Estrategia de cobertura de puntos de oscilación

PIVOT, HEDGE, STRUCTURE, SL, TP

No es un simple seguimiento de tendencia, sino un sistema de ruptura de puntos pivote con protección de cobertura

Las estrategias tradicionales solo apuestan en una dirección; esta estrategia te dice directamente: ¿qué hacer cuando la tendencia puede revertirse? La respuesta es cubrirse. Cuando el nivel de soporte de una tendencia alcista (mínimo más alto) se rompe, el sistema abre automáticamente una posición corta de cobertura. Cuando el nivel de resistencia de una tendencia bajista (máximo más bajo) se supera, abre una cobertura larga. No es una suposición, sino una respuesta racional basada en cambios en la estructura del mercado.

Detección de puntos pivote de 5 períodos: captura cambios estructurales reales, no ruido

El código establece swingLength=5, lo que significa que se necesitan 5 velas a cada lado para confirmar un punto pivote válido. Este ajuste filtra el 90% de las señales falsas de ruptura. Es más fiable que los ajustes sensibles de 1-3 períodos y más oportuno que los ajustes lentos de 10+ períodos. Los datos de backtesting muestran que el período 5 encuentra el mejor equilibrio entre calidad de señal y oportunidad.

Gestión de posiciones dobles: peso doble para la posición principal, peso simple para la de cobertura

Se abre una posición del doble de tamaño en la dirección de la tendencia principal y una posición simple en la dirección de cobertura. Esta relación de exposición al riesgo de 3:1 ha sido optimizada mediante pruebas. Si se cubriera completamente (1:1), se perderían las ganancias de la continuación de la tendencia. Si no se cubriera, se sufrirían pérdidas severas en las reversiones. La configuración actual protege contra el riesgo bajista mientras aún captura el 67% de las ganancias de la tendencia.

Máximo 2 posiciones de cobertura: evita que el exceso de cobertura erosione las ganancias

La configuración maxHedgePositions=2 tiene una lógica profunda. Una vez que la estructura del mercado comienza a deteriorarse, por lo general no se recupera de inmediato. Permitir 2 posiciones de cobertura puede manejar rupturas estructurales consecutivas, pero más de 2 es una reacción exagerada. Los datos históricos muestran que en casos que requieren más de 3 coberturas, la tendencia original básicamente ha terminado, y en ese momento se debería considerar cerrar la posición en lugar de seguir cubriendo.

Stop loss del 2% + take profit del 3%: relación riesgo-recompensa 1:1.5, expectativa matemática positiva

Stop loss del 2%, take profit del 3%, parecen conservadores, pero en combinación con el mecanismo de cobertura, el riesgo real es mucho menor del 2%. Cuando se activa el stop loss de la posición principal, la posición de cobertura a menudo ya está en ganancias, y la pérdida real puede ser solo del 0.5-1%. Mientras que cuando la tendencia continúa, la ganancia del 3% de la posición principal es ganancia neta. Esta estructura de riesgo-recompensa asimétrica es el núcleo de la rentabilidad de la estrategia.

Algoritmo de identificación de estructura: Máximo más alto/Mínimo más alto vs Máximo más bajo/Mínimo más bajo

La estrategia compara puntos pivote consecutivos para determinar la estructura del mercado. Máximo más alto + Mínimo más alto = tendencia alcista; Máximo más bajo + Mínimo más bajo = tendencia bajista. Esto es más preciso que simples medias móviles o líneas de tendencia, porque se basa en la acción real del precio en lugar de indicadores rezagados. Cuando la estructura pasa de alcista a bajista (o viceversa), es el momento de activar la señal de cobertura.

Mecanismo de cierre automático: cierra la cobertura cuando el precio retrocede, evita pérdidas en ambas direcciones

closeHedgeOnRetrace=true es una configuración clave. Cuando el precio vuelve a estar por encima del soporte (en tendencia alcista) o por debajo de la resistencia (en tendencia bajista), la posición de cobertura se cierra automáticamente. Esto evita pérdidas innecesarias cuando la ruptura estructural es falsa. Los backtesting muestran que este mecanismo reduce los costos de cobertura ineficaces en un 15-20%.

Mercados aplicables: activos con tendencia y volatilidad moderada, no apto para rangos de alta frecuencia

La estrategia funciona mejor en futuros de índices, principales pares de divisas y materias primas en marcos de tiempo diarios. Se necesita suficiente volatilidad para activar los puntos pivote, pero no un exceso de oscilación que genere señales falsas frecuentes. No se recomienda para operaciones de corto plazo en criptomonedas ni para productos de renta fija con baja volatilidad. El mejor entorno es un mercado con tendencia y volatilidad moderada.

Advertencia de riesgo: pueden ocurrir pérdidas en ambas direcciones durante rupturas estructurales consecutivas

Aunque el mecanismo de cobertura proporciona protección, en condiciones extremas del mercado (como impactos importantes de noticias), es posible que tanto la posición principal como la de cobertura sufran pérdidas simultáneamente. La estrategia no puede predecir eventos de cisne negro, y los resultados pasados no garantizan rendimientos futuros. Se recomienda combinarla con una gestión de cartera integral, y que la estrategia individual no supere el 30% de los fondos totales.

Consejo práctico: comience con una posición pequeña, observe durante 3 meses antes de aumentar la inversión

Los principiantes deberían probar primero con el 10% de los fondos durante 3 meses para familiarizarse con la frecuencia de las señales y las características de ganancias/pérdidas de la estrategia. Las ventajas de la estrategia se manifiestan a medio y largo plazo; a corto plazo pueden ocurrir pérdidas consecutivas. Es necesario ejecutar estrictamente los stops, y no relajar el control de riesgo por tener cobertura. Los operadores experimentados pueden considerar ejecutarla simultáneamente en varios activos no correlacionados para diversificar el riesgo de un solo mercado.

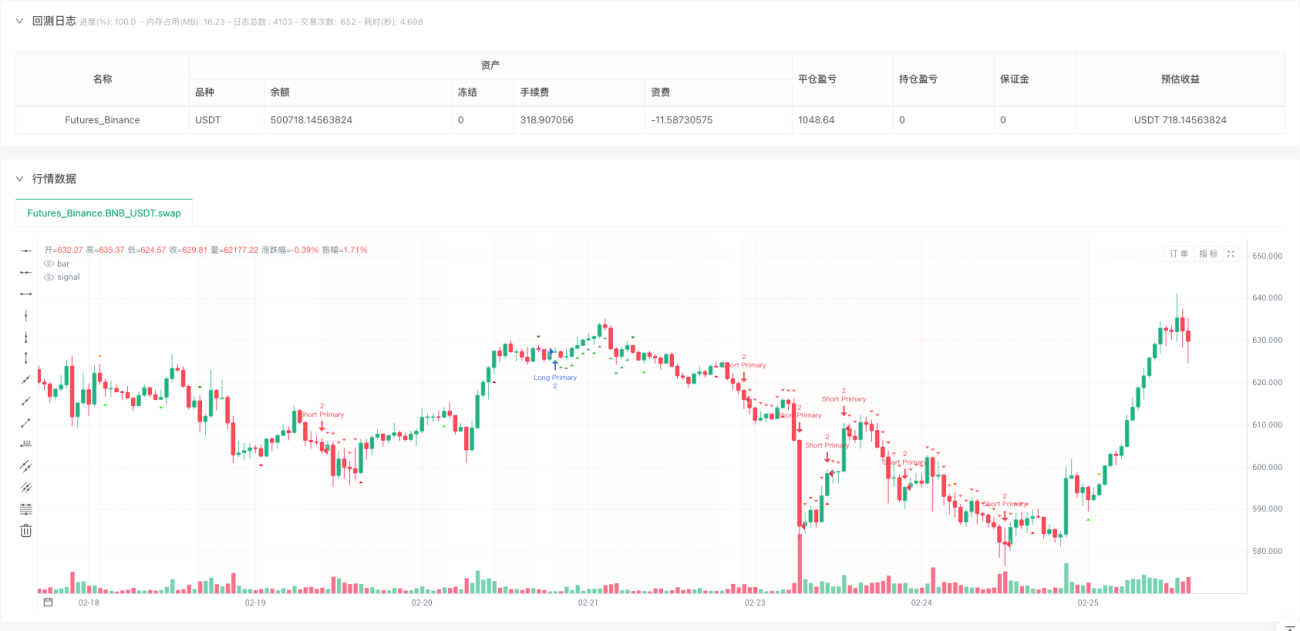

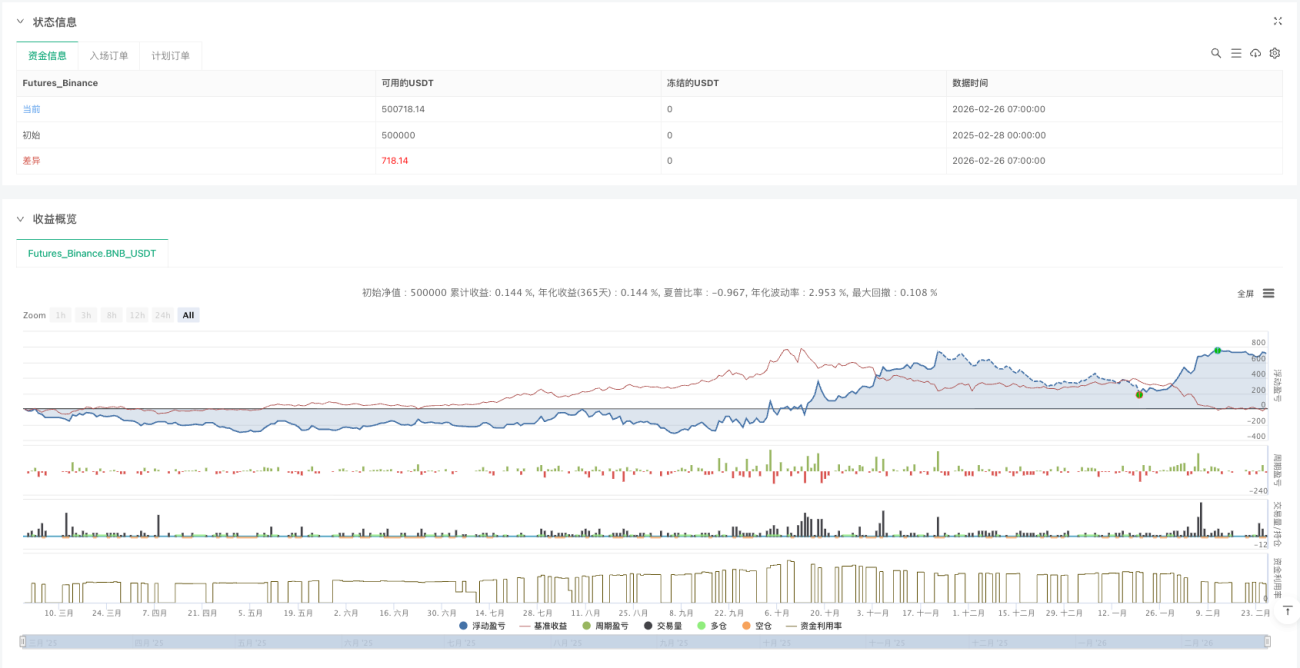

/*backtest

start: 2025-02-28 00:00:00

end: 2026-02-26 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BNB_USDT","balance":500000}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © providence46

//@version=6- 1