Utilice la interfaz de mercado agregada de la plataforma de criptomonedas para construir una estrategia de símbolos múltiples

El autor:No lo sé., Creado: 2022-04-24 17:34:03, Actualizado:Utilice la interfaz de mercado agregada de la plataforma de criptomonedas para construir una estrategia de símbolos múltiples

En la sección [

Tomemos Binance y Huobi como ejemplo; si revisas su documentación de API, encontrarás que hay interfaces agregadas:

Interfaz de mercado

-

Contrato de Binance:https://fapi.binance.com/fapi/v1/ticker/bookTickerLos datos devueltos por la interfaz:

[ { "symbol": "BTCUSDT", // trading pair "bidPrice": "4.00000000", //optimum bid price "bidQty": "431.00000000", //bid quantity "askPrice": "4.00000200", //optimum ask price "askQty": "9.00000000", //ask quantity "time": 1589437530011 // matching engine time } ... ] -

El sitio de Huobi:https://api.huobi.pro/market/tickersLos datos devueltos por la interfaz:

[ { "open":0.044297, // open price "close":0.042178, // close price "low":0.040110, // the lowest price "high":0.045255, // the highest price "amount":12880.8510, "count":12838, "vol":563.0388715740, "symbol":"ethbtc", "bid":0.007545, "bidSize":0.008, "ask":0.008088, "askSize":0.009 }, ... ]Sin embargo, el resultado en realidad no es así, y la estructura real devuelta por la interfaz Huobi es:

{ "status": "ok", "ts": 1616032188422, "data": [{ "symbol": "hbcbtc", "open": 0.00024813, "high": 0.00024927, "low": 0.00022871, "close": 0.00023495, "amount": 2124.32, "vol": 0.517656218, "count": 1715, "bid": 0.00023427, "bidSize": 2.3, "ask": 0.00023665, "askSize": 2.93 }, ...] }Debe prestarse atención al procesar los datos devueltos por la interfaz.

Construir la estructura del programa de la estrategia

¿Cómo encapsular las dos interfaces en la estrategia, y cómo procesar los datos? Vamos a echar un vistazo.

Primero, escribir un constructor, para construir objetos de control

// parameter e is used to import the exchange object; parameter subscribeList is the trading pair list to be processed, such as ["BTCUSDT", "ETHUSDT", "EOSUSDT", "LTCUSDT", "ETCUSDT", "XRPUSDT"]

function createManager(e, subscribeList) {

var self = {}

self.supportList = ["Futures_Binance", "Huobi"] // the supported platform's

// object attribute

self.e = e

self.name = e.GetName()

self.type = self.name.includes("Futures_") ? "Futures" : "Spot"

self.label = e.GetLabel()

self.quoteCurrency = ""

self.subscribeList = subscribeList // subscribeList : [strSymbol1, strSymbol2, ...]

self.tickers = [] // all market data obtained by the interfaces; define the data format as: {bid1: 123, ask1: 123, symbol: "xxx"}}

self.subscribeTickers = [] // the market data needed; define the data format as: {bid1: 123, ask1: 123, symbol: "xxx"}}

self.accData = null // used to record the account asset data

// initialization function

self.init = function() {

// judge whether a platform is supported

if (!_.contains(self.supportList, self.name)) {

throw "not support"

}

}

// judge the data precision

self.judgePrecision = function (p) {

var arr = p.toString().split(".")

if (arr.length != 2) {

if (arr.length == 1) {

return 0

}

throw "judgePrecision error, p:" + String(p)

}

return arr[1].length

}

// update assets

self.updateAcc = function(callBackFuncGetAcc) {

var ret = callBackFuncGetAcc(self)

if (!ret) {

return false

}

self.accData = ret

return true

}

// update market data

self.updateTicker = function(url, callBackFuncGetArr, callBackFuncGetTicker) {

var tickers = []

var subscribeTickers = []

var ret = self.httpQuery(url)

if (!ret) {

return false

}

try {

_.each(callBackFuncGetArr(ret), function(ele) {

var ticker = callBackFuncGetTicker(ele)

tickers.push(ticker)

for (var i = 0 ; i < self.subscribeList.length ; i++) {

if (self.subscribeList[i] == ele.symbol) {

subscribeTickers.push(ticker)

}

}

})

} catch(err) {

Log("error:", err)

return false

}

self.tickers = tickers

self.subscribeTickers = subscribeTickers

return true

}

self.httpQuery = function(url) {

var ret = null

try {

var retHttpQuery = HttpQuery(url)

ret = JSON.parse(retHttpQuery)

} catch (err) {

// Log("error:", err)

ret = null

}

return ret

}

self.returnTickersTbl = function() {

var tickersTbl = {

type : "table",

title : "tickers",

cols : ["symbol", "ask1", "bid1"],

rows : []

}

_.each(self.subscribeTickers, function(ticker) {

tickersTbl.rows.push([ticker.symbol, ticker.ask1, ticker.bid1])

})

return tickersTbl

}

// initialization

self.init()

return self

}

Utilice la función de la API FMZHttpQueryPara enviar una solicitud de acceso a la interfaz de la plataforma.HttpQuery, usted necesita utilizar el procesamiento de excepcionestry...catchpara manejar excepciones como el fallo de retorno de la interfaz.

Algunos estudiantes aquí pueden preguntar: bidPriceen Binance, perobiden Huobi.

Usamos la función de devolución aquí y separar estas partes que necesitan un procesamiento especializado de forma independiente.

Así que después de que el objeto anterior se inicializa, se convierte en esto en el uso específico:

(El siguiente código omite el constructorcreateManager(en inglés)

los contratos supervisados por Binance Futures:["BTCUSDT", "ETHUSDT", "EOSUSDT", "LTCUSDT", "ETCUSDT", "XRPUSDT"]los pares de operaciones al contado supervisados por Huobi Spot:["btcusdt", "ethusdt", "eosusdt", "etcusdt", "ltcusdt", "xrpusdt"]

function main() {

var manager1 = createManager(exchanges[0], ["BTCUSDT", "ETHUSDT", "EOSUSDT", "LTCUSDT", "ETCUSDT", "XRPUSDT"])

var manager2 = createManager(exchanges[1], ["btcusdt", "ethusdt", "eosusdt", "etcusdt", "ltcusdt", "xrpusdt"])

while (true) {

// update market data

var ticker1GetSucc = manager1.updateTicker("https://fapi.binance.com/fapi/v1/ticker/bookTicker",

function(data) {return data},

function (ele) {return {bid1: ele.bidPrice, ask1: ele.askPrice, symbol: ele.symbol}})

var ticker2GetSucc = manager2.updateTicker("https://api.huobi.pro/market/tickers",

function(data) {return data.data},

function(ele) {return {bid1: ele.bid, ask1: ele.ask, symbol: ele.symbol}})

if (!ticker1GetSucc || !ticker2GetSucc) {

Sleep(1000)

continue

}

var tbl1 = {

type : "table",

title : "futures market data",

cols : ["futures contract", "futures buy1", "futures sell1"],

rows : []

}

_.each(manager1.subscribeTickers, function(ticker) {

tbl1.rows.push([ticker.symbol, ticker.bid1, ticker.ask1])

})

var tbl2 = {

type : "table",

title : "spot market data",

cols : ["spot contract", "spot buy1", "spot sell1"],

rows : []

}

_.each(manager2.subscribeTickers, function(ticker) {

tbl2.rows.push([ticker.symbol, ticker.bid1, ticker.ask1])

})

LogStatus(_D(), "\n`" + JSON.stringify(tbl1) + "`", "\n`" + JSON.stringify(tbl2) + "`")

Sleep(10000)

}

}

Prueba de funcionamiento:

Añadir Binance Futures como el primer objeto de intercambio, y añadir Huobi Spot como el segundo objeto de intercambio.

Como pueden ver, aquí la función de devolución de llamada se invoca para hacer un procesamiento especializado en operaciones en diferentes plataformas, como cómo obtener los datos devueltos por interfaz.

var ticker1GetSucc = manager1.updateTicker("https://fapi.binance.com/fapi/v1/ticker/bookTicker",

function(data) {return data},

function (ele) {return {bid1: ele.bidPrice, ask1: ele.askPrice, symbol: ele.symbol}})

var ticker2GetSucc = manager2.updateTicker("https://api.huobi.pro/market/tickers",

function(data) {return data.data},

function(ele) {return {bid1: ele.bid, ask1: ele.ask, symbol: ele.symbol}})

Después de diseñar el método de obtención de los datos del mercado, podemos crear un método de obtención de los datos del mercado.

Añadir el método de obtención de activos en el constructorcreateManager:

// update assets

self.updateAcc = function(callBackFuncGetAcc) {

var ret = callBackFuncGetAcc(self)

if (!ret) {

return false

}

self.accData = ret

return true

}

Del mismo modo, para los formatos devueltos por diferentes interfaces de plataformas y los nombres de los campos son diferentes, aquí tenemos que utilizar la función de devolución de llamada para hacer el procesamiento especializado.

Tomemos Huobi Spot y Binance Futures como ejemplos, y la función de devolución de llamada se puede escribir así:

// the callback function of obtaining the account assets

var callBackFuncGetHuobiAcc = function(self) {

var account = self.e.GetAccount()

var ret = []

if (!account) {

return false

}

// construct the array structure of assets

var list = account.Info.data.list

_.each(self.subscribeList, function(symbol) {

var coinName = symbol.split("usdt")[0]

var acc = {symbol: symbol}

for (var i = 0 ; i < list.length ; i++) {

if (coinName == list[i].currency) {

if (list[i].type == "trade") {

acc.Stocks = parseFloat(list[i].balance)

} else if (list[i].type == "frozen") {

acc.FrozenStocks = parseFloat(list[i].balance)

}

} else if (list[i].currency == "usdt") {

if (list[i].type == "trade") {

acc.Balance = parseFloat(list[i].balance)

} else if (list[i].type == "frozen") {

acc.FrozenBalance = parseFloat(list[i].balance)

}

}

}

ret.push(acc)

})

return ret

}

var callBackFuncGetFutures_BinanceAcc = function(self) {

self.e.SetCurrency("BTC_USDT") // set to USDT-margined contract trading pair

self.e.SetContractType("swap") // all are perpetual contracts

var account = self.e.GetAccount()

var ret = []

if (!account) {

return false

}

var balance = account.Balance

var frozenBalance = account.FrozenBalance

// construct asset data structure

_.each(self.subscribeList, function(symbol) {

var acc = {symbol: symbol}

acc.Balance = balance

acc.FrozenBalance = frozenBalance

ret.push(acc)

})

return ret

}

Operar la estructura estratégica con la función de obtener datos y activos de mercado

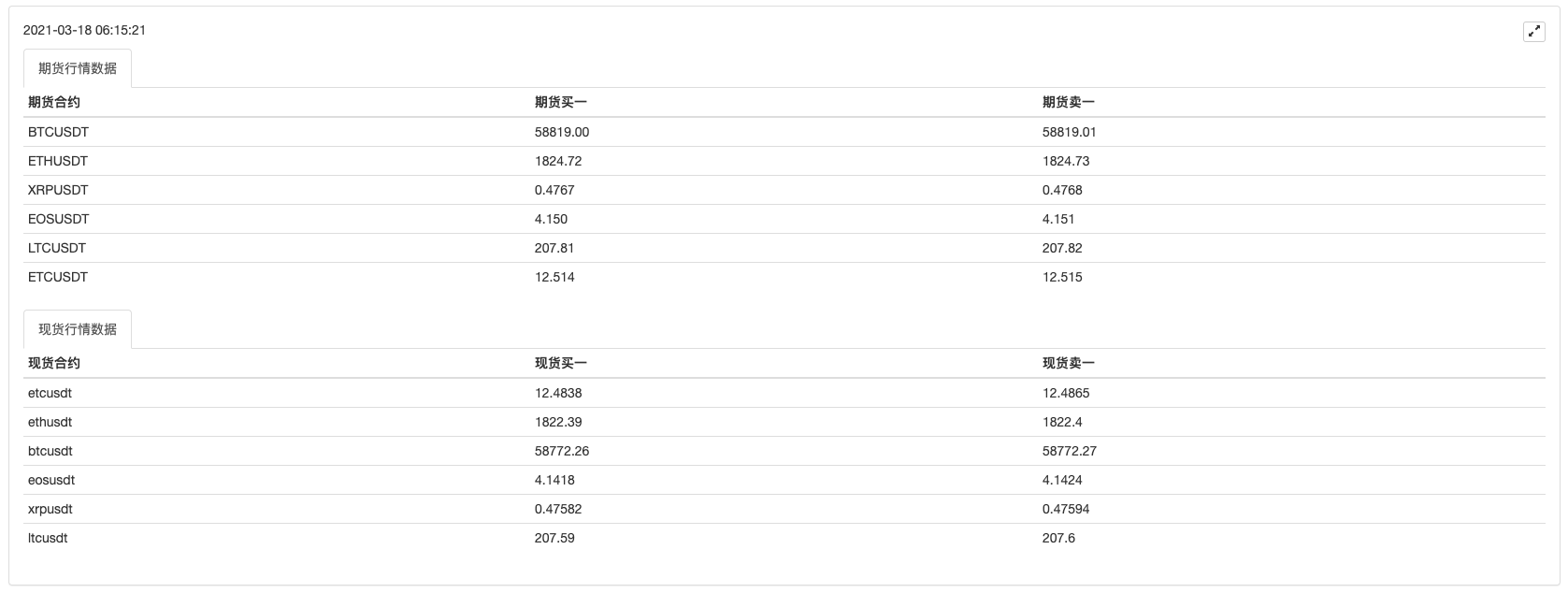

Mercado:

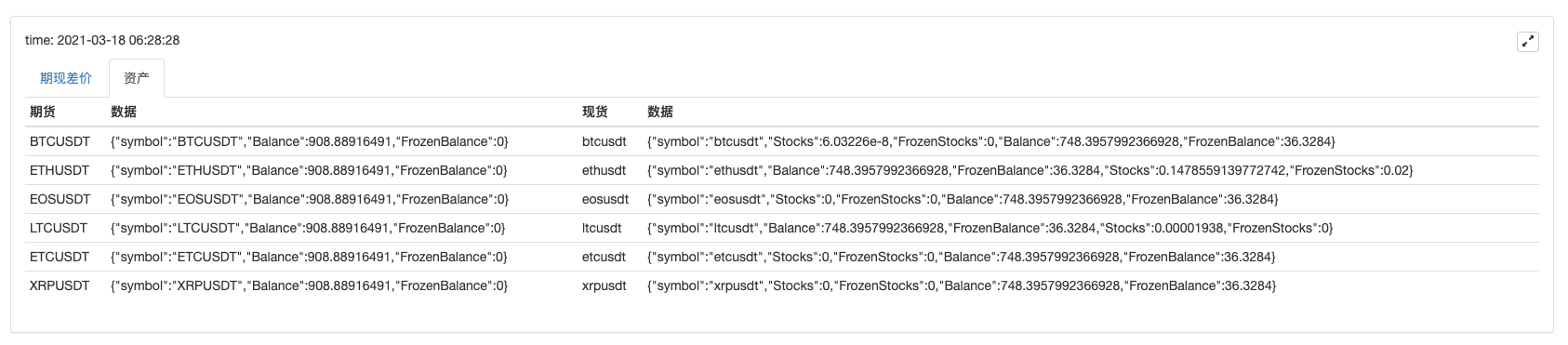

Activos y pérdidas

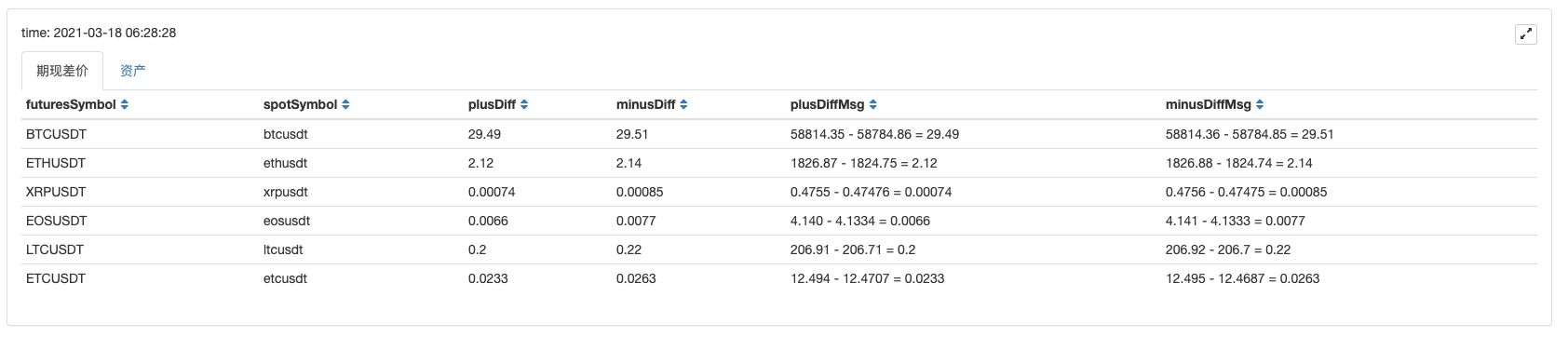

Se puede ver que después de obtener los datos del mercado, se pueden procesar los datos para calcular el margen de precios de cada símbolo, y monitorear el precio de los futuros al contado de múltiples pares comerciales. Y luego se puede diseñar una estrategia de cobertura de futuros multi-símbolo.

De acuerdo con esta forma de diseño, otras plataformas también se pueden expandir de esta manera, y los estudiantes que estén interesados pueden probarlo.

- FMZ PINE Doc de guión

- Nota y explicación de la estrategia del algoritmo de duplicación inversa de futuros

- Soluciones para obtener el mensaje de solicitud HTTP de Docker

- Extensión de plantilla personalizada mediante edición de estrategia visual (en bloque)

- Análisis de la estrategia de cosechadora de beneficios (2)

- Análisis de la estrategia de cosecha de beneficios (1)

- ¿Cuál de las funciones que afectan a esto es la que se necesita cambiar?

- Añadir Stoploss para controlar los riesgos

Cuál es el precio - Discusión sobre el diseño de estrategias de alta frecuencia

Magicamente modificado cosechador de ganancias - Arbitraje de la tasa de financiación perpetua de Binance (100% de la tasa anualizada en el mercado alcista)

- ¿Cómo se escribe aquí para que haya una señal?

- Se aplicarán las siguientes condiciones:

- Utilice SQLite para construir la base de datos cuántica FMZ

- Novato, comprueba

Te llevará al comercio cuantitativo de criptomonedas (8) - Novato, comprueba

Te llevará al comercio cuantitativo de criptomonedas (7) - Novato, comprueba

Te llevará al comercio cuantitativo de criptomonedas (6) - Novato, comprueba

Te llevará al comercio cuantitativo de criptomonedas (3) - Novato, comprueba

Te llevará al comercio cuantitativo de criptomonedas (2) - Mi inventor tiene el tiempo equivocado.

- ¡Damos ideas para la estrategia de escritura de Dios!