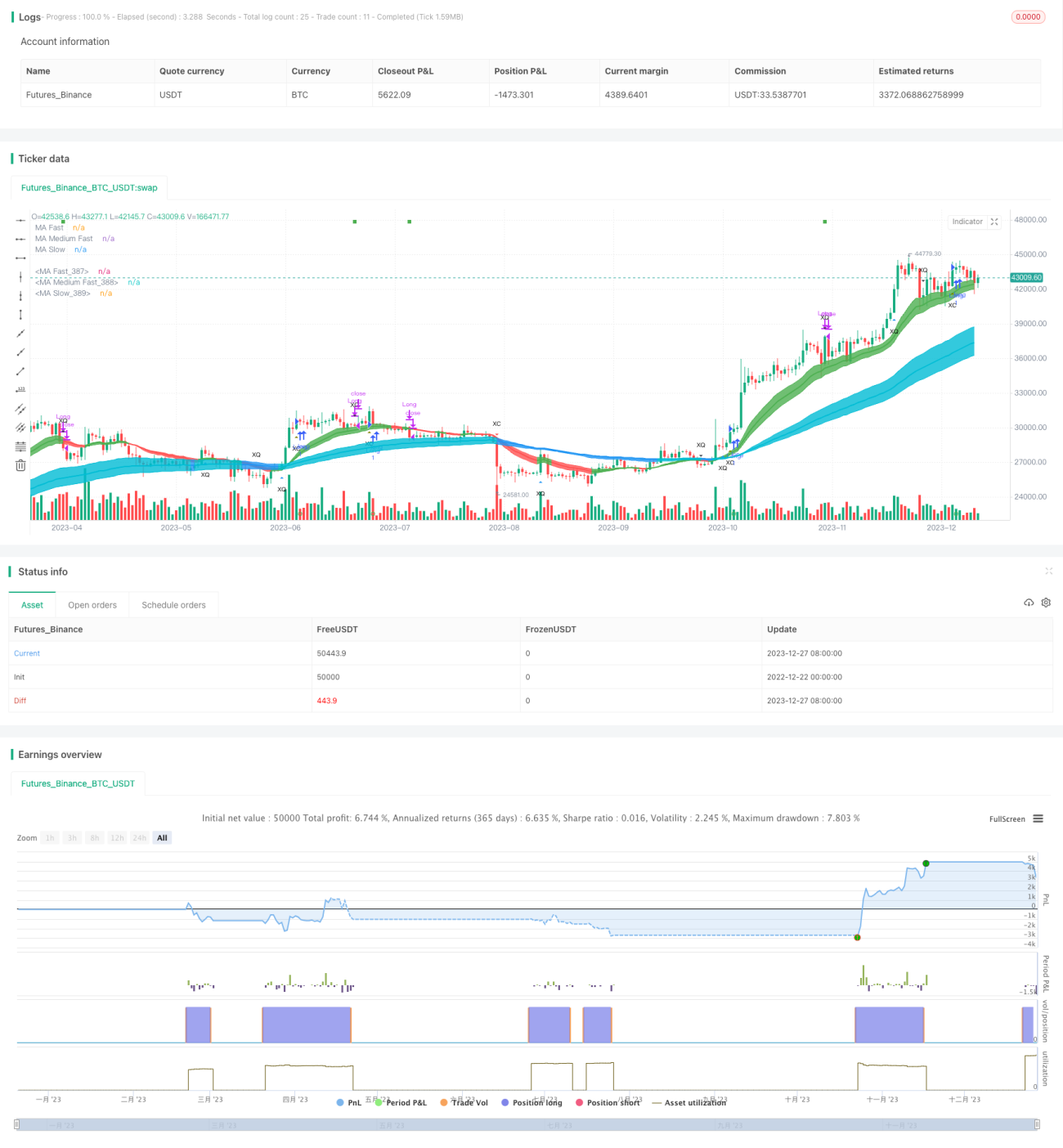

Trendfolgestrategie basierend auf QQE und MA

Übersicht

Diese Strategie ist eine Trendfolgestrategie auf Basis des QQE-Indikators (Qualitative Quantitative Estimation, qualitative quantitative Schätzung) und gleitender Durchschnitte. Sie nutzt die Kreuzung des schnellen QQE-Indikators sowie die Richtungsfilterung durch gleitende Durchschnitte, um die Trendrichtung zu bestimmen und Kaufs- und Verkaufssignale zu generieren.

Die Strategie kann wahlweise drei Arten von QQE-Kreuzungen zur Signalbestimmung verwenden: (1) Kreuzung des geglätteten RSI-Indikators mit der Nulllinie; (2) Kreuzung des geglätteten RSI-Indikators mit der schnellen QQE-Linie; (3) Verlassen des RSI-Schwellenkanals durch den geglätteten RSI-Indikator. Standardmäßig wird die dritte Kreuzung zum Eröffnen von Positionen und die zweite Kreuzung zum Schließen von Positionen verwendet.

Bei Kaufs- und Verkaufssignalen kann optional eine zusätzliche Filterung durch gleitende Durchschnitte erfolgen: Ein Signal wird nur dann generiert, wenn der Schlusskurs über (unter) dem schnellen gleitenden Durchschnitt liegt und der schnelle gleitende Durchschnitt über (unter) dem langsamen gleitenden Durchschnitt liegt.

Diese Strategie eignet sich für den Signal-gegen-Signal-Modus im automatisierten Programmhandel.

Prinzip

Der Kernindikator der Strategie ist der QQE, dessen Berechnungsformel wie folgt lautet:

Wilders_Period = RSILen * 2 - 1

Rsi = rsi(close, RSILen)

RSIndex = ema(Rsi, SF)

AtrRsi = abs(RSIndex - RSIndex[1])

MaAtrRsi = ema(AtrRsi, Wilders_Period)

DeltaFastAtrRsi = ema(MaAtrRsi, Wilders_Period) * QQEfactor

newshortband = RSIndex + DeltaFastAtrRsi

newlongband = RSIndex - DeltaFastAtrRsi

Dabei sind RSILen die Längenperiode des RSI und SF der Glättungsfaktor des RSI. Der QQE ist im Wesentlichen ein geglätteter RSI. Er berechnet obere und untere Kanäle über einen schnellen ATR. Überschreitet der Kurs den Kanal, wird dies als Kauf- oder Verkaufschance gewertet.

Die Strategie verwendet drei QQE-Kreuzungen zur Identifizierung von Handelssignalen:

- Kreuzung des geglätteten RSI-Indikators mit der Nulllinie (XZ)

QQEzlong = RSIndex >= 50 ? QQEzlong + 1 : 0

QQEzshort = RSIndex < 50 ? QQEzshort + 1 : 0

- Kreuzung des geglätteten RSI-Indikators mit dem schnellen QQE-Indikator (XQ), ähnlich einem vorzeitigen Schwingsignal

QQExlong = FastAtrRsiTL < RSIndex ? QQExlong + 1 : 0

QQExshort = FastAtrRsiTL > RSIndex ? QQExshort + 1 : 0

- Verlassen des Schwellenkanals durch den geglätteten RSI-Indikator (XC), ähnlich einem bestätigten Schwingsignal

threshhold = 10

QQEclong = RSIndex > (50 + threshhold) ? QQEclong + 1 : 0

QQEcshort = RSIndex < (50 - threshhold) ? QQEcshort + 1 : 0

Wahlweise können eine oder mehrere der obigen drei Kreuzungen zur Identifizierung von Kauf-/Verkaufssignalen sowie von Schließungssignalen verwendet werden.

Bei Kaufs- und Verkaufssignalen kann optional eine zusätzliche Filterung durch gleitende Durchschnitte erfolgen:

// Filterbedingungen

QQEflong = close > ma_medium und

ma_medium > ma_slow und

ma_fast > ma_medium

QQEfshort = close < ma_medium und

ma_medium < ma_slow und

ma_fast < ma_medium

Dies hilft, Fehlsignale in Seitwärtsmärkten zu vermeiden.

Die Strategie eignet sich für den automatisierten Handel, indem unterschiedliche QQE-Kreuzungen zum Eröffnen und Schließen von Positionen verwendet werden:

Eröffnungssignal = XC oder XQ oder XZ

Schließsignal = XQ oder XZ

Vorteile

Die Strategie bietet folgende Vorteile:

-

Verwendung des QQE-Indikators zur Bestimmung von Trends und Kreuzungssignalen. Der QQE selbst besitzt glättende und entrauschende Eigenschaften, wodurch Fehlsignale reduziert werden können.

-

Die Kombination mit gleitenden Durchschnitten zur Filterung kann Fehlsignale in Seitwärtsmärkten weiter vermeiden und die Signalqualität verbessern.

-

Die Möglichkeit, verschiedene QQE-Kreuzungen zum Eröffnen und Schließen von Positionen zu wählen, ermöglicht einen automatisierten Handel.

-

Aufgrund der Verzögerung des geglätteten RSI-Indikators werden Kauf- und Verkaufssignale nicht neu gezeichnet.

-

Die Optimierung auf verschiedenen Zeitrahmen ist möglich, um die besten Parameterkombinationen zu finden.

Risiken

Die Strategie birgt auch gewisse Risiken:

-

Bei Trendumkehrungen können Fehlsignale auftreten, weshalb ein Stop-Loss zur Risikokontrolle erforderlich ist.

-

Eine falsche Parametereinstellung kann die Performance der Strategie beeinträchtigen. Es sind mehrere Test- und Optimierungsrunden erforderlich, um die optimalen Parameter zu finden.

-

Parameter für verschiedene Produkte und Zeitrahmen müssen separat getestet und optimiert werden.

-

Der mechanische Handel ist mit Drawdowns und Verlustserien verbunden, sodass ein Risikomanagement erforderlich ist.

Die entsprechenden Lösungen lauten wie folgt:

-

Setzen Sie einen Stop-Loss, um auszusteigen, wenn der Verlust ein bestimmtes Niveau erreicht.

-

Testen Sie verschiedene Parameterkombinationen im Detail, um die optimalen Parameter zu finden.

-

Passen Sie die Parameter basierend auf den Eigenschaften des Produkts und des Zeitrahmens an.

-

Betreiben Sie ein solides Risikomanagement: Staffeln Sie den Positionsaufbau und kontrollieren Sie die Größe der Einzelpositionen.

Optimierungsrichtungen

Die Strategie kann in folgenden Bereichen optimiert werden:

-

Optimierung der QQE-Parameter, einschließlich RSI-Länge, RSI-Glättungslänge, schnelle ATR-Länge usw., um die optimale Parameterkombination zu finden.

-

Optimierung der Parameter gleitender Durchschnitte: Anpassung von Perioden, Typen usw., um die beste Übereinstimmung mit dem QQE-Indikator zu erzielen.

-

Testen verschiedener QQE-Kreuzungen für Eröffnung und Schließung von Positionen, um die stabilste Kombination zu finden.

-

Feinabstimmung der Parameter je nach Produkt und Handelszeitrahmen. Intraday-Handel kann mit kürzeren Perioden die Parameter verbessern.

-

Hinzufügen eines Stop-Loss-Mechanismus, der aussteigt, wenn der Verlust einen bestimmten Prozentsatz erreicht.

-

Reduzierung der Positionsgrößen und Testen verschiedener Positionsmanagement-Methoden.

Zusammenfassung

Diese Strategie integriert den QQE-Indikator zur Bestimmung von Trends und Kreuzungssignalen sowie gleitende Durchschnitte zur Filterung, um Handelssignale zu generieren. Im Live-Handel kann durch Anpassung der Parameter die Signalqualität optimiert werden; in Kombination mit strengem Risikomanagement können Risiken kontrolliert werden. Die Strategie eignet sich für den Signal-gegen-Signal-Modus im automatisierten Handel und kann auch als Hilfsmittel im diskretionären Handel dienen. Durch Parameteroptimierung und Regelanpassung kann sie an verschiedene Marktumgebungen angepasst werden.

- 1