Estrategia de seguimiento de tendencia basada en QQE y MA

Resumen

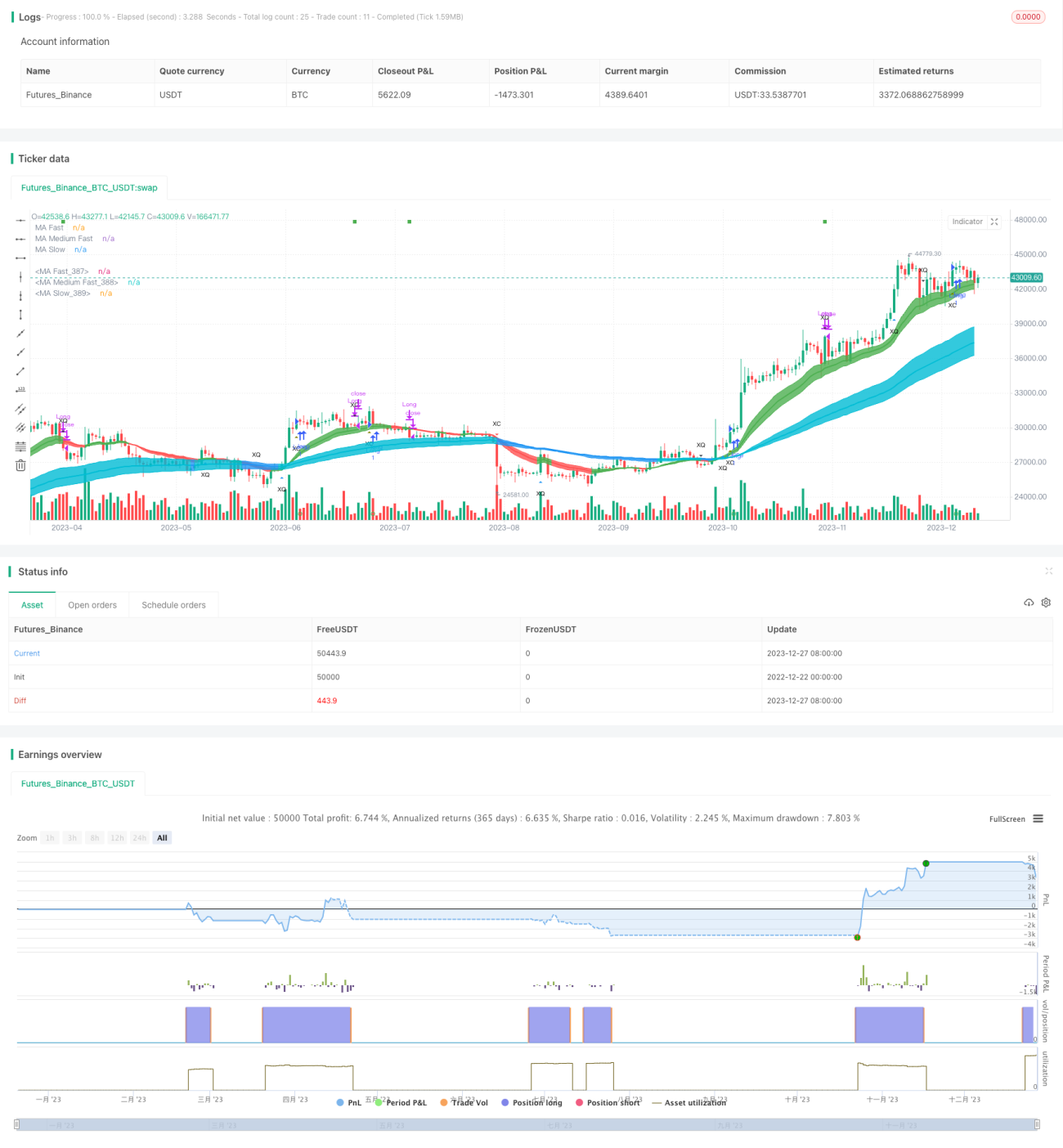

Esta estrategia es una estrategia de seguimiento de tendencia basada en el indicador QQE (Quantitative Qualitative Estimation) y medias móviles. Determina la dirección de la tendencia mediante el cruce del indicador QQE rápido y el filtro de la dirección de la media móvil, generando señales de compra y venta.

La estrategia puede seleccionar tres tipos de cruces del indicador QQE para determinar las señales: (1) cruce del RSI suavizado con el eje 0; (2) cruce del RSI suavizado con la línea QQE rápida; (3) salida del RSI suavizado del canal de umbral RSI. Por defecto, se utiliza el tercer tipo de cruce para abrir posiciones y el segundo para cerrarlas.

Las señales de compra y venta pueden filtrarse adicionalmente mediante medias móviles: el precio de cierre debe estar por encima (por debajo) de la media móvil rápida, y la media móvil rápida debe estar por encima (por debajo) de la media móvil lenta para generar la señal.

Esta estrategia es adecuada para su uso en modo de señal a señal en sistemas de trading automatizado.

Principio

El indicador central de la estrategia es el QQE, cuya fórmula de cálculo es la siguiente:

Wilders_Period = RSILen * 2 - 1

Rsi = rsi(close,RSILen)

RSIndex = ema(Rsi, SF)

AtrRsi = abs(RSIndex - RSIndex[1])

MaAtrRsi = ema(AtrRsi, Wilders_Period)

DeltaFastAtrRsi = ema(MaAtrRsi,Wilders_Period) * QQEfactor

newshortband = RSIndex + DeltaFastAtrRsi

newlongband = RSIndex - DeltaFastAtrRsi

Donde RSILen es la longitud del período del RSI, y SF es el factor de suavizado del RSI. El QQE es esencialmente un RSI suavizado. Calcula canales superior e inferior mediante un ATR rápido; cuando el precio supera el canal, se considera una oportunidad de compra o venta.

La estrategia utiliza tres tipos de cruces del QQE para identificar señales de trading:

- Cruce del RSI suavizado con el eje 0 (XZ)

QQEzlong = RSIndex >= 50 ? QQEzlong + 1 : 0

QQEzshort = RSIndex < 50 ? QQEzshort + 1 : 0

- Cruce del RSI suavizado con el indicador QQE rápido (XQ), similar a una señal de oscilación anticipada

QQExlong = FastAtrRsiTL < RSIndex ? QQExlong + 1 : 0

QQExshort = FastAtrRsiTL > RSIndex ? QQExshort + 1 : 0

- Salida del RSI suavizado del canal de umbral (XC), similar a una señal de oscilación confirmada

threshhold = 10

QQEclong = RSIndex > (50 + threshhold) ? QQEclong + 1 : 0

QQEcshort = RSIndex < (50 - threshhold) ? QQEcshort + 1 : 0

Se puede elegir uno o varios de los tres cruces anteriores para identificar señales de compra/venta y señales de cierre.

Las señales de compra y venta pueden filtrarse adicionalmente mediante medias móviles:

// Condiciones de filtro

QQEflong = close > ma_medium y

ma_medium > ma_slow y

ma_fast > ma_medium

QQEfshort = close < ma_medium y

ma_medium < ma_slow y

ma_fast < ma_medium

Esto evita señales falsas en mercados laterales.

La estrategia es adecuada para trading automatizado, utilizando diferentes cruces del QQE para abrir y cerrar posiciones:

Señal de apertura = XC o XQ o XZ

Señal de cierre = XQ o XZ

Ventajas

Esta estrategia presenta las siguientes ventajas:

-

Utiliza el indicador QQE para determinar la tendencia y las señales de cruce. El QQE tiene propiedades de suavizado y reducción de ruido, lo que reduce las señales falsas.

-

La combinación con medias móviles como filtro evita aún más las señales falsas en mercados laterales, mejorando la calidad de las señales.

-

Permite seleccionar diferentes cruces del QQE para abrir y cerrar posiciones, facilitando el trading automatizado.

-

Debido al retardo del RSI suavizado, las señales de compra y venta no se redibujan.

-

Se puede optimizar en diferentes marcos temporales para encontrar la mejor combinación de parámetros.

Riesgos

La estrategia también conlleva ciertos riesgos:

-

En las reversiones de tendencia, puede generar señales falsas; es necesario establecer un stop loss para controlar el riesgo.

-

Una configuración inadecuada de parámetros también puede afectar el rendimiento de la estrategia; se requieren múltiples pruebas de optimización para encontrar los mejores parámetros.

-

Los parámetros para diferentes instrumentos y marcos temporales deben probarse y optimizarse por separado.

-

El trading mecanizado conlleva el riesgo de drawdown y pérdidas consecutivas; se necesita una gestión de capital adecuada.

Las soluciones correspondientes son las siguientes:

-

Establecer un stop loss para salir cuando las pérdidas alcancen un cierto nivel.

-

Probar diferentes combinaciones de parámetros en detalle para encontrar los óptimos.

-

Ajustar los parámetros según las características del instrumento y el período.

-

Realizar una gestión de capital adecuada, abrir posiciones por lotes y controlar el tamaño de cada operación.

Direcciones de optimización

La estrategia se puede optimizar en las siguientes direcciones:

-

Optimizar los parámetros del QQE, incluyendo la longitud del RSI, la longitud de suavizado del RSI, la longitud del ATR rápido, etc., para encontrar la combinación óptima de parámetros.

-

Optimizar los parámetros de las medias móviles, ajustando el período, el tipo, etc., para lograr la mejor coincidencia con el indicador QQE.

-

Probar diferentes cruces del QQE para abrir y cerrar posiciones, buscando la combinación más estable.

-

Ajustar los parámetros según el instrumento y el período de trading. El trading intradía puede acortar los períodos para aumentar la sensibilidad.

-

Agregar un mecanismo de stop loss. Detener la pérdida cuando alcance un cierto porcentaje.

-

Reducir adecuadamente el tamaño de las posiciones y probar diferentes métodos de gestión de tamaño.

Resumen

Esta estrategia integra el indicador QQE para determinar la tendencia y las señales de cruce, y utiliza medias móviles como filtro para generar señales de trading. En la operativa real, se puede ajustar los parámetros para optimizar la calidad de las señales y combinarlo con una gestión de capital estricta para controlar el riesgo. La estrategia es adecuada para su uso en modo de señal a señal en sistemas de trading automatizado, así como para ayudar en la toma de decisiones en trading discrecional. Mediante la optimización de parámetros y reglas, se puede adaptar a más entornos de mercado.

- 1