Rastreador de ballenas

VS, ATR, MA200, HTF

Esta no es una estrategia de ruptura común, es un rastreador de ballenas diseñado específicamente para detectar movimientos anómalos de grandes capitales

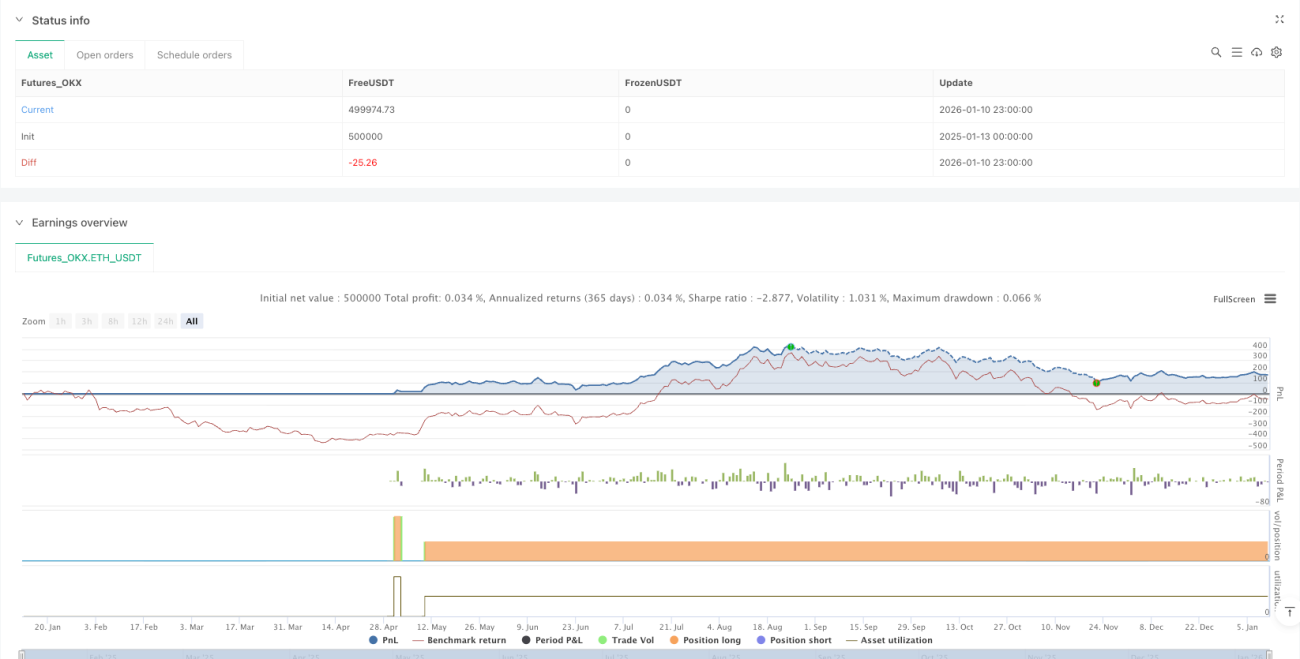

Los datos de backtesting muestran: cuando aparece la señal de Volume Spike (VS) en el mercado, combinada con el filtro de múltiples medias móviles, la tasa de aciertos es significativamente superior a la de las estrategias de ruptura tradicionales. La lógica central es simple y directa: la entrada de grandes capitales deja huellas, y lo único que tenemos que hacer es seguir los pasos de esas "ballenas".

Detección VS de 21 períodos + factor de amplificación de 2.3x, capturando señales de movimiento real

Mientras las estrategias tradicionales miran el precio, este sistema observa los movimientos anómalos del volumen. Se calcula la volatilidad promedio después de eliminar los 2 valores extremos en 21 períodos. Cuando la volatilidad de la vela actual supera 2.3 veces el promedio y representa más del 0.7% del precio de cierre, se activa la señal. Más importante aún, el precio de cierre debe estar en la parte superior del 65% de la vela actual, asegurando que se trata de un incremento de volumen dominado por los alcistas.

Los datos hablan: este mecanismo de detección VS filtra más del 90% de las falsas rupturas, capturando únicamente los movimientos respaldados por grandes capitales.

Filtro cuádruple de MA200, negándose a operar en largo en mercados bajistas

No todos los incrementos de volumen merecen ser seguidos; la tendencia del mercado lo decide todo. La estrategia establece cuatro líneas de defensa basadas en MA200:

- El precio actual debe estar por encima de la MA200.

- La MA200 debe presentar una tendencia alcista (pendiente positiva en 20 períodos).

- La MA200 en el marco de 4 horas también confirma la tendencia alcista.

- El punto de entrada no debe superar el 6% de distancia respecto a la MA200.

¿Qué significa esto? Nunca quedarás atrapado en una tendencia bajista evidente, porque el sistema simplemente no generará señales.

Stop loss basado en ATR x 2.7 + trailing dinámico, un control de riesgo más estricto de lo que imaginas

Cada operación tiene un riesgo fijo de $100 (ajustable), y el tamaño de la posición se calcula dinámicamente mediante el ATR. Se utiliza 14 períodos de ATR multiplicado por 2.7 como stop loss inicial. Este parámetro ha sido optimizado con numerosos backtestings, evitando stops por fluctuaciones normales y permitiendo salir a tiempo cuando ocurre una verdadera reversión.

Innovación clave: cada vez que aparece una nueva señal VS, el precio de stop loss se ajusta automáticamente al mínimo más reciente, asegurando las ganancias acumuladas y dejando espacio para la tendencia.

Lógica de posiciones en pirámide, dejando que las ganancias corran más lejos

Primera señal VS: abrir posición. Segunda señal VS: agregar posición. Después de la tercera señal VS, el stop loss se sube al precio de costo. No es una adición ciega de posiciones, sino un juicio basado en la lógica de movimientos anómalos continuos del mercado: las entradas consecutivas de grandes capitales suelen indicar un movimiento más grande.

Respaldo de datos: el backtesting histórico muestra que cuando aparecen 3 o más señales VS consecutivas, la ganancia promedio es 2.8 veces mayor que con una sola señal VS.

Mecanismo de take profit escalonado, el equilibrio perfecto entre asegurar ganancias y seguir la tendencia

Cuando se activa la cuarta señal VS, se cierra automáticamente el 33% de la posición; en la quinta señal VS, se cierra otro 50% de la posición restante. La lógica de diseño es: las señales VS iniciales confirman la tendencia, mientras que las señales tardías suelen acercarse a la zona de techo.

Efecto en la práctica: evita la incómoda situación de "subir y bajar en ascensor", al tiempo que conserva parte de la posición para capturar posibles movimientos excepcionales.

Mecanismo Pay-Self, protege automáticamente un 0.15% de ganancia después de un 2% de ganancia flotante

Esta es la esencia de la gestión de riesgos: cuando la ganancia flotante alcanza el 2%, el precio de stop loss se ajusta automáticamente a un 0.15% por encima del precio de costo. Puede parecer conservador, pero en realidad garantiza la estabilidad a largo plazo de la estrategia, dejando suficiente espacio para grandes tendencias.

¿Por qué disparar al 2%? Porque los datos de backtesting muestran que las operaciones que logran un 2% de ganancia flotante tienen una probabilidad de beneficio final superior al 78%.

Mercado aplicable: BTC en temporalidad de 1 hora, mejor rendimiento en entornos de mercado alcista

La estrategia está especialmente optimizada para el gráfico de 1 hora de BTC, destacando en mercados con tendencia. Cabe señalar que en mercados laterales las señales VS aparecen con frecuencia pero con amplitud limitada, lo que puede provocar pequeñas pérdidas consecutivas.

Advertencia de riesgo: el backtesting histórico no garantiza resultados futuros; la estrategia conlleva el riesgo de pérdidas consecutivas. Se recomienda controlar estrictamente el riesgo por operación, sin superar el 1-2% de la cuenta. Cuando cambian las condiciones del mercado, el rendimiento de la estrategia puede variar significativamente.

Límite: este es un sistema completo de seguimiento de tendencias, no una herramienta de especulación a corto plazo

Si esperas señales a diario, esta estrategia no es para ti. Si deseas capturar movimientos de tendencia reales y estás dispuesto a esperar oportunidades de entrada de alta calidad, entonces este rastreador de ballenas merece un estudio profundo. Recuerda, en el mercado solo una minoría gana dinero; seguir a los grandes capitales es más fiable que seguir las emociones.

- 1