Adaptive SuperTrend-KI-Strategie

SUPERTREND, ATR, ADX, EMA, AI

Dies ist nicht die gewöhnliche SuperTrend-Strategie, die Sie kennen

Der größte Schmerzpunkt der traditionellen SuperTrend-Strategie? Feste Parameter zeigen in unterschiedlichen Marktumgebungen extrem unterschiedliche Leistungen. Diese KI-verbesserte Version passt den ATR-Multiplikator dynamisch an: In Phasen hoher Volatilität wird der Multiplikator auf das 2-fache des Basiswerts erhöht, in Phasen niedriger Volatilität auf das 0,85-fache reduziert. Backtest-Daten zeigen, dass dieser adaptive Mechanismus Fehlsignale in Seitwärtsmärkten signifikant reduzieren kann.

Die Kerninnovation liegt in einem dreistufigen Filtersystem: Marktzustandserkennung, KI-Signalbewertung und mehrfache Bestätigungsmechanismen. Es wird nicht mehr einfach bei einem Preisbruch der SuperTrend-Linie eingestiegen, sondern erst wenn die KI-Bewertung mindestens 65 Punkte erreicht, wird ein Handelssignal ausgelöst. Dieses Bewertungssystem berücksichtigt fünf Dimensionen: Volumenspitzen, Grad der Preisabweichung, Trendkonsistenz usw.

KI-Bewertungssystem: Quantifizierung der Zuverlässigkeit jedes Signals

Das Bewertungssystem ist raffiniert konzipiert: Volumenspitze 20 Punkte, Abstand der Preisabweichung zur SuperTrend-Linie 25 Punkte, EMA-Trendkonsistenz 20 Punkte, Marktzustandsqualität 15 Punkte, vorherige Entfernung des Preises zur Trendlinie 20 Punkte. Gesamtpunktzahl 100, die standardmäßige Schwelle von 65 Punkten bedeutet, dass nur hochwertige Signale den Filter passieren.

Konkret: Wenn das Volumen das 2,5-fache des 20-Perioden-Durchschnitts übersteigt, gibt es die vollen 20 Punkte; wenn die Preisabweichung mehr als das 1,5-fache des ATR von der SuperTrend-Linie beträgt, die vollen 25 Punkte. Diese quantitative Bewertung vermeidet subjektive Urteile – jedes Signal basiert auf klaren Daten. In der Praxis empfiehlt es sich, die Mindestpunktzahl je nach Eigenschaften des Instruments anzupassen.

Marktzustandsadaptive Anpassung: Schluss mit Einheitsparametern

Die Strategie erkennt drei Marktzustände anhand des ATR-Verhältnisses und des ADX-Indikators: Trendphase (regime=1), Hochvolatilitätsphase (regime=2), Seitwärtsphase (regime=0). Wenn das ATR-Verhältnis 1,4 übersteigt, wird es als Hochvolatilitätsphase eingestuft; wenn der ADX unter 20 liegt und das ATR-Verhältnis unter 0,9, als Seitwärtsphase.

Logik der adaptiven Multiplikatoranpassung: In der Hochvolatilitätsphase wird der Multiplikator um 40% × (ATR-Verhältnis - 1,0) erhöht, in der Seitwärtsphase auf 85% des Basiswerts reduziert. Das bedeutet, dass ein Basis-Multiplikator von 3,0 bei extremer Volatilität auf 4,2 angepasst werden kann, in der Seitwärtsphase auf 2,55. Dieser dynamische Anpassungsmechanismus verbessert die Anpassungsfähigkeit der Strategie in verschiedenen Marktumgebungen erheblich.

Risikomanagement: Drei Stop-Modi zur Auswahl

Der dynamische ATR-Stop ist die erste Wahl – der Standardabstand von 2,5 ATR toleriert normale Schwankungen und stoppt rechtzeitig. Der prozentuale Stop eignet sich für Instrumente mit relativ stabiler Volatilität, während der SuperTrend-Modus bei Trendumkehr sofort schließt.

Take-Profit unterstützt das Risiko-Ertrags-Verhältnis, standardmäßig 2,5:1 – statistisch vorteilhaft. Bei aktiviertem Trailing-Stop wird die Stop-Linie für profitable Positionen dynamisch basierend auf dem 2,5-fachen ATR-Abstand angepasst, um Gewinne in Trendmärkten zu maximieren.

Mehrfachfilter: Reduzierung ineffektiver Trades

Der EMA-Trendfilter stellt sicher, dass nur bei Übereinstimmung mit der 50-Perioden-EMA-Richtung eingestiegen wird, wodurch gegenläufige Trades vermieden werden. Der Seitwärtsphasenfilter überspringt direkt Signale mit regime=0 – obwohl dadurch möglicherweise Gelegenheiten verpasst werden, sinkt die Fehlsignalrate deutlich.

Der Volumenfilter erfordert ein Volumen über dem 20-Perioden-Durchschnitt zum Einstiegszeitpunkt, um ausreichende Marktbeteiligung für den Preisbruch sicherzustellen. Eine Abkühlungsphase von 10 Perioden verhindert häufige Trades und senkt die Handelskosten.

Praxis-Tipps: Parameteroptimierung und Risikokontrolle

Für Kryptowährungen wird empfohlen, die Mindest-KI-Bewertung auf 70 Punkte anzuheben, für traditionelle Aktien kann sie auf 60 Punkte gesenkt werden. Hochfrequenzhändler können die Abkühlungsphase auf 5 Perioden verkürzen, langfristige Anleger sollten sie auf 15 Perioden verlängern.

Der ATR-Längenparameter 10 ist ein optimierter Kompromiss – zu kurz macht zu empfindlich, zu lang führt zu Verzögerungen. Der Basismultiplikator 3,0 eignet sich für die meisten Instrumente – bei hochvolatilen Instrumenten kann er auf 3,5 erhöht, bei niedrigvolatilen auf 2,5 reduziert werden.

Wichtiger Risikohinweis: Historische Backtest-Ergebnisse garantieren keine zukünftige Performance. Die Strategie kann unter extremen Marktbedingungen zu Verlustserien führen. Es wird empfohlen, die Positionsgröße pro Trade streng auf maximal 30% des Gesamtkapitals zu begrenzen. Die Leistung der Strategie variiert erheblich je nach Marktumgebung; eine fortlaufende Überwachung und Parameteranpassung ist erforderlich.

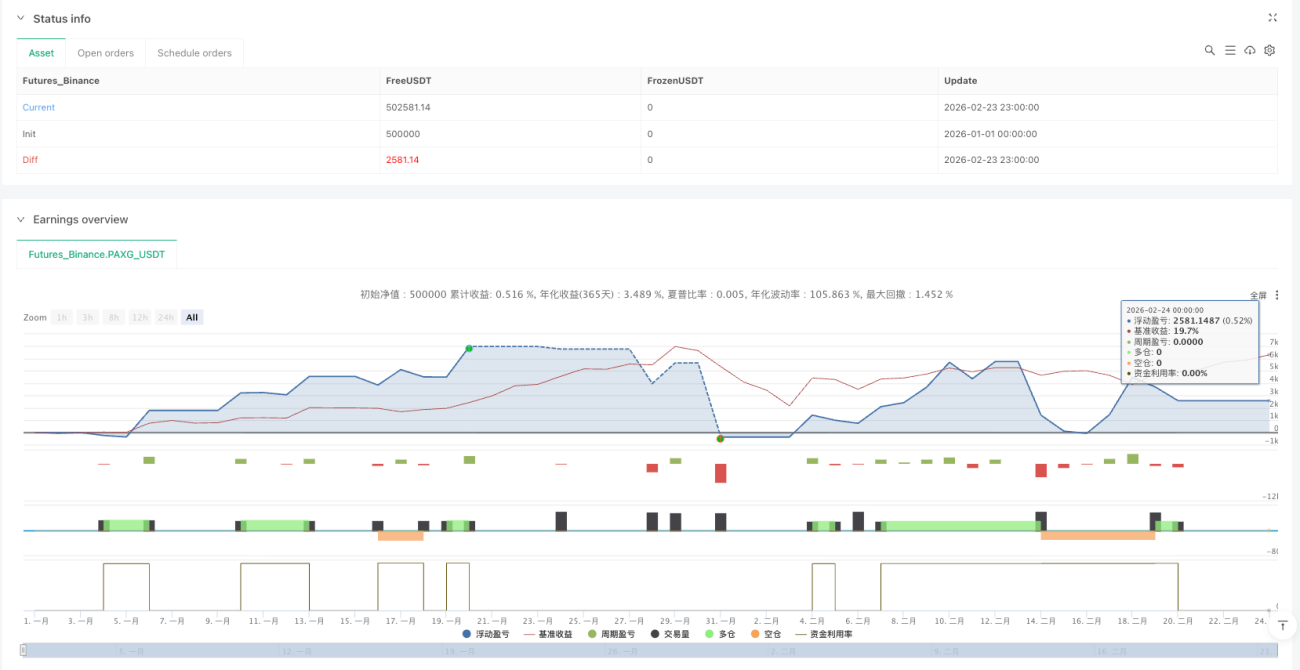

/*backtest

start: 2026-01-01 00:00:00

end: 2026-02-24 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"PAXG_USDT","balance":500000}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © DefinedEdge

//@version=6- 1