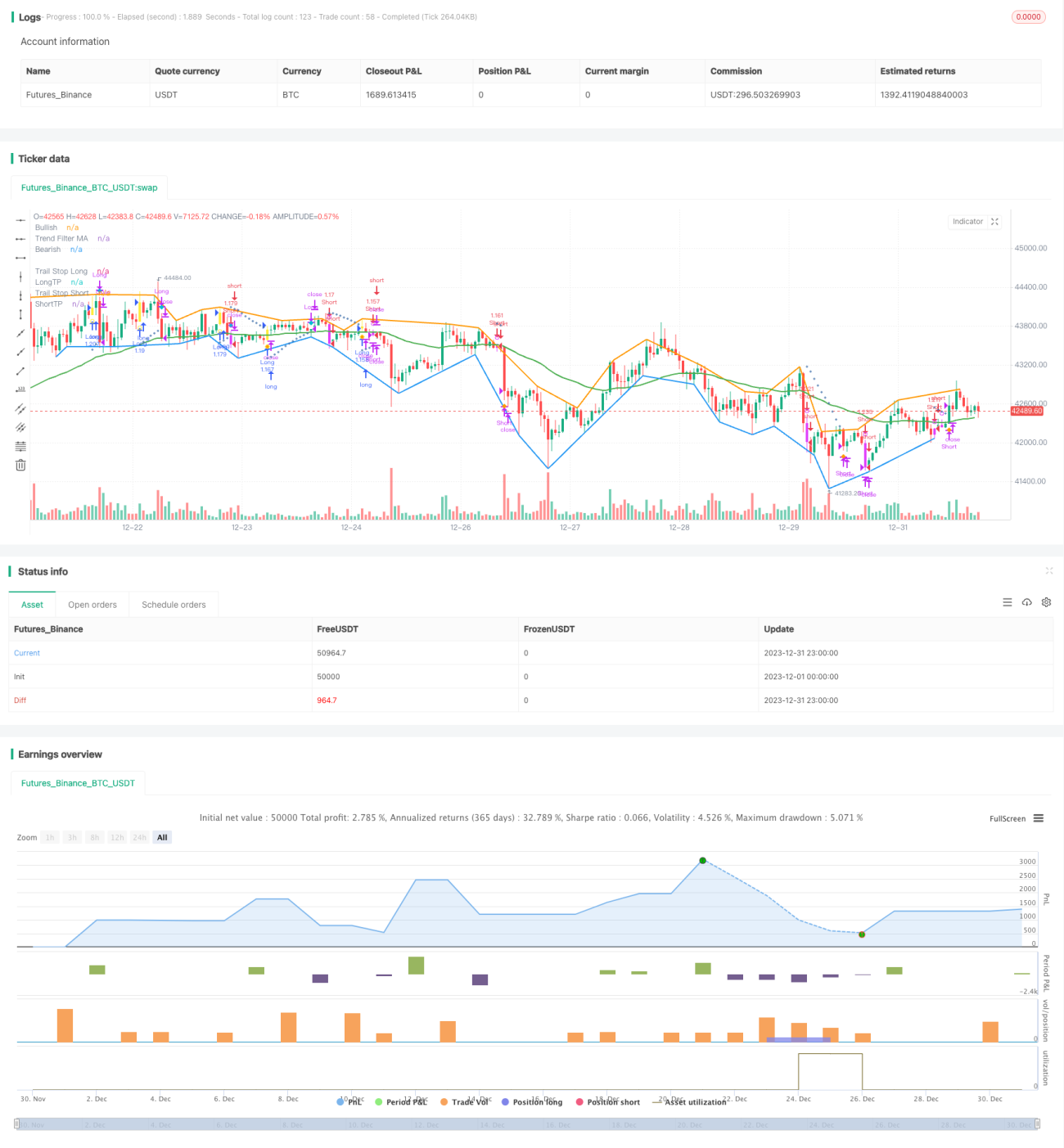

Handelsstrategie mit MACD-Indikator über mehrere Zeitperioden

Übersicht

Diese Strategie basiert auf dem klassischen MACD-Indikator und kombiniert mehrere Hilfsindikatoren wie Trendbewertung, Stop-Loss- und Take-Profit-Methoden, um ein relativ vollständiges Trendfolge-Handelssystem zu bilden. Sie kann sowohl für Kryptowährungen als auch für Devisen- und Aktienhandel eingesetzt werden.

Strategieprinzip

-

MACD-Indikatorbewertung

- Die Differenz zwischen dem FASTLENGTH-EMA und dem SLOWLENGTH-EMA bildet den MACD-Histogramm

- Der MACDLENGTH-EMA glättet das MACD-Histogramm zur MACD-Linie

- Ein Durchbruch des MACD-Histogramms über die Nulllinie erzeugt Kauf-/Verkaufssignale

-

Trendbewertung

- ADX: Durchschnittlicher Trendindikator, bewertet das Vorhandensein eines Trends

- MA: Gleitender Durchschnitt, der Preis über/unter dem MA zeigt den Trend an

- SAR: Parabolischer SAR, die Bewegung des SAR über/unter dem Preis zeigt den Trend an

-

Stop-Loss-Methoden

- ATR-Prozentsatz-Stop-Loss: Festlegung eines prozentualen Stops basierend auf dem ATR-Faktor

- SAR-Stop-Loss: Parabolischer SAR als Stop nach dem Einstieg

-

Take-Profit-Methoden

- ATR-fester Take-Profit-Abstand: Festlegung eines festen Take-Profit-Abstands basierend auf dem ATR-Faktor

- Prozentualer Take-Profit: Festlegung eines prozentualen Take-Profit-Abstands

-

Zeitbasierter Stop-Loss

- Möglichkeit, nach einer bestimmten Anzahl von Kerzen einen Stop-Loss zu setzen

Vorteilsanalyse

-

Mehrere Hilfsbewertungen

- Kombination von Trend-, Unterstützungs- und Widerstandsbewertungen reduziert Fehlsignale

- ATR/SAR-Stop-Loss für umfassendere Risikokontrolle

-

Flexible Konfiguration

- Auswahl, ob Trendfilter verwendet werden soll

- Wahl zwischen ATR- oder SAR-Stop-Loss

- Wahl zwischen ATR- oder Standard-Take-Profit

- Parameter flexibel einstellbar

-

Bereitstellung von Divergenzanalysen

- Anzeige historischer positiver und negativer Divergenzen

- Textuelle Hinweise

-

Einfache Optimierung und Anpassung

- Strategie enthält viele konfigurierbare Parameter

- Einfaches Testen verschiedener Variablenkombinationen

Risikoanalyse

-

Ungünstige Parametereinstellungen können Verluste vergrößern

- Falsche Einstellung von ATR/SAR-Parametern kann zu vorzeitigem Stop-Loss führen

- Zu großer Take-Profit-Prozentsatz kann zu vorzeitigem Take-Profit führen

-

Risiko des Trendbewertungsversagens

- Falsche Parameter für Trendindikatoren können zu Fehlbewertungen führen

- Unerwartete Ereignisse beeinträchtigen die Trendbewertung

-

Risiko des zeitbasierten Stop-Loss

- Festlegung eines festen zeitbasierten Stop-Loss birgt Verlustrisiko

Optimierungsmöglichkeiten

- Anpassung der ATR/SAR-Parameter für einen glatteren Stop-Loss

- Testen verschiedener MA-Perioden zur Optimierung der Trendbewertung

- Testen und Anpassen des Take-Profit-Prozentsatzes zur Optimierung der Rendite

- Kombination mit Volatilitätsindikatoren zur Parameteroptimierung

Zusammenfassung

Diese Strategie berücksichtigt mehrere Aspekte wie Trendbewertung, Stop-Loss/Take-Profit und Divergenzerkennung und bildet ein relativ umfassendes Handelssystem für Kryptowährungen. Sie kombiniert die Stärken des MACD-Indikators, fügt einen Trendfilter hinzu, um Fehlhandel zu vermeiden, und integriert ATR/SAR-Stop-Loss für eine bessere Risikokontrolle. Die Divergenzerkennung bietet zusätzliche Referenzpunkte. Dank zahlreicher konfigurierbarer Parameter kann die Strategie einfach getestet und optimiert werden. Insgesamt kann diese Strategie als gutes Beispiel für die Erforschung von Kryptowährungsstrategien dienen.

- 1