The net of easy and bad contracts

Author: The Noble, Date: 2021-11-18 17:28:35Tags:

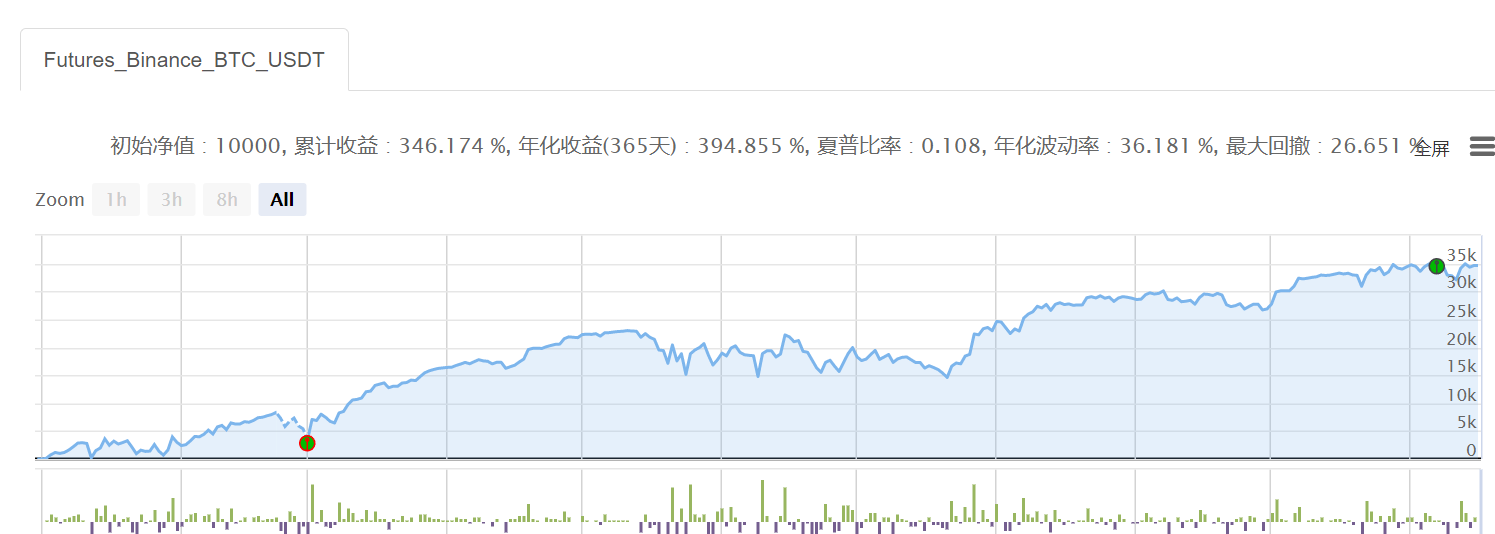

The parameters are very simple, take BTC as an example, to the area with a lot of flat open, to the area with a lot of open, to the area with a lot of flat open, and back again.

Obviously, in monetary circles, in the long run, any complex model can't run on a brainless grid.

The code for wealth is brainless grid + brainless hound

Hopefully, like the first Martin, it's the simplest, roughest, but most profitable strategy.

'''backtest

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

- The balance strategy of the bearish bullish U

- Multiple ATR strategies for digital currency futures (teachings)

- Transfer USDT from a contract account to a cash/currency account (OKEX, Binance support simultaneously)

- Binance trading terminal funds scraping tool

- All orders in the account are displayed (U-bits)

- Binance manually opens the clearing instrument

- Directly retrieve Binance K-string data with HttpQuery

- Digital currency cash multi-variety two-way strategy (teaching)

- Summary of the capital rates of the major exchanges

- Digital currency futures with double-equal turning point strategies (Teaching)

- Current Index Balance Strategy v1.1 ((It's been running for a while, now it seems there's a bug, because it doesn't work, it needs to be fixed))

- Get the full name of the USDT contract

- Binance websocket subscribes to the permanent contract market information

- The new currency is going up.

- Some people turn to the reverse when the stock explodes.

- Automatically accesses Binance futures trading accuracy & minimum open positions (which have been abandoned)

- One-bond market for a permanent contract

- Strategy of the current balance - 0.0.1v

- Binance contract grid - 0.0.2v

- Index hedge (short field) 0.0.1

mexminThere is a problem with the for loop syntax

Light cloudsPlease tell me, the real disk error suggests Traceback (most recent call last): File "

Light cloudsI'm a huge fan of JS, and I'd love to write one with JS.

Light cloudsGood. Thank you.

The NobleSo let's say that we have an array of positions, and let's look at the array structure.