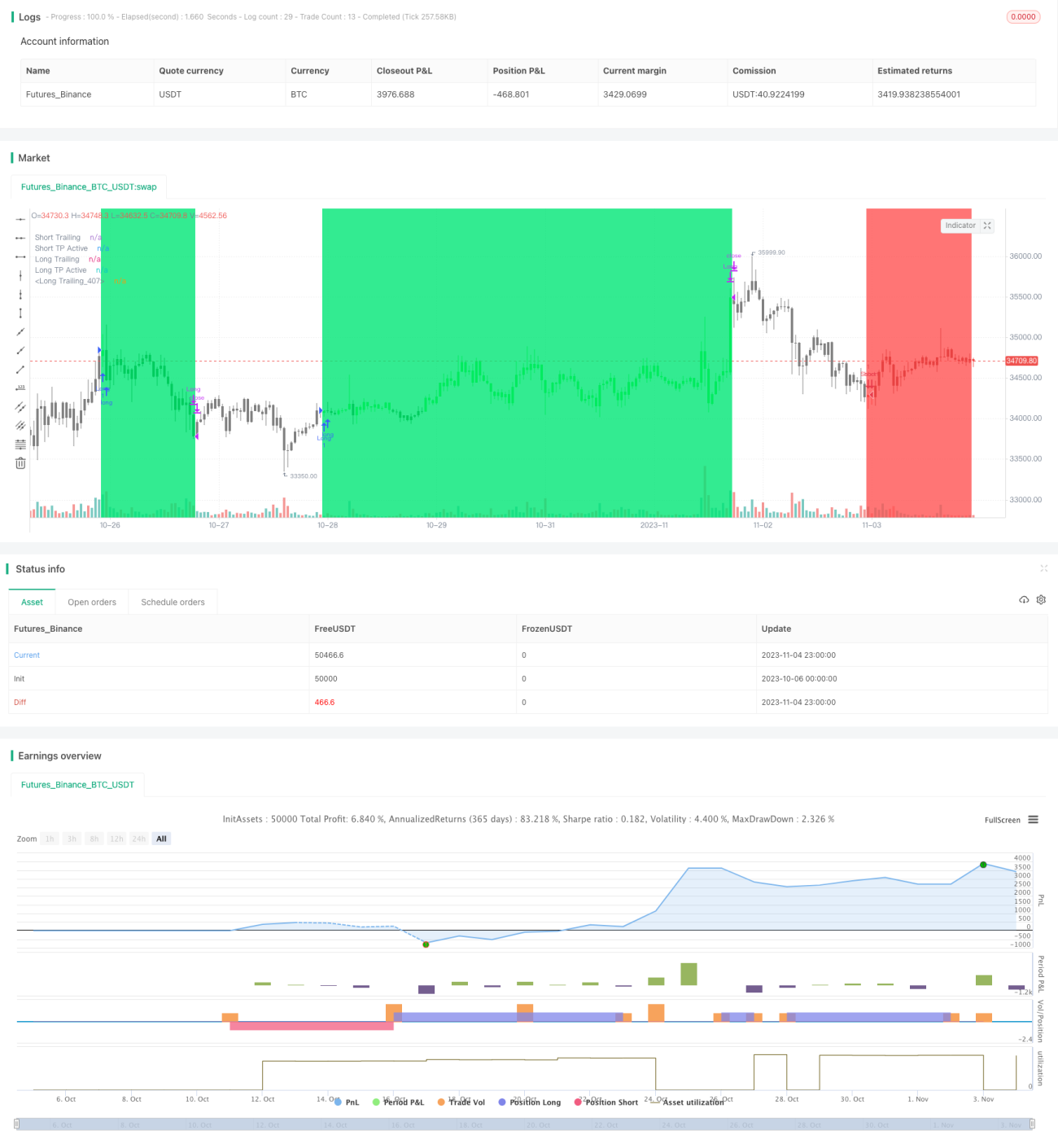

Diese Handelsstrategie kombiniert mehrere gleitende Durchschnitte mit einem Momentum-Indikator, um die Richtung und Stärke eines Trends zu identifizieren. Positionen werden zu Beginn eines Trends eröffnet, anschließend werden Trailing-Stop-Loss und Trailing-Take-Profit eingesetzt, um Gewinne zu optimieren und Risiken zu kontrollieren. Ziel ist es, in mittel- bis langfristigen Trends signifikante Kursbewegungen zu erfassen.

Funktionsweise der Strategie

-

Zwei Gruppen gleitender Durchschnitte mit unterschiedlichen Parametern bilden eine schnelle und eine langsame Linie:

- Die schnelle Linie besteht aus einem 5-Perioden exponentiellen gleitenden Durchschnitt (EMA) und einem 25-Perioden gewichteten gleitenden Durchschnitt (WMA) und repräsentiert den kurzfristigen Trend.

- Die langsame Linie besteht aus einem 28-Perioden EMA und einem 72-Perioden WMA und repräsentiert den mittel- bis langfristigen Trend.

-

Wenn die schnelle Linie die langsame Linie von unten nach oben kreuzt, bedeutet dies, dass der kurzfristige Trend stärker wird als der mittel- bis langfristige Trend – dies ist ein Einstiegssignal.

-

In Kombination mit dem Momentum-Indikator RSI erfolgt der Einstieg nur, wenn der RSI auf einem niedrigen Niveau (Kaufsignal) oder auf einem hohen Niveau (Verkaufssignal) liegt, um Fehlausbrüche zu filtern.

-

Nach dem Einstieg wird ein Trailing-Stop-Loss verwendet, um Verluste zu begrenzen, und ein Trailing-Take-Profit, um Gewinne zu sichern.

-

Wenn die schnelle Linie die langsame Linie von oben nach unten kreuzt, deutet dies auf eine Trendumkehr hin. Dann wird die Position via Stop-Loss oder Take-Profit geschlossen.

Vorteile

- Die Kombination zweier gleitender Durchschnitte filtert Rauschen und identifiziert Richtung und Stärke des Trendverlaufs.

- Positionen werden nur zu Beginn eines Trends eröffnet, wodurch unnötige Verluste durch Fehlausbrüche vermieden werden.

- Der Momentum-Indikator filtert die Einstiegssignale und verbessert deren Qualität.

- Der Trailing-Stop-Loss begrenzt Einzelverluste und reduziert die Auswirkungen einzelner schlechter Trades.

- Der Trailing-Take-Profit sichert Gewinne und ermöglicht in guten Marktphasen zusätzliche Gewinne.

Risiken

- Die doppelten gleitenden Durchschnitte können an Trendwenden eine Verzögerung aufweisen, sodass Umkehrmöglichkeiten verpasst werden.

- Lösung: Die Perioden der gleitenden Durchschnitte können verkürzt werden, um sie empfindlicher zu machen.

- Fehlausbrüche können zu unnötigen Einstiegen führen.

- Lösung: Es können weitere Filterindikatoren hinzugefügt werden.

- Der Abstand von Stop-Loss oder Take-Profit ist möglicherweise nicht optimiert – zu weit oder zu eng.

- Lösung: Durch Backtesting die Parameter optimieren, um den optimalen Abstand zu finden.

- Die Strategie ist richtungsabhängig und eignet sich nur für Trendmärkte.

- Lösung: Je nach Marktlage (z.B. anhand des Gesamtmarktes) entscheiden, ob die Strategie angewendet wird.

Optimierungsmöglichkeiten

- Optimierung der Parameter der gleitenden Durchschnitte, um die beste Parameterkombination zur Darstellung des Trends zu finden.

- Hinzufügen von Trendfiltern wie ATR (dynamischer Stop-Loss), Volume-Weighted Average Price (VWAP) oder On-Balance-Volume (OBV).

- Optimierung der Stop-Loss- und Take-Profit-Parameter, um die beste Kombination zu finden.

- Einbeziehung einer Beurteilung des übergeordneten Marktes, um zu entscheiden, ob die Strategie aktiviert wird.

- Integration mehrerer Zeitebenen (Multi-Timeframe-Analyse), wobei die Richtung des übergeordneten Trends als Leitlinie für die kurzfristige Strategie dient.

Zusammenfassung

Diese Strategie kombiniert gleitende Durchschnitte mit einem Momentum-Indikator, um frühzeitige Einstiege in entstehende Trends zu identifizieren und durch zeitnahe Stop-Loss- und Take-Profit-Setzung Risiko- und Gewinnmanagement zu betreiben. Obwohl noch Anpassungen der Parameter und Regeln erforderlich sind, um sich an breitere Marktbedingungen anzupassen, bietet sie bereits ein grundlegendes Gerüst und eine Richtung für die Erfassung mittel- bis langfristiger Trends. Durch kontinuierliche Optimierung kann diese Strategie zu einem stabilen und effizienten Trendfolgeansatz heranwachsen.

- 1