Estrategia de trading cuantitativo multifactorial que combina momentum y juicio de tendencia

Resumen

Esta estrategia es una estrategia de trading cuantitativa de juicio multifactorial que combina indicadores de momentum e indicadores de tendencia. La estrategia calcula combinaciones matemáticas de múltiples medias móviles para determinar la tendencia general y la dirección del momentum del mercado, y emite señales de trading según condiciones de umbral.

Principio de la estrategia

- Calcular múltiples conjuntos de medias móviles e indicadores de momentum

- Calcular múltiples medias móviles, como la media armónica, la media a corto plazo, la media a medio plazo y la media a largo plazo.

- Calcular las diferencias entre cada media móvil para reflejar la tendencia de cambio de precio.

- Calcular la primera derivada de cada media móvil para reflejar el momentum del cambio de precio.

- Calcular indicadores de seno y coseno para determinar la dirección de la tendencia.

- Evaluar integralmente las señales de trading

- Realizar una operación ponderada de múltiples factores, como indicadores de momentum e indicadores de tendencia.

- Según la distancia del valor resultante al umbral, determinar el estado actual del mercado.

- Emitir señales de trading de largo y corto.

Análisis de ventajas

- Juicio multifactorial, mejora la precisión de las señales

- Considera de manera integral múltiples factores como precio, tendencia y momentum.

- Se pueden configurar diferentes pesos para diferentes factores.

- Parámetros ajustables, se adapta a diferentes mercados

- Los parámetros de las medias móviles y los límites del rango de trading se pueden personalizar.

- Se puede adaptar a diferentes períodos y entornos de mercado.

- Estructura del código clara, fácil de entender

- Nomenclatura estandarizada, comentarios completos.

- Fácil de desarrollar y optimizar secundariamente.

Análisis de riesgos

- La optimización de parámetros es difícil

- Se necesita una gran cantidad de datos históricos para backtesting a fin de encontrar los parámetros óptimos.

- La frecuencia de trading puede ser demasiado alta

- El juicio combinado de múltiples factores puede generar demasiadas transacciones.

- El efecto tiene una alta correlación con el mercado

- Una estrategia de juicio de tendencia es susceptible a comportamientos irracionales.

Direcciones de optimización

- Agregar lógica de stop-loss

- Puede evitar pérdidas significativas causadas por comportamientos irracionales.

- Optimizar la configuración de parámetros

- Encontrar la combinación óptima de parámetros para mejorar la estabilidad de la estrategia.

- Agregar elementos de aprendizaje automático

- Utilizar aprendizaje profundo para determinar el estado actual del mercado y ayudar en la toma de decisiones de la estrategia.

Conclusión

Esta estrategia evalúa el estado del mercado mediante una combinación multifactorial de indicadores de momentum e indicadores de tendencia, y emite señales de trading según los umbrales establecidos. Las ventajas de la estrategia son su alta capacidad de configuración, su idoneidad para diferentes entornos de mercado y su fácil comprensión; las desventajas son la dificultad en la optimización de parámetros, la posible alta frecuencia de trading y la fuerte correlación del efecto con el mercado. En el futuro, se puede optimizar aún más agregando stop-loss, optimizando parámetros y utilizando aprendizaje automático, entre otros medios.

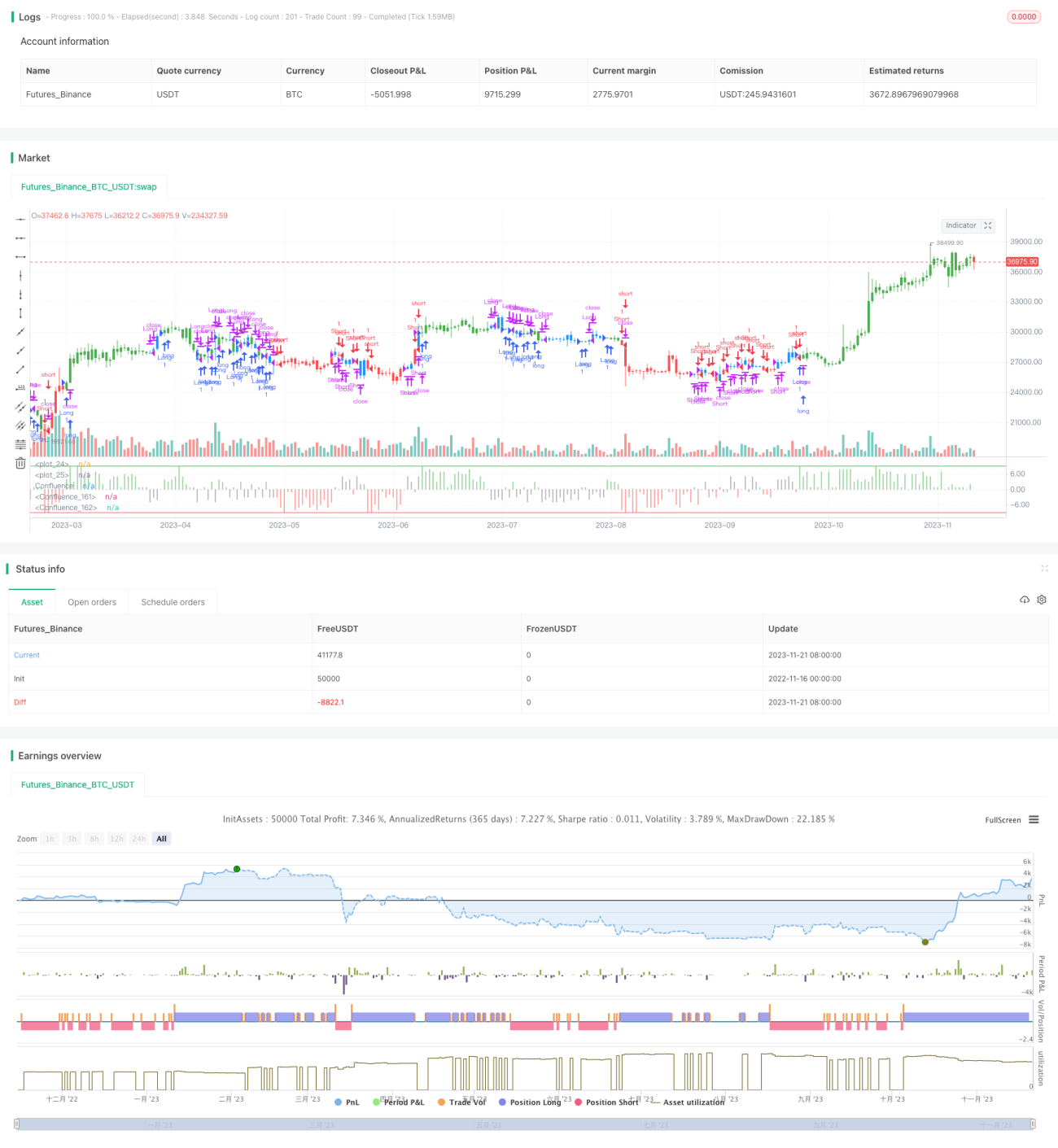

/*backtest

start: 2022-11-16 00:00:00

end: 2023-11-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/03/2017

// This is modified version of Dale Legan's "Confluence" indicator written by Gary Fritz.- 1