Estrategia cuantitativa combinada de triple media móvil y MACD

Resumen

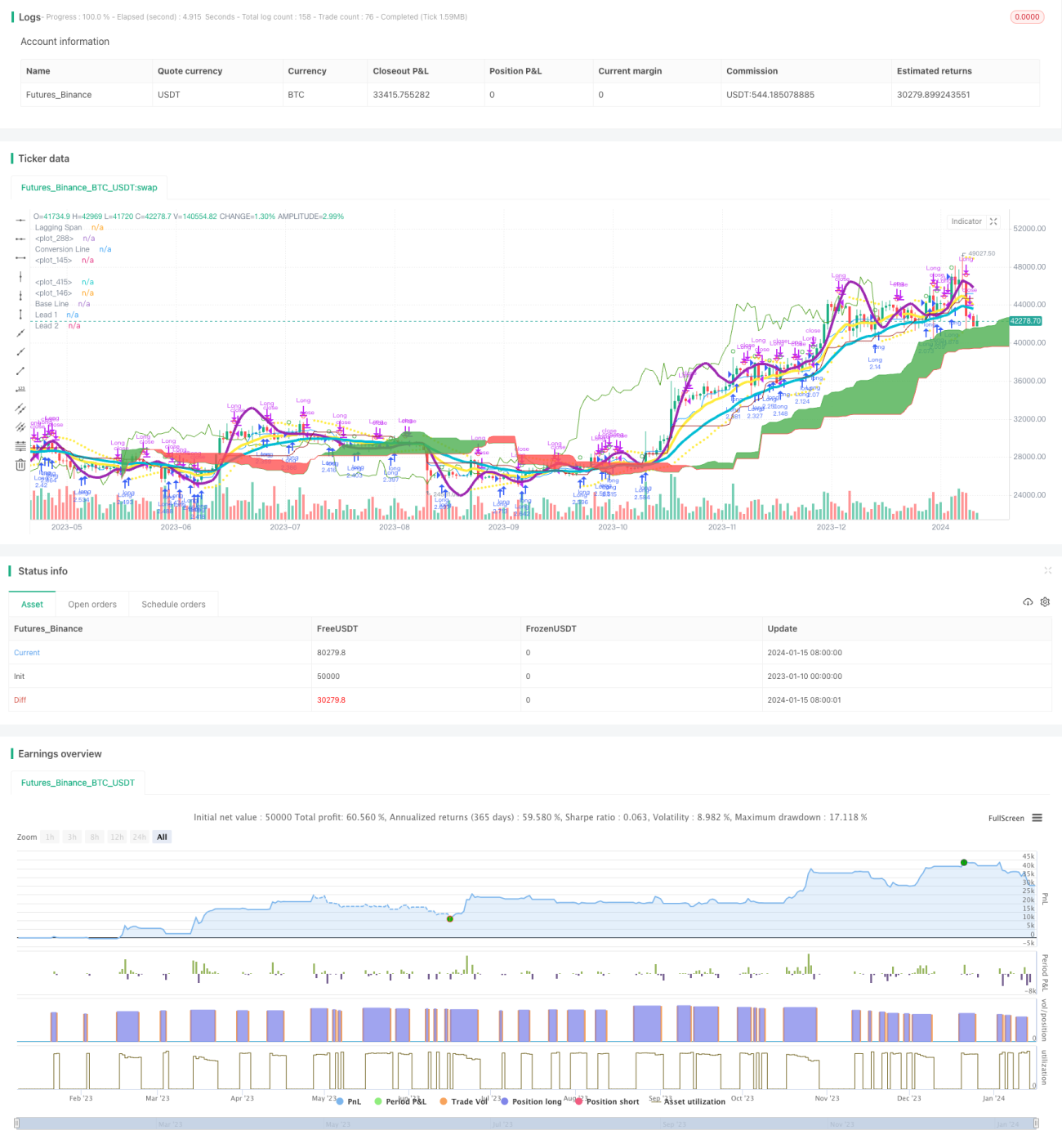

Esta estrategia desarrolla una estrategia de trading cuantitativo relativamente estable y confiable mediante el uso combinado del indicador de triple media móvil y el indicador MACD. La estrategia tiene como objetivo capturar posibles tendencias futuras, siendo especialmente adecuada para posiciones de medio y largo plazo.

Principio de la estrategia

La estrategia se basa principalmente en el uso combinado de la triple media móvil y el indicador MACD.

En primer lugar, la estrategia utiliza tres medias móviles exponenciales de longitudes 3, 7 y 2 respectivamente. Estas tres medias móviles construyen un sistema de medias móviles que va desde lo rápido hasta lo lento, utilizado para determinar la dirección de la tendencia futura. Cuando la media móvil de corto plazo cruza por encima de la media móvil de largo plazo, es una señal de compra; cuando la media móvil de corto plazo cruza por debajo de la media móvil de largo plazo, es una señal de venta.

En segundo lugar, la estrategia también utiliza el indicador MACD con parámetros 3 y 7. Cuando la línea principal del MACD cruza por encima de la línea de señal, es una señal de compra; cuando cruza por debajo, es una señal de venta.

Al combinar el uso de dos indicadores, se pueden evitar las múltiples señales erróneas causadas por un solo indicador, mejorando así la estabilidad de la estrategia.

Ventajas de la estrategia

- Uso de doble filtro de indicadores para mejorar la calidad de las señales.

- Parámetros optimizados tras múltiples pruebas, estables y fiables.

- El sistema de triple media móvil filtra eficazmente el ruido del mercado y determina la tendencia futura.

- Los parámetros del MACD son rápidos, permitiendo capturar oportunidades de corto plazo rápidamente.

Riesgos de la estrategia

- Existe cierto riesgo de retrocesos y pérdidas continuas.

- Cuando el mercado no presenta una tendencia clara, la estrategia genera un mayor número de operaciones erróneas.

- El indicador MACD tiende a generar señales falsas, por lo que debe combinarse con indicadores de medias móviles.

Soluciones:

- Adoptar una estrategia de stop loss adecuada para controlar el retroceso máximo.

- Reducir la frecuencia de trading cuando el estado del mercado es claramente sin tendencia.

- Optimizar los parámetros del MACD y combinarlo con otros indicadores.

Direcciones de optimización de la estrategia

- Probar y optimizar los parámetros de las medias móviles y el MACD para encontrar la mejor combinación.

- Agregar indicadores auxiliares como KDJ, VRSI para evitar señales falsas.

- Incorporar modelos de aprendizaje automático para determinar el estado del mercado y lograr ajustes dinámicos.

- Combinar con estrategias de stop loss para establecer el punto óptimo de stop loss.

Conclusión

Esta estrategia logra una captura estable de tendencias mediante la combinación de medias móviles y MACD. Su ventaja radica en el uso combinado de indicadores, lo que reduce eficazmente las señales falsas y obtiene buenos resultados. Como próximo paso, se perfeccionará la estrategia mediante la optimización de parámetros, la introducción de stop loss y el ajuste dinámico, convirtiéndola en una herramienta eficaz para buscar oportunidades de medio y largo plazo.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1