Estrategia de ruptura impulsada por sentimiento que integra múltiples indicadores

Resumen

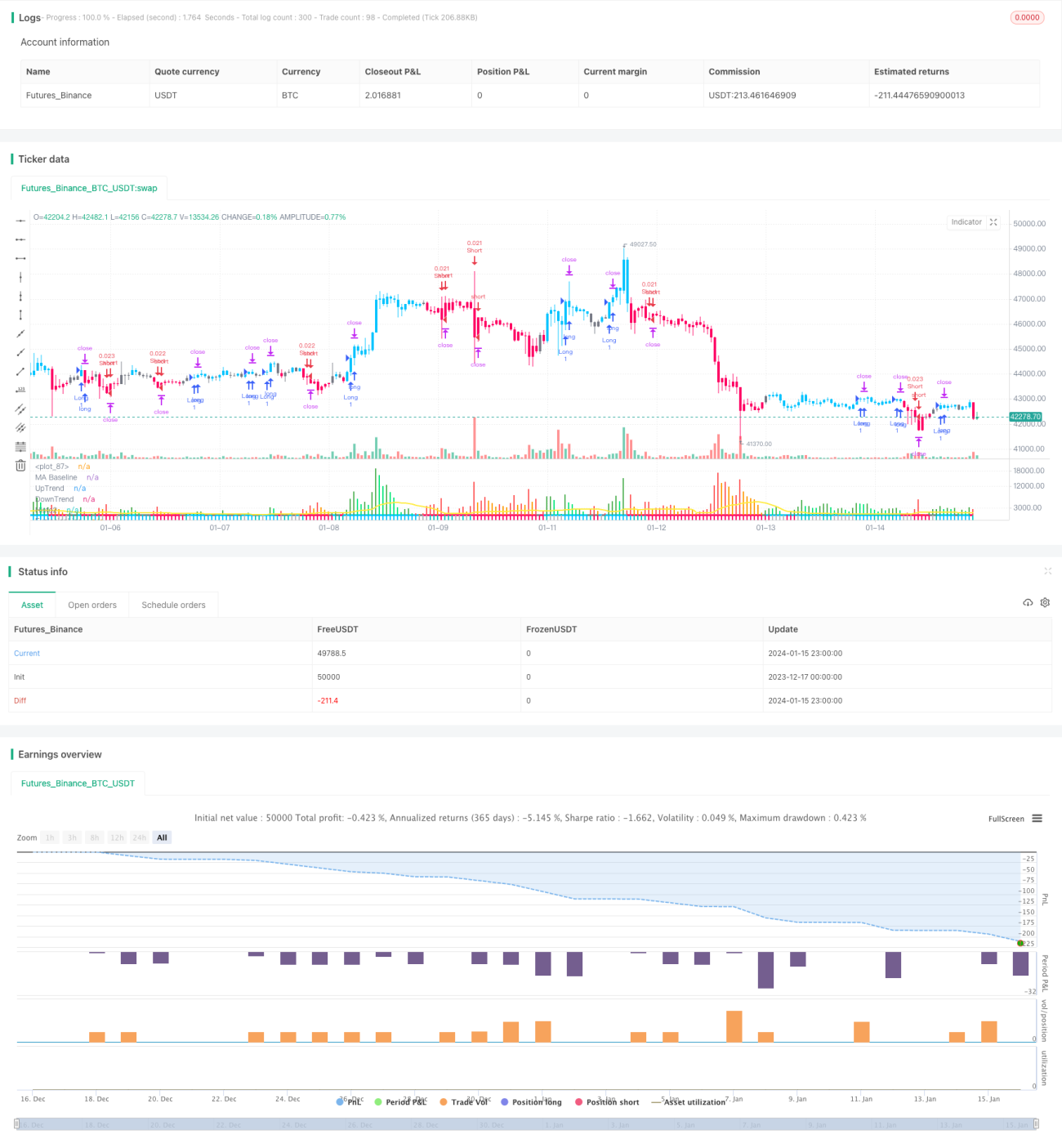

Esta estrategia combina tres indicadores emocionales: el indicador QQE mejorado, el indicador híbrido SSL y el indicador de explosión Waddah Attar para generar señales de trading. Es una estrategia de ruptura emocional impulsada por múltiples indicadores. Puede evaluar el sentimiento del mercado antes de una ruptura, evitando falsas rupturas, lo que la convierte en una estrategia de ruptura de alta calidad.

Principio de la Estrategia

La lógica central de esta estrategia se basa en tres indicadores para tomar decisiones de trading:

Indicador QQE mejorado: Este indicador es una mejora del RSI, haciéndolo más sensible para determinar niveles altos y bajos del sentimiento del mercado. La estrategia lo utiliza para identificar señales de reversión en el suelo y en el techo.

Indicador híbrido SSL: Este indicador considera la ruptura de múltiples medias móviles para determinar las señales del mercado. La estrategia lo utiliza para identificar patrones de ruptura de canales.

Indicador de explosión Waddah Attar: Este indicador mide la fuerza de la explosión del precio dentro del canal. La estrategia lo utiliza para confirmar que el impulso durante la ruptura es suficiente.

Cuando el indicador QQE emite una señal de reversión en el suelo, el indicador SSL muestra una ruptura por encima del canal superior, y el indicador Waddah Attar confirma un impulso explosivo, la estrategia genera una decisión de compra. Cuando los tres indicadores emiten simultáneamente señales opuestas, se toma una decisión de venta.

La estrategia también establece puntos de salida precisos con stop loss y take profit para maximizar las ganancias, constituyendo una estrategia de ruptura emocional de alta calidad.

Análisis de Ventajas

Esta estrategia tiene las siguientes ventajas:

- Combina múltiples indicadores para evaluar el sentimiento del mercado, evitando el riesgo de falsas rupturas.

- Considera simultáneamente indicadores de reversión, de canal y de impulso, asegurando una alta confirmación del mercado en el momento de la ruptura.

- Utiliza un stop loss móvil de alta precisión para limitar el riesgo, rastreando y asegurando las ganancias.

- Los parámetros han sido ampliamente optimizados y probados, ofreciendo buena estabilidad, adecuado para posiciones de medio a largo plazo.

- Los parámetros de los indicadores son configurables para ajustar el estilo de la estrategia, adaptándose a una gama más amplia de condiciones del mercado.

Análisis de Riesgos

Los principales riesgos de esta estrategia son:

- En mercados persistentemente bajistas, es probable que se generen muchas operaciones con pequeñas pérdidas.

- Depende de múltiples indicadores simultáneamente, que podrían fallar de manera anómala en ciertos mercados.

- Indicadores como el QQE corren el riesgo de sobreoptimización de parámetros; se deben configurar con cuidado.

- El stop loss móvil puede no funcionar correctamente en condiciones de mercado excepcionales.

Para mitigar estos riesgos, se recomienda ajustar los parámetros de los indicadores para hacerlos más estables y aumentar el período de tenencia para obtener una mayor tasa de ganancias.

Direcciones de Optimización

Esta estrategia se puede optimizar aún más en los siguientes aspectos:

- Ajustar los parámetros de cada indicador para hacerlos más estables o más sensibles.

- Agregar un módulo de optimización del tamaño de la posición basado en la volatilidad.

- Incorporar un módulo de gestión de riesgos basado en aprendizaje automático para evaluar las condiciones del mercado en tiempo real.

- Utilizar modelos de aprendizaje profundo para predecir las formas de los indicadores, mejorando la precisión de las decisiones.

- Introducir un análisis entre marcos temporales para reducir la probabilidad de falsas rupturas.

Resumen

Esta estrategia aprovecha las ventajas de múltiples indicadores emocionales predominantes para construir una estrategia de ruptura emocional eficiente. Evita con éxito muchos de los riesgos asociados con rupturas de baja calidad, al mismo tiempo que emplea un concepto de stop loss de alta precisión para asegurar ganancias. Es un conjunto de estrategias de ruptura maduro y confiable que vale la pena estudiar y aplicar. Con la optimización continua de parámetros y la introducción de modelos predictivos, se espera que esta estrategia genere rendimientos excedentes cada vez más consistentes y sostenibles.

- 1