Estrategia de seguimiento de tendencia basada en múltiples indicadores

Resumen

Esta estrategia identifica la tendencia combinando múltiples indicadores y establece un stop loss dinámico para asegurar las ganancias. Utiliza principalmente Bandas de Bollinger, RSI, ADX y otros indicadores para determinar los puntos de entrada, así como ATR y Bandas de Bollinger para el stop loss.

Principio de la estrategia

Los principales indicadores de juicio de la estrategia son las Bandas de Bollinger, RSI y ADX. Cuando el precio se acerca a la banda inferior de Bollinger y el RSI está por debajo de 30, se considera sobrevendido y se toma una posición larga; cuando el precio se acerca a la banda superior de Bollinger y el RSI está por encima de 70, se considera sobrecomprado y se toma una posición corta. Además, si el ADX supera 25, se considera que se ha formado una tendencia, lo que hace que las señales de compra y venta sean más efectivas.

Después de abrir una posición, la estrategia utiliza el indicador ATR y las bandas superior e inferior de Bollinger para el stop loss. Específicamente, el ATR se utiliza para determinar la distancia máxima de stop loss; cuando el precio alcanza el punto máximo de stop loss, se cierra la posición. Las bandas superior e inferior de Bollinger se utilizan para establecer un stop loss dinámico, actualizando en tiempo real el precio de stop loss según la evolución del precio.

Análisis de ventajas

Esta estrategia combina múltiples indicadores para identificar tendencias de manera efectiva y utiliza un mecanismo de stop loss para asegurar ganancias y reducir el riesgo de pérdidas, siendo una estrategia relativamente sólida. Las ventajas específicas son las siguientes:

- Utiliza las Bandas de Bollinger para identificar condiciones de sobrecompra/sobreventa, lo que permite detectar oportunidades de reversión.

- Combinar con el indicador RSI aumenta la precisión del juicio.

- El indicador ADX identifica la formación de tendencias, asegurando la dirección correcta de la operación.

- El stop loss dinámico con ATR y Bandas de Bollinger maximiza la captura de ganancias.

Análisis de riesgos

Esta estrategia también presenta algunos riesgos:

- El juicio con múltiples indicadores puede llevar a una optimización excesiva de los parámetros.

- Cuando el rango de las Bandas de Bollinger es demasiado amplio, las señales de sobrecompra/sobreventa son menos efectivas.

- Un seguimiento inadecuado del stop loss puede aumentar las pérdidas.

Para mitigar estos riesgos, podemos tomar las siguientes medidas:

- Realizar optimización con múltiples combinaciones de parámetros para evitar el sobreajuste.

- Ajustar los parámetros de las Bandas de Bollinger según la volatilidad del mercado.

- Probar la distancia del stop loss para asegurar que pueda soportar las fluctuaciones normales.

Direcciones de optimización

La estrategia también se puede optimizar en las siguientes áreas:

- Agregar control de posición, ajustando el tamaño de la posición según el multiplicador del stop loss.

- Incorporar un módulo de gestión de capital para controlar estrictamente la pérdida máxima por operación.

- Probar otros indicadores de stop loss, como DMI, Envelopes, etc.

- Agregar modelos de aprendizaje automático para estimar la probabilidad de tendencia y mejorar el rendimiento.

Conclusión

En general, esta estrategia es un enfoque de seguimiento de tendencias relativamente sólido. Al combinar múltiples indicadores para determinar la dirección de la tendencia y aplicar medidas de stop loss para controlar el riesgo, se puede obtener una buena relación riesgo-recompensa. También hemos propuesto varias direcciones de optimización que, si se implementan, pueden mejorar aún más los resultados.

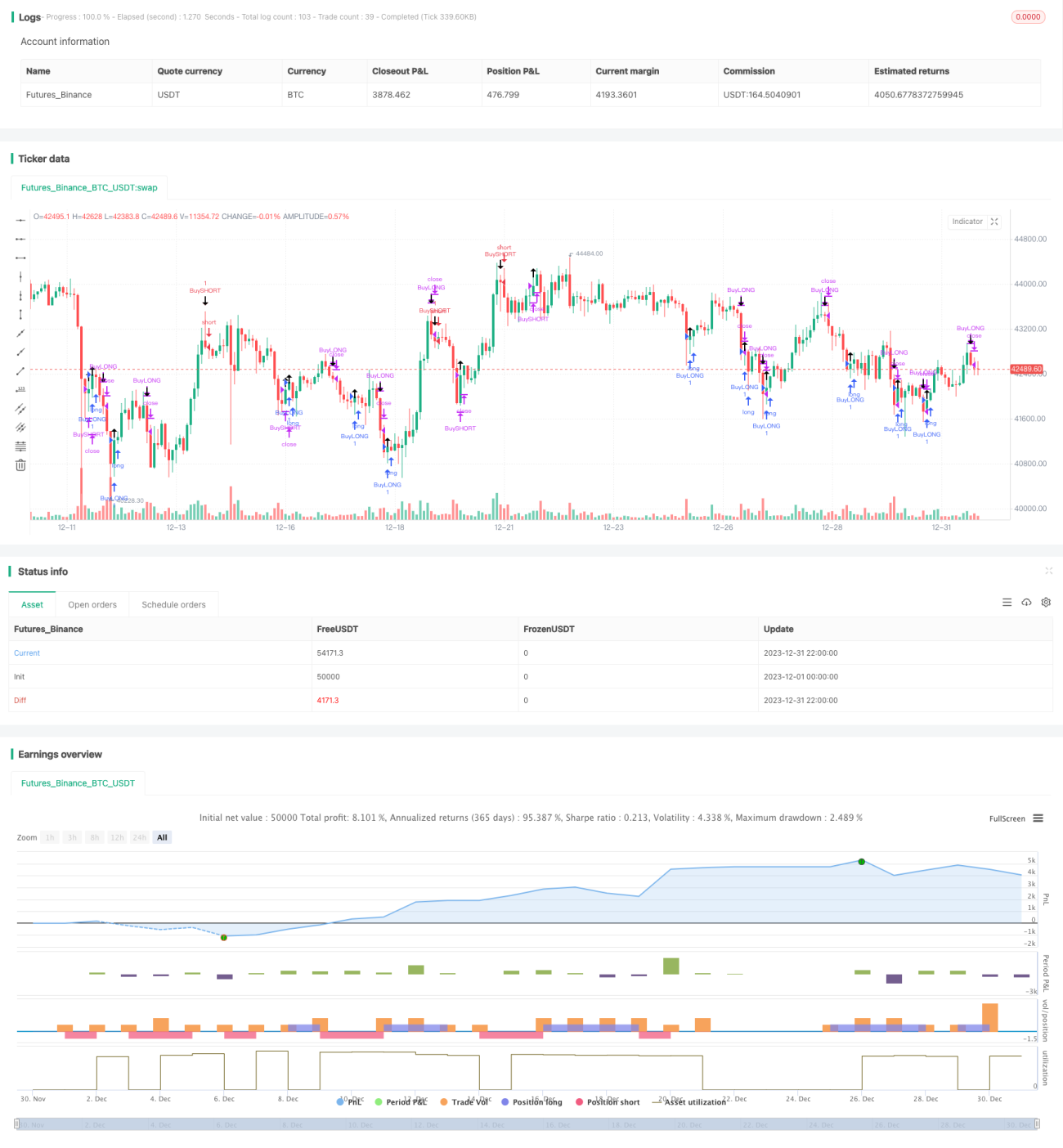

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1