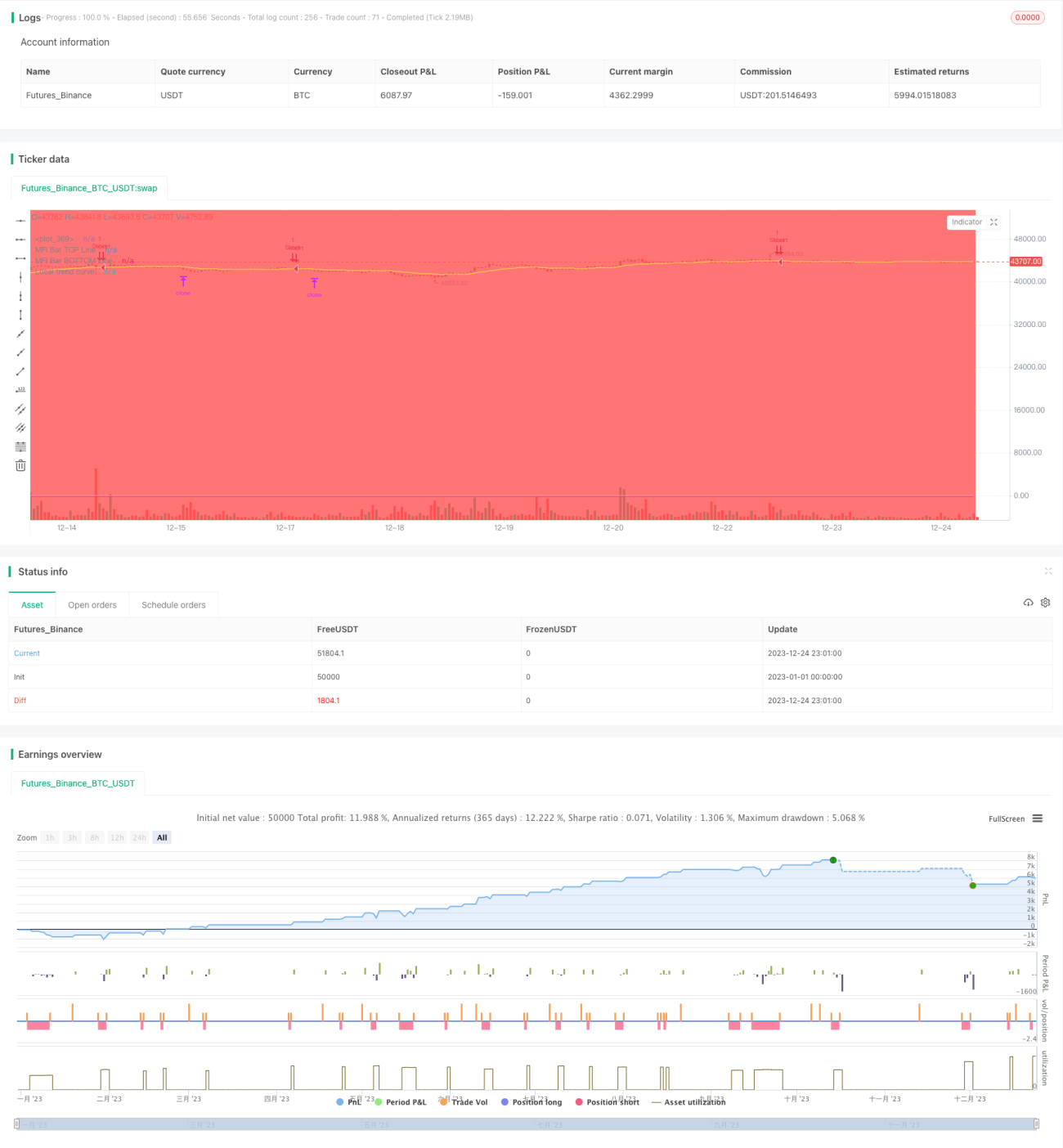

Quantitative Handelsstrategie basierend auf einem doppelten Trendfilter

Übersicht

Dies ist eine Strategie für den quantitativen Handel, die einen doppelten Trendfilter verwendet. Die Strategie kombiniert einen globalen Trendfilter und einen lokalen Trendfilter, um sicherzustellen, dass nur in die Richtung des Trends eröffnet wird. Darüber hinaus enthält die Strategie mehrere andere Filterbedingungen wie RSI-Filter, Preisfilter, Steigungsfilter usw., um die Zuverlässigkeit der Handelssignale weiter zu verbessern. Beim Ausstieg sind in der Strategie voreingestellte Stop-Loss- und Take-Profit-Niveaus enthalten. Insgesamt handelt es sich um eine stabile und präzise quantitative Handelsstrategie.

Strategieprinzip

Die Kernlogik dieser Strategie basiert auf dem doppelten Trendfilter. Der globale Trendfilter beurteilt den allgemeinen Markttrend anhand eines höherperiodischen EMA, während der lokale Trendfilter den lokalen Trend anhand eines niedrigerperiodischen EMA bewertet. Eine Position wird nur dann eröffnet, wenn beide Filter denselben Trend anzeigen.

Konkret berechnet die Strategie die EMA-Linie von BTCUSDT, um zu bestimmen, ob sich der Gesamtmarkt in einem Aufwärts- oder Abwärtstrend befindet – dies ist der globale Trendfilter. Gleichzeitig berechnet die Strategie die EMA-Linie des aktuellen Kontrakts, um den lokalen Markttrend zu beurteilen – dies ist der lokale Trendfilter. Wenn beide Filter denselben Trend anzeigen, wird in Kombination mit mehreren anderen Hilfsfiltern ein Handelssignal generiert, und die Strategie eröffnet mit voreingestellten Take-Profit- und Stop-Loss-Preisen.

Nach der Bestimmung des Handelssignals platziert die Strategie sofort eine Order zur Eröffnung. Gleichzeitig werden Take-Profit- und Stop-Loss-Preise voreingestellt. Wenn der Preis diese Niveaus erreicht, wird die Strategie automatisch den Gewinn mitnehmen oder den Verlust begrenzen.

Vorteilsanalyse

Dies ist eine stabile und zuverlässige quantitative Handelsstrategie mit den folgenden Hauptvorteilen:

-

Der doppelte Trendfilter-Mechanismus filtert die meisten Fehlsignale heraus und macht die Handelssignale zuverlässiger und präziser.

-

Die Kombination mehrerer Hilfsfilter wie RSI-Filter, Preisfilter usw. verbessert die Signalqualität weiter.

-

Die automatische Berechnung von Take-Profit- und Stop-Loss-Niveaus erfordert keine manuelle Überwachung und reduziert das Handelsrisiko.

-

Die Strategieparameter können individuell angepasst werden, um sich an verschiedene Handelsinstrumente anzupassen, was eine hohe Anpassungsfähigkeit bietet.

-

Die Strategielogik ist klar und leicht verständlich, was Optimierungen und Verbesserungen erleichtert und ein großes Erweiterungspotenzial bietet.

Risikoanalyse

Obwohl die Strategie viele Vorteile hat, bestehen dennoch gewisse Handelsrisiken, die sich hauptsächlich auf Folgendes konzentrieren:

-

Der Zeitpunkt des Einstiegs, der durch den doppelten Trendfilter bestimmt wird, ist möglicherweise nicht präzise. Dies kann durch Anpassung der Filterparameter optimiert werden.

-

Die Festlegung von Take-Profit- und Stop-Loss-Preisen kann ungenau sein, was zu einem vorzeitigen Gewinnmitnahme oder Verlustbegrenzung führen kann. Verschiedene Parameterkombinationen können getestet werden, um die optimale Lösung zu finden.

-

Eine ungeeignete Wahl des Handelsinstruments oder Zeitrahmens kann dazu führen, dass die Strategie unwirksam wird. Es wird empfohlen, für verschiedene Handelsinstrumente separate Parameteroptimierungen und Tests durchzuführen.

-

Es besteht ein gewisses Risiko der Überanpassung. Die Strategie sollte in mehreren Marktumgebungen rückgetestet werden, um ihre Robustheit sicherzustellen.

Optimierungsmöglichkeiten

Die Strategie kann hauptsächlich in folgenden Bereichen optimiert werden:

-

Anpassung der Parameter des doppelten Filters, um die optimale Parameterkombination zu finden.

-

Testen und Auswahl der besten Hilfsfilter.

-

Optimierung des Take-Profit- und Stop-Loss-Algorithmus, um ihn intelligenter zu gestalten.

-

Versuch, maschinelles Lernen einzuführen, um eine dynamische Parameteranpassung der Strategie zu ermöglichen.

-

Rücktests über mehrere Handelsinstrumente und längere Zeiträume, um die Stabilität der Strategie zu verbessern.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine stabile, präzise und leicht optimierbare quantitative Handelsstrategie. Sie verwendet einen doppelten Trendfilter in Kombination mit mehreren Hilfsfiltern, um Handelssignale zu generieren, die den Großteil des Rauschens herausfiltern und die Signale präziser und zuverlässiger machen. Gleichzeitig sind Take-Profit- und Stop-Loss-Einstellungen integriert, um das Handelsrisiko zu reduzieren. Diese Strategie hat einen hohen praktischen Wert und kann nach Optimierung und Validierung direkt im Live-Handel eingesetzt werden. Sie bietet auch ein großes Erweiterungspotenzial und ist eine quantitative Strategie, die es wert ist, eingehend untersucht zu werden.

- 1