Multi-factor Quantitative Trading Strategy

Overview

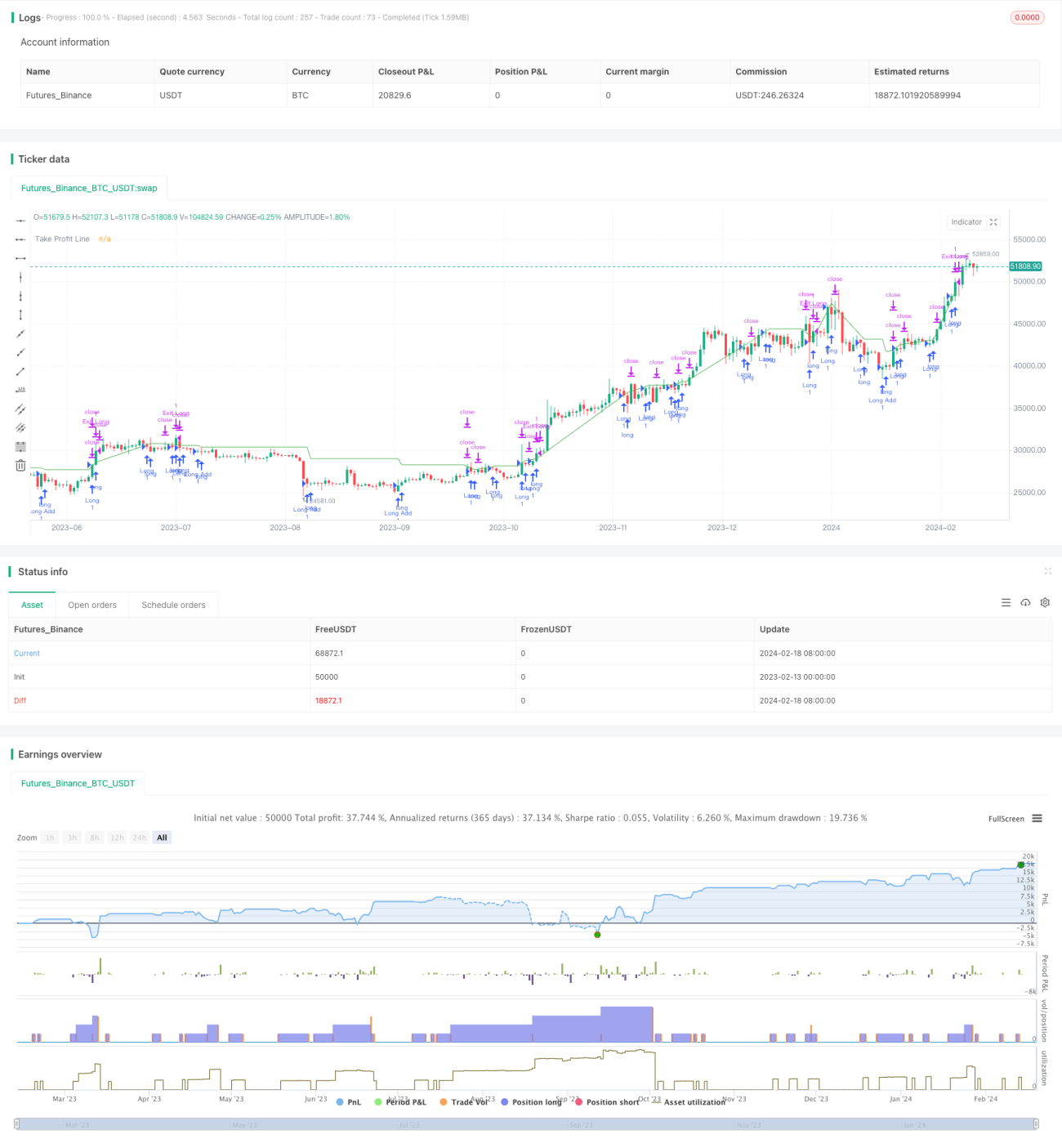

This strategy combines multiple technical indicators such as RSI, MACD, OBV, CCI, CMF, MFI and VWMACD to detect divergences between price and volume to identify potential entry opportunities. The strategy also incorporates user dip detection indicators to generate trading signals when high volatility and depth or VFI conditions are met. The strategy only goes long and uses tracking stop loss to gradually accumulate positions.

Strategy Logic

-

Calculate indicators like RSI, MACD, OBV, CCI, CMF, MFI and VWMACD, and detect divergences between the indicators and historical prices using an adaptive linear regression method. Generate buy signals when an indicator makes a new low while the price does not.

-

Based on user input volatility threshold and depth percentage threshold, combined with VFI indicator filtering, generate signals on candlesticks that meet high volatility and depth tests.

-

After initial long entry, if the price breaks the last long entry price by a configured percentage, add another long position.

-

Use tracking stop loss to close positions when reaching configured take profit ratio.

Advantage Analysis

-

Multi-factor combination makes comprehensive use of price and volume indicators to improve signal reliability.

-

Adaptive linear regression method detects divergences and avoids subjectivity of manual judgment.

-

Incorporating volatility, depth/VFI indicators helps discover reversal opportunities.

-

Multi-entry accumulation allows full use of pullbacks, and tracking stop profit helps lock in profits.

Risk Analysis

-

Complex multi-factor judgment may affect actual performance depending on parameter optimization and divergence detection effectiveness.

-

Unidirectional holding has higher risk, large losses may occur if judgment is wrong.

-

Loss may be amplified in repeated adding model, position size needs to be carefully controlled.

-

Pay attention to impact of trading fees on actual profit.

Optimization Directions

-

Test combinations of different parameters and indicators to select optimal configuration.

-

Add stop loss strategies to control per trade and maximum losses.

-

Consider opportunities in both directions to diversify risks.

-

Incorporate machine learning methods to automatically optimize parameters.

Summary

This strategy identifies entry timing through a combination of technical indicators, and uses user defined conditions and VFI filtering to eliminate false signals. It takes advantage of pullbacks to accumulate positions chasing the trend, which helps capture opportunities in trends. But it also faces risks of wrong judgment and unidirectional holding. Appropriate optimization on indicator parameters, stop loss strategies etc. is needed to reduce risks and expand profit space.

- 1