Estrategia de trading de Bitcoin basada en indicadores cuantitativos

Resumen

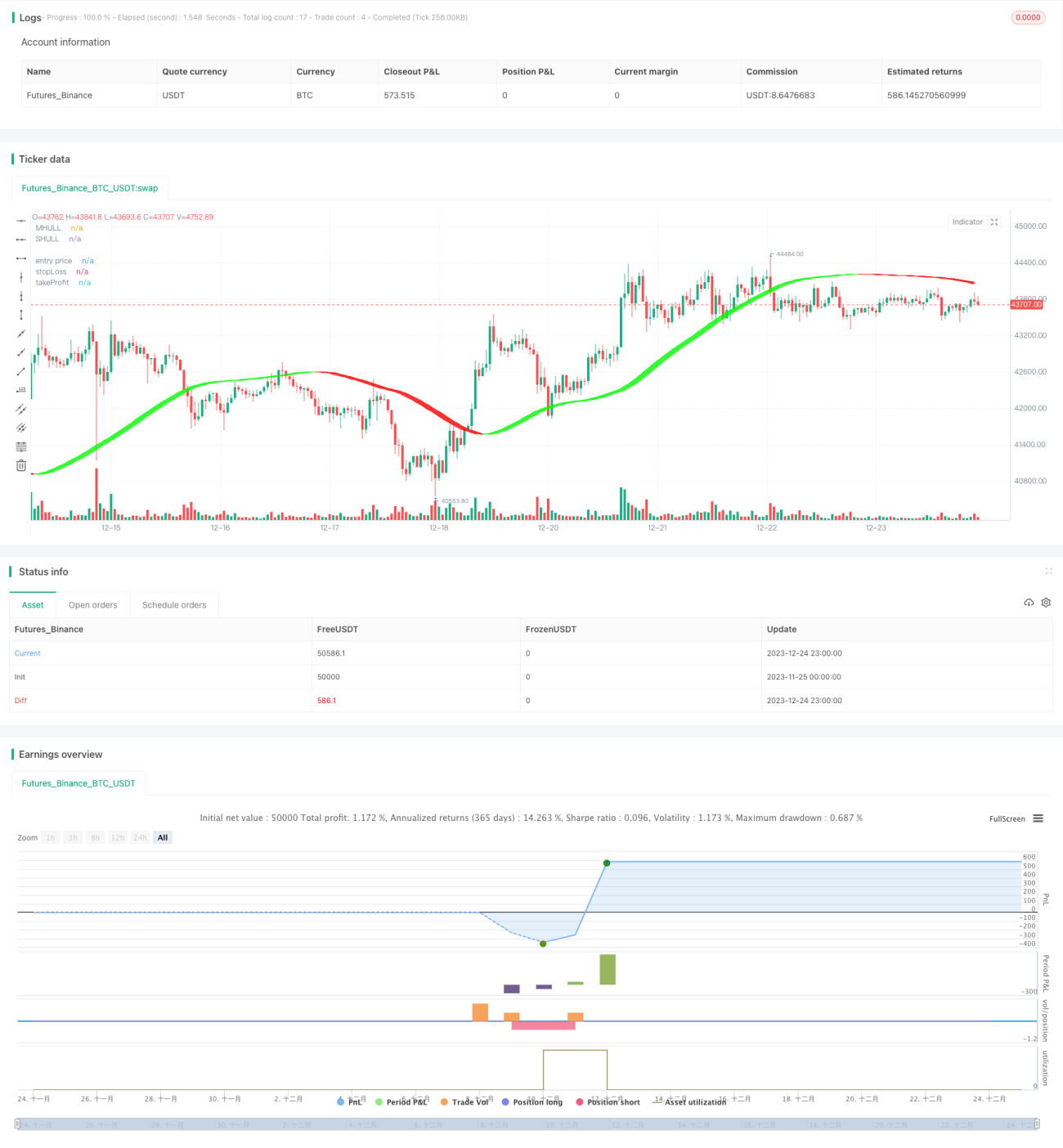

Esta estrategia utiliza múltiples indicadores cuantitativos para determinar los momentos de compra y venta de Bitcoin, logrando un trading automatizado. Incluye principalmente el indicador Hull, el índice de fuerza relativa (RSI), las Bandas de Bollinger (BB) y el oscilador de volumen (VO).

Principio de la estrategia

-

Se utiliza una media móvil Hull modificada para determinar la dirección principal de la tendencia del mercado, combinada con las Bandas de Bollinger para ayudar a identificar puntos de ruptura de compra y venta.

-

El indicador RSI, junto con un rango de volatilidad adaptativo, identifica zonas de sobrecompra y sobreventa, generando señales de trading. Además, se configuran dos conjuntos de parámetros como verificación de señales Duplicate.

-

El oscilador de volumen evalúa la fuerza de compra y venta, evitando falsas rupturas.

-

Se establecen niveles de stop loss y take profit predefinidos según la relación de parámetros de precio de stop loss/take profit, logrando una gestión de riesgos.

Análisis de ventajas

-

La curva Hull puede detectar cambios de tendencia más rápidamente, y la ayuda de las Bandas de Bollinger reduce las señales falsas.

-

La optimización de los parámetros del RSI y la verificación con señales Duplicate aumentan la fiabilidad.

-

El oscilador de volumen, combinado con la tendencia y las señales de los indicadores, evita operaciones inexactas.

-

El método de stop loss y take profit predefinido controla automáticamente las pérdidas y ganancias individuales, gestionando eficazmente el riesgo global.

Análisis de riesgos

-

Una configuración inadecuada de los parámetros puede provocar una frecuencia de trading demasiado alta o un empeoramiento de la efectividad de las señales.

-

Cuando eventos inesperados causan una volatilidad extrema en el mercado, el stop loss podría ser superado, generando pérdidas significativas.

-

Al cambiar el activo a otra criptomoneda, es necesario reajustar y optimizar los parámetros.

-

Si faltan datos de volumen, el oscilador de volumen dejará de funcionar.

Direcciones de optimización

-

Realizar más pruebas de combinaciones de parámetros del RSI para encontrar los valores óptimos.

-

Probar otros indicadores como MACD, KD, etc., en combinación con el RSI para mejorar la precisión de las señales.

-

Agregar un módulo de predicción de modelos, combinando aprendizaje automático para determinar la dirección del mercado.

-

Probar el efecto de los parámetros al cambiar a otros activos de trading.

-

Optimizar el algoritmo de stop loss y take profit para maximizar las ganancias.

Conclusión

Esta estrategia integra múltiples indicadores técnicos cuantitativos para determinar los momentos de compra y venta. Mediante la optimización de parámetros y el control de riesgos, logra la negociación automatizada de Bitcoin. Los resultados son relativamente buenos, pero aún requiere pruebas y optimización continuas para adaptarse a los cambios del mercado. Puede servir como referencia para inversores y ayudar en la toma de decisiones de trading.

- 1