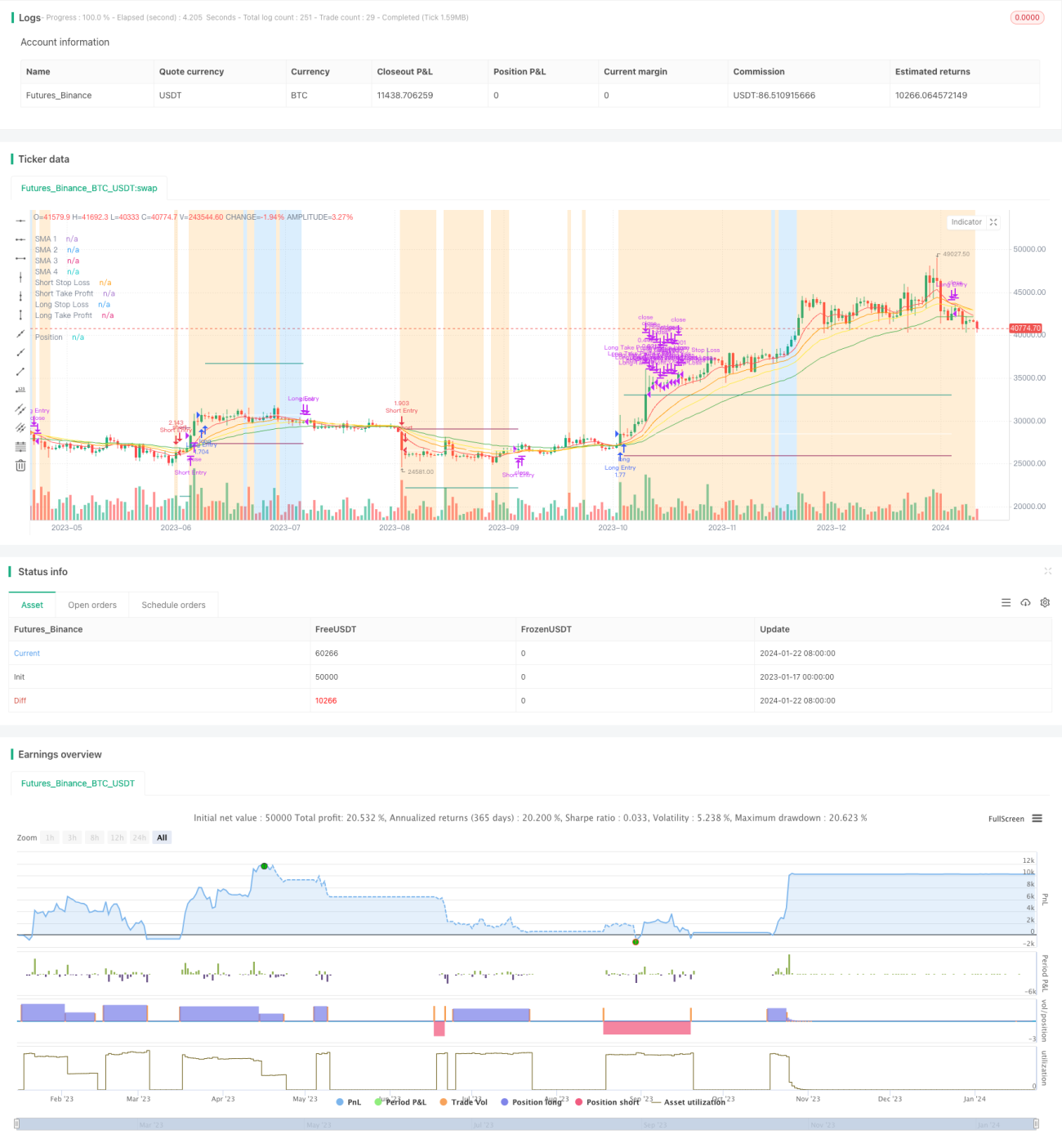

Auf gleitenden Durchschnitten basierende Trendfolgestrategie

Übersicht

Diese Strategie ist eine einfache Trendfolgestrategie basierend auf gleitenden Durchschnitten. Sie vergleicht die Größenverhältnisse gleitender Durchschnitte unterschiedlicher Perioden, um die aktuelle Trendrichtung und die Dauer des Trends zu bestimmen. Wenn der kurzfristige gleitende Durchschnitt den langfristigen gleitenden Durchschnitt von unten nach oben kreuzt, wird eine Long-Position eröffnet. Wenn der kurzfristige gleitende Durchschnitt den langfristigen von oben nach unten kreuzt, wird eine Short-Position eröffnet. Zudem werden Stop-Loss- und Take-Profit-Punkte festgelegt, um das Risiko zu kontrollieren.

Strategieprinzip

Die Strategie verwendet vier gleitende Durchschnitte mit unterschiedlichen Perioden: 5-Tage-Linie, 10-Tage-Linie, 15-Tage-Linie und 25-Tage-Linie. Diese vier gleitenden Durchschnitte werden als MA1, MA2, MA3 und MA4 bezeichnet. MA1 ist die kürzeste, MA4 die längste Periode.

Wenn MA1 > MA2 > MA3 > MA4 ist, deutet dies auf einen Aufwärtstrend hin. In diesem Fall wird long gegangen. Wenn MA1 < MA2 < MA3 < MA4 ist, deutet dies auf einen Abwärtstrend hin. In diesem Fall wird short gegangen.

Die Eröffnungsbedingungen für Long- und Short-Positionen müssen zusätzlich den ATR-Stopfilter erfüllen, d. h. der ATR-Wert muss größer sein als der 40-Perioden-einfache gleitende Durchschnitt des ATR. Dies verhindert falsche Signale bei zu geringer Preisschwankung.

Vorteile der Strategie

Die Strategie hat folgende Vorteile:

- Einfach und leicht verständlich, unkompliziert umsetzbar.

- Die Verwendung mehrerer gleitender Durchschnitte zur Trendbestimmung ist zuverlässig.

- Durch die Festlegung von Take-Profit und Stop-Loss kann der maximale Verlust pro Trade wirksam begrenzt werden.

- Der ATR-Stopfilter vermeidet falsche Signale bei zu geringer Preisschwankung.

Risikoanalyse

Die Strategie birgt auch folgende Risiken:

- In stark schwankenden Märkten kann es zu Fehlsignalen kommen.

- Eine ungeeignete Parametereinstellung (z. B. Perioden der gleitenden Durchschnitte) kann zu einer schlechten Strategieleistung führen.

- Fundamentaldaten und wichtige Nachrichten, die den Kurs beeinflussen, werden nicht berücksichtigt.

Um diese Risiken zu verringern, können die Parameter optimiert oder zusätzliche Filterbedingungen hinzugefügt werden, um die Stabilität der Strategie zu erhöhen.

Optimierungsmöglichkeiten

Die Optimierungsansätze für diese Strategie sind:

- Testen verschiedener Parameterkombinationen der gleitenden Durchschnitte, um die optimalen Parameter zu finden.

- Hinzufügen weiterer technischer Indikatorfilter wie MACD, KDJ usw., um die Zuverlässigkeit der Signale zu bewerten.

- Hinzufügen eines Volumenfilters: Nur bei erhöhtem Handelsvolumen wird gehandelt.

- Feinabstimmung der Parameter je nach unterschiedlichen Instrumenten.

- Integration von Machine-Learning-Algorithmen zur Signalauswertung.

Zusammenfassung

Insgesamt handelt es sich bei dieser Strategie um eine relativ einfache Trendfolgestrategie. Sie nutzt gleitende Durchschnitte zur Trendbestimmung und setzt angemessene Take-Profit- und Stop-Loss-Werte zur Risikokontrolle. Es gibt noch viel Raum für Optimierungen, z. B. durch Parameteranpassungen oder das Hinzufügen von Filtern, um die Stabilität und Rentabilität der Strategie weiter zu verbessern.

- 1