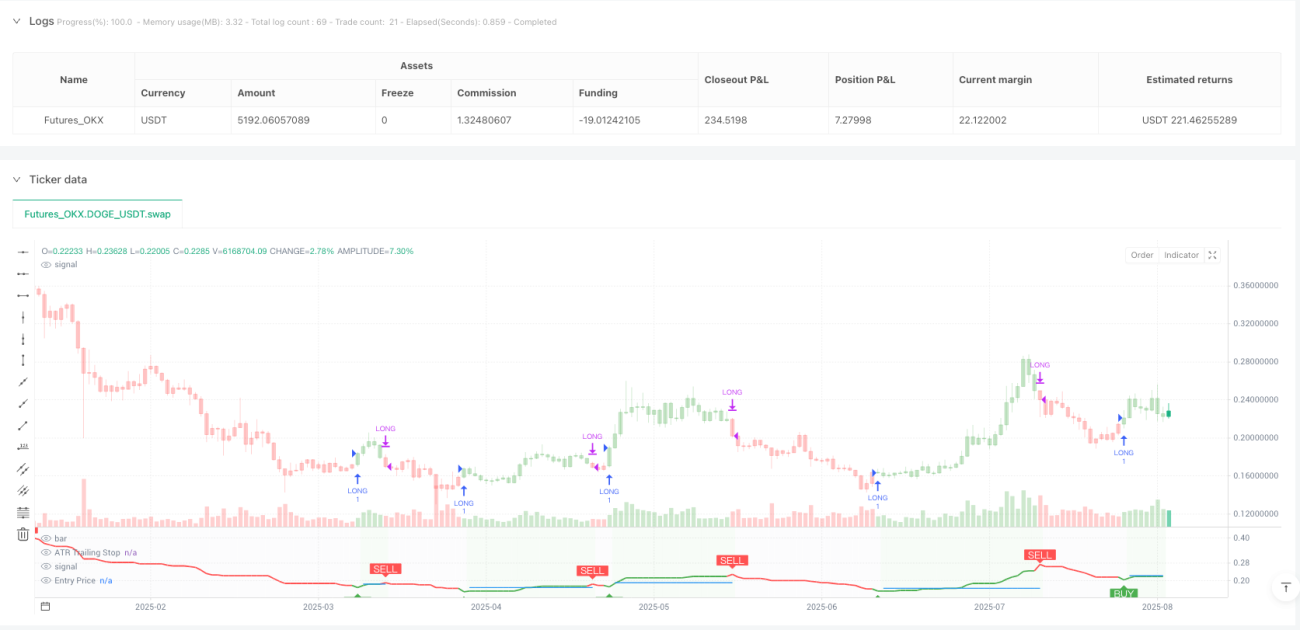

Volatility-Adaptive Heikin Ashi ATR Trailing Stop Trend Trading Strategy

Overview

The Volatility-Adaptive Heikin Ashi ATR Trailing Stop Trend Trading Strategy is a systematic trading approach designed for trend identification and risk management in financial markets. The strategy is based on Heikin Ashi candlestick technique to filter market noise, combined with an Average True Range (ATR) dynamically adjusted trailing stop system, using Exponential Moving Average (EMA) crossovers to generate trading signals. The strategy executes long-only positions and enhances signal robustness and trade management through volatility-adjusted components. This strategy is particularly suitable for highly volatile markets such as cryptocurrencies, as well as for traders pursuing systematic trend following.

Strategy Principles

The core principles of this strategy rely on the synergistic action of several key technical components:

-

Heikin Ashi Candlestick Filtering: The strategy offers three different Heikin Ashi calculation modes (manual calculation, TradingView built-in function, and regular candlesticks) to mitigate short-term market noise and highlight underlying trend direction. The manual calculation mode provides the most transparent and reliable results, while the built-in function uses confirmed historical bars to prevent repainting.

-

ATR Trailing Stop Mechanism: Average True Range (ATR) serves as a dynamic measure of market volatility, combined with user-defined parameters (Key Value and ATR Period) to calibrate the trailing stop sensitivity, allowing it to adapt to different market volatility regimes. This mechanism aims to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

-

EMA Crossover Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi price and an Exponential Moving Average (EMA). A crossover event between these two components is used to objectively identify momentum shifts, signaling potential long entry or exit points.

-

Rigorous Stop Loss Implementation: The strategy includes an optional stop loss feature, configurable as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not synthetic Heikin Ashi values, ensuring that risk management is grounded in actual market liquidity and price levels.

-

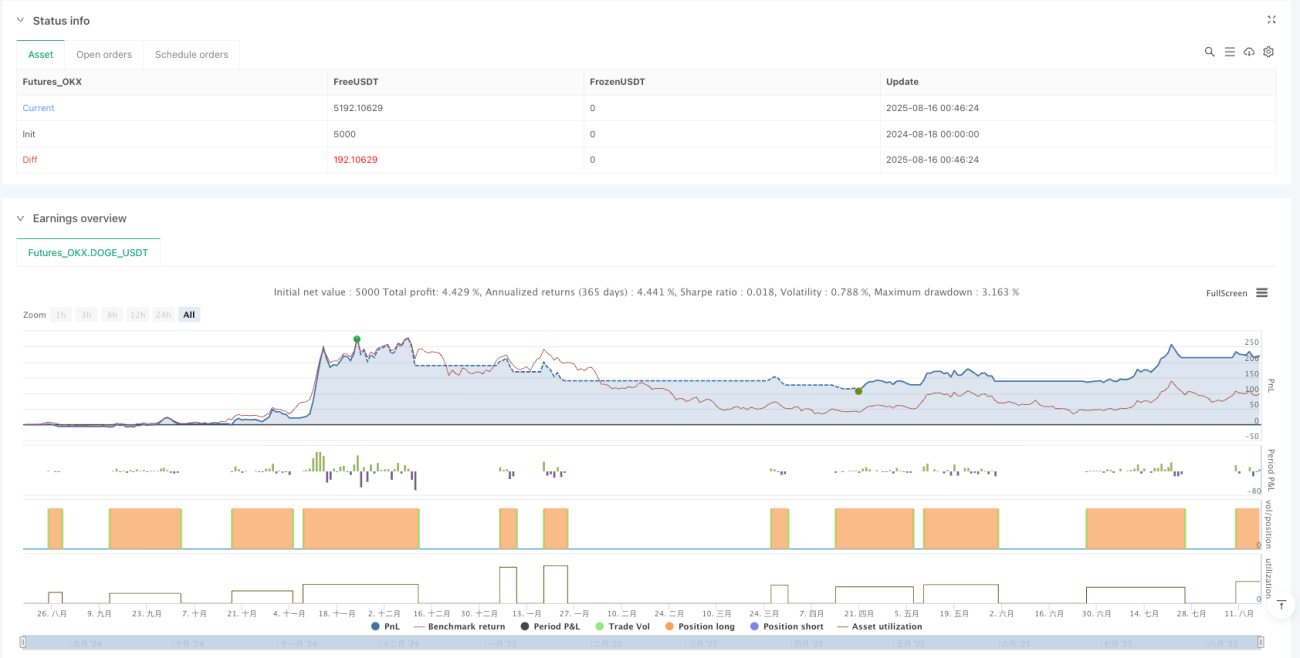

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices, and includes a configurable Date Filter to define specific historical periods for performance evaluation.

-

Data Visualization: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level, as well as an integrated information table displaying real-time strategy parameters, current position status, trend direction, and key price levels.

Strategy Advantages

-

Noise Filtering Capability: The Heikin Ashi candlestick technique effectively filters short-term market noise, helping traders focus on more significant market trends and reducing interference from false signals.

-

Dynamic Risk Management: The ATR-based trailing stop mechanism automatically adjusts according to market volatility, providing wider stops during increased volatility and tighter protection when volatility subsides, optimizing the risk-reward ratio.

-

Objective Entry and Exit Signals: Signals generated through EMA crossovers eliminate subjective judgment, making trading decisions more systematic and repeatable, contributing to emotional discipline.

-

Real Market Price Execution: The strategy uses real market prices (rather than Heikin Ashi synthetic prices) for trade execution and stop losses in backtesting, providing more accurate backtesting results that are closer to actual trading environments.

-

Visual Feedback and Monitoring: The integrated information table and visual indicators provide real-time strategy status and key data points, facilitating quick assessment and monitoring, enhancing decision-making capabilities.

-

Flexible Parameter Configuration: Adjustable key parameters (sensitivity value, ATR period, Heikin Ashi method, and stop loss settings) allow the strategy to adapt to different market environments and trader risk preferences.

-

Long-Only Strategy Design: Focusing on capturing upward trends avoids potential short squeeze risks, particularly suitable for markets with a long-term bullish bias, such as certain cryptocurrencies.

Strategy Risks

-

Trend Reversal Risk: As a trend-following strategy, it may face significant drawdowns during sideways markets or rapid reversals, and the ATR trailing stop may not fully prevent such losses.

-

Parameter Optimization Trap: Excessive optimization of parameters may lead to curve fitting, causing the strategy to perform excellently on historical data but poorly in future markets. Testing across multiple markets and timeframes is recommended to ensure robustness.

-

Entry Timing Risk: EMA crossover signals may occur at a relatively late stage of trend development, resulting in less-than-ideal entry positions. In strong markets, this may lead to buying at high levels.

-

Stop Loss Trigger Risk: In highly volatile markets, prices may briefly touch stop loss levels even during an overall favorable trend, causing unnecessary exits. Stop loss parameters need to be carefully set according to market characteristics.

-

Single Technical Indicator Dependency: The strategy primarily relies on ATR and EMA indicators without considering fundamental factors or other technical indicators, potentially missing important market turning points.

-

Performance in Extended Sideways Markets: In long-term sideways markets, the strategy may generate multiple false signals, resulting in accumulated small losses. It is advisable to use it when the market is confirmed to be in a trending state.

-

Slippage and Execution Risk: Although the strategy considers slippage in backtesting, actual slippage and execution delays in real trading may be greater than the set values, especially in less liquid markets.

Strategy Optimization Directions

-

Multi-Timeframe Analysis Integration: Consider integrating trend confirmation signals from higher timeframes, executing trades only when the trend direction on higher timeframes is consistent, which can significantly improve win rates and risk-reward ratios.

-

Volatility Filter: Adding a volatility-based filter to pause trading or adjust position sizes during abnormally high volatility periods can reduce risks associated with extreme market fluctuations.

-

Dynamic Position Management: Implementing dynamic position sizing based on volatility and market conditions, rather than fixed percentage allocations, can optimize capital efficiency across different market conditions.

-

Multi-Indicator Confirmation: Integrating other complementary technical indicators (such as Relative Strength Index RSI, Stochastic, or MACD) as secondary confirmations can reduce false signal rates and improve trade quality.

-

Stop Loss Strategy Improvement: Implementing more sophisticated stop loss strategies, such as multiples of ATR or support/resistance level-based stops, rather than simple percentages or fixed points, can better adapt to market structure.

-

Exit Strategy Refinement: Developing more refined partial profit-taking and staged exit mechanisms can lock in partial profits while maintaining trend exposure, optimizing the overall return curve.

-

Market Regime Recognition: Adding market regime recognition algorithms to automatically adjust strategy parameters for different market states (trending, oscillating, or reversing) enhances the strategy's adaptive capabilities.

-

Machine Learning Integration: Exploring machine learning techniques to optimize parameter selection or predict optimal entry/exit points can further enhance strategy performance and reduce subjective intervention.

Summary

The Volatility-Adaptive Heikin Ashi ATR Trailing Stop Trend Trading Strategy is a well-designed, risk-controlled trend following system particularly suitable for markets with higher volatility. By combining the noise filtering capability of Heikin Ashi candlesticks, the dynamic risk management of ATR, and the trend identification functionality of EMA, the strategy provides an objective, systematic trading framework.

The strategy's main strengths lie in its adaptability and dynamic risk management capability, automatically adjusting stop loss levels according to market volatility conditions, protecting capital and locking in profits. Meanwhile, its rigorous stop loss implementation and execution mechanism based on real market prices ensure the reliability and reproducibility of backtesting results.

However, as a trend-following strategy, it may face challenges during sideways markets or rapid reversals. Through integrating multi-timeframe analysis, adding volatility filters, optimizing position management, and refining exit strategies, the strategy's robustness and performance can be further enhanced.

For traders looking to build systematic trading methods, this strategy provides a solid foundation that can be customized and expanded according to individual risk preferences and market characteristics, with the potential to achieve stable risk-adjusted returns across various market environments.

- 1