Las redes de contratos de baja calidad

El autor:El Nobel, Fecha: 2021-11-18 17:28:35Las etiquetas:

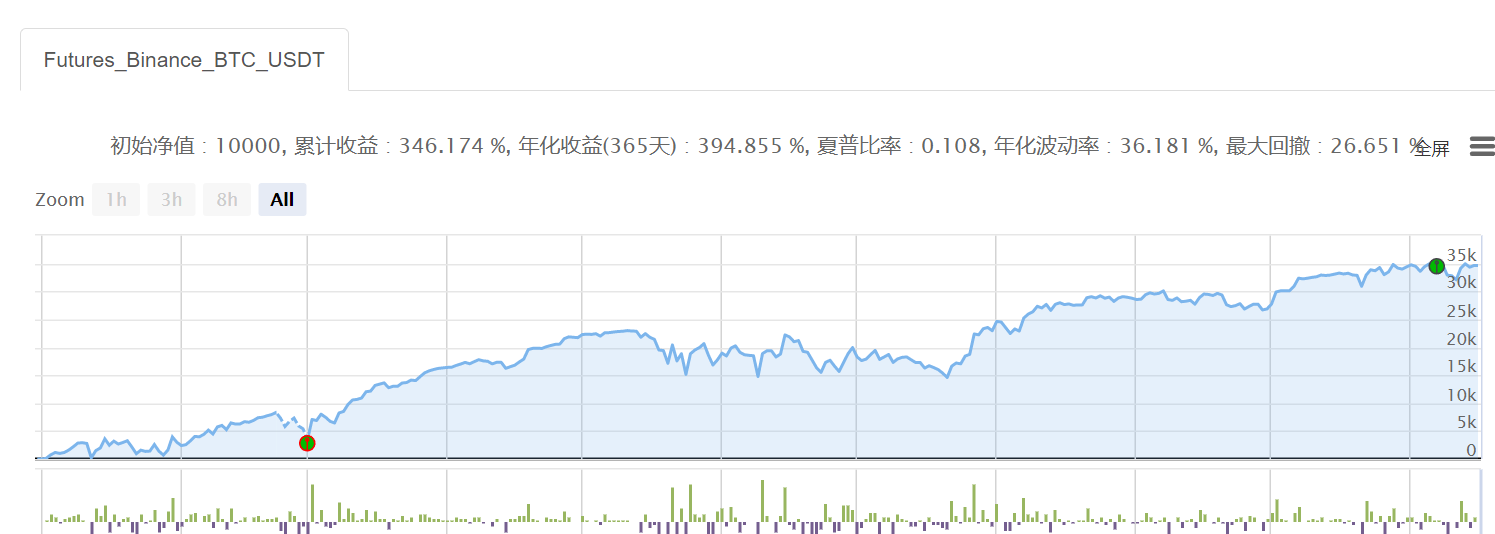

Los parámetros son muy simples, tomando BTC como ejemplo, a la zona donde hay mucho espacio, a la zona donde hay mucho espacio, a la zona donde hay mucho espacio, repetidamente.

Obviamente, en el círculo monetario, en el largo plazo, ningún modelo complejo puede funcionar en una red sin cerebro.

El código de la riqueza es una red sin cerebro + un perro sin cerebro.

La esperanza, al igual que el primer Martin, es la estrategia más simple, brutal, pero rentable.

'''backtest

start: 2021-01-01 00:00:00

end: 2021-11-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":2500}]

args: [["H",30],["n1",0.001],["grid",300],["xia",50000]]

'''

def CancelPendingOrders():

orders = _C(exchanges[0].GetOrders)

if len(orders)>0:

for j in range(len(orders)):

exchanges[0].CancelOrder(orders[j].Id, orders[j])

j=j+1

def main():

exchange.SetContractType('swap')

exchange.SetMarginLevel(M)

currency=exchange.GetCurrency()

if _G('buyp') and _G('sellp'):

buyp=_G('buyp')

sellp=_G('sellp')

Log('读取网格价格')

else:

ticker=exchange.GetTicker()

buyp=ticker["Last"]-grid

sellp=ticker["Last"]+grid

_G('buyp',buyp)

_G('sellp',sellp)

Log('网格数据初始化')

while True:

account=exchange.GetAccount()

ticker=exchange.GetTicker()

position=exchange.GetPosition()

orders=exchange.GetOrders()

if len(position)==0:

if ticker["Last"]>shang:

exchange.SetDirection('sell')

exchange.Sell(-1,n1*H)

Log(currency,'到达开空区域,买入空头底仓')

else:

exchange.SetDirection('buy')

exchange.Buy(-1,n1*H)

Log(currency,'到达开多区域,买入多头底仓')

if len(position)==1:

if position[0]["Type"]==1:

if ticker["Last"]<xia:

Log(currency,'空单全部止盈反手')

exchange.SetDirection('closesell')

exchange.Buy(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('sell')

exchange.Sell(sellp,n1)

exchange.SetDirection('closesell')

exchange.Buy(buyp,n1)

if len(orders)==1:

if orders[0]["Type"]==1: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

if orders[0]["Type"]==0:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if position[0]["Type"]==0:

if ticker["Last"]>float(shang):

Log(currency,'多单全部止盈反手')

exchange.SetDirection('closebuy')

exchange.Sell(-1,position[0].Amount)

else:

orders=exchange.GetOrders()

if len(orders)==0:

exchange.SetDirection('buy')

exchange.Buy(buyp,n1)

exchange.SetDirection('closebuy')

exchange.Sell(sellp,n1)

if len(orders)==1:

if orders[0]["Type"]==0: #止盈成交

Log(currency,'网格减仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp+grid

sellp=sellp+grid

LogProfit(account["Balance"])

if orders[0]["Type"]==1:

Log(currency,'网格加仓,当前份数:',position[0].Amount)

CancelPendingOrders()

buyp=buyp-grid

sellp=sellp-grid

LogProfit(account["Balance"])

- Las estrategias de equilibrio de las monedas de los monedas de los monedas de los monedas de los monedas U

- Las estrategias ATR para los futuros de las monedas digitales son muy variadas.

- Transferir USDT de una cuenta de contrato a una cuenta de efectivo/dinero ((OKEX, Binance con soporte simultáneo)

- La herramienta de transferencia de fondos de los terminales de transacción de Bitcoin

- Todos los pedidos en la cuenta se muestran en U.

- El instrumento de liquidación Binance se abre manualmente

- Obtener datos de las líneas de Binance K directamente con HttpQuery

- Las estrategias de doble línea para el comercio de divisas digitales (enseñanza)

- Las tasas de capital de las principales bolsas

- Las estrategias de los puntos de inflexión de los futuros de las monedas digitales (enseñanza)

- Estrategia de equilibrio del índice de liquidez v1.1 (que ha estado funcionando durante un tiempo, y ahora se sospecha que hay un error, ya que no sirve, debe ser modificado)

- Obtener el nombre completo de la moneda del contrato USDT

- Información sobre el mercado de suscripción a contratos permanentes en Binance websocket

- Se abre el nuevo monedero

- Cuando alguien hace explosión, cambia de dirección.

- Obtener automáticamente la precisión y el mínimo de apertura de operaciones de contratos perpetuos de Bitcoin (abandonado)

- Los contratos permanentes en el mercado de la paridad

- Estrategia para el equilibrio de los productos al contado - 0.0.1v

- La red de contratos de Binance - 0.0.2v

- Indicador de cobertura (campo de tiro) 0.0.1

Mexmina¿Qué pasa con la gramática circular de for?

Nube ligeraPor favor, instruyanme, el disco real ha recibido un error en Traceback (most recent call last): File "

Nube ligeraYo soy un súper fan, si puedo escribir un libro con JS, será mejor O ((

Nube ligeraEstá bien, gracias.

El NobelY esto es un problema de la estructura de la matriz de posición.