High Volume Low Breakout Compounded Position Sizing Strategy

Overview

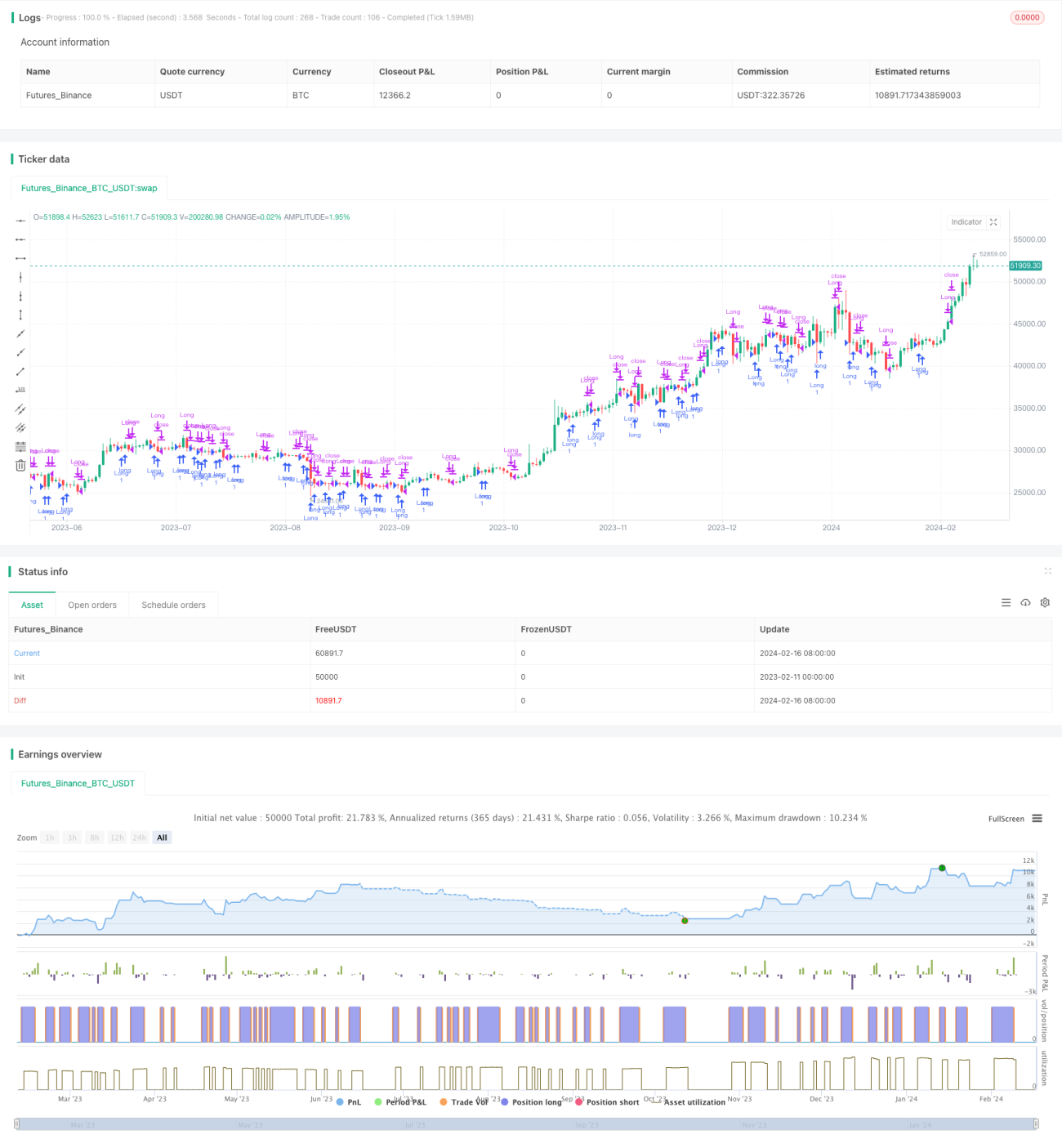

The core idea of this strategy is to track breakouts during high trading volume by using a compounded position sizing approach based on a defined risk percentage and 250x simulated leverage. It aims to capture potential reversal opportunities after heavy selling pressure.

Strategy Logic

Long entry signals are triggered when:

- Volume exceeds a user-defined threshold (volThreshold)

- The current bar's low is lower than the previous bar's low (lowLowerThanPrevBar)

- The current bar's close is negative but higher than the previous bar's close (negativeCloseWithHighVolume)

- There is no existing open long position (strategy.position_size == 0)

Position sizing is calculated as:

- Risk amount based on equity * risk percentage

- Risk amount * leverage (250x) to determine number of contracts/lots

Exit rules:

Close long position when profit percentage posProfitPct hits stop loss (-0.14%) or take profit (4.55%).

Advantage Analysis

Advantages of this strategy:

- Captures trend reversal opportunities from high trading volume

- Compounded position sizing allows for faster profit growth

- Reasonable stop loss and take profit helps control risk

Risk Analysis

Risks to consider:

- 250x leverage amplifies losses

- Does not account for slippage, commissions, margin requirements

- Requires robust backtesting and parameter optimization

Risk can be reduced by:

- Lowering leverage amount

- Increasing stop loss percentage

- Accounting for real-world trading costs

Optimization Opportunities

Areas for improvement:

- Dynamically adjust leverage level

- Optimize stop loss and take profit rules

- Add trend filter

- Customize parameters based on instrument

Conclusion

In summary, this is a fairly simple and straightforward strategy for capturing reversals and outsized gains. But risks exist and prudent real-world testing is essential. With optimization, it can be made more robust and practical.

/*backtest

start: 2023-02-11 00:00:00

end: 2024-02-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Volume Low Breakout (Compounded Position Size)", overlay=true, initial_capital=1000)

// Define input for volume threshold- 1