Stratégie de trading en range à triple mode

Aperçu

La stratégie de trading d'oscillation à triple mode est une stratégie de trading à court terme basée sur une combinaison de plusieurs indicateurs techniques. Elle combine l'indicateur SuperTrend, la moyenne mobile mixte SSL et l'indicateur QQE amélioré pour former des signaux de trading stables. Elle convient aux instruments financiers très volatils comme les crypto-monnaies et les actions, et montre de bonnes performances en particulier après les périodes de rupture.

Principe

Signal d'entrée

Entrée en position longue :

- Le SuperTrend passe de baissier à haussier

- Le prix de clôture franchit à la hausse la bande supérieure de la moyenne mobile mixte SSL

- La version améliorée du QQE est bleue (haussier)

Entrée en position courte :

- Le SuperTrend passe de haussier à baissier

- Le prix de clôture franchit à la baisse la bande inférieure de la moyenne mobile mixte SSL

- La version améliorée du QQE est rouge (baissier)

Signal de sortie

Sortie de position longue : Le SuperTrend passe de haussier à baissier

Sortie de position courte : Le SuperTrend passe de baissier à haussier

Stop-loss

Possibilité de choisir un stop-loss en pourcentage, basé sur l'ATR, ou sur les plus hauts/plus bas récents.

Take-profit

Possibilité de définir un ratio de profit de take-profit, le prix de take-profit est calculé automatiquement.

Gestion du capital

Option d'utiliser ou non une logique de gestion du capital pour contrôler la taille des positions.

Graphiques

- Tracer la ligne SuperTrend et le canal de moyenne mobile mixte SSL

- Option d'afficher ou non la moyenne mobile EMA

- Tracer les lignes d'ouverture, de stop-loss et de take-profit pour les positions longues et courtes

- Afficher les étiquettes d'ouverture des positions longues et courtes

Avantages

-

Combinaison de plusieurs indicateurs pour des signaux de trading stables

En combinant le SuperTrend, la moyenne mobile mixte SSL et l'indicateur QQE amélioré, les différents indicateurs se valident mutuellement, ce qui permet de filtrer les fausses ruptures et de générer des signaux de haute qualité.

-

Convient au trading d'oscillation sur les instruments volatils

La stratégie adopte une approche de trading à court terme, se concentrant sur la capture des fluctuations de prix à moyen et court terme. Le SuperTrend suit efficacement la tendance des prix, tandis que la moyenne mobile mixte SSL identifie clairement les niveaux de support et de résistance. Leur combinaison permet de générer des bénéfices sur les marchés oscillants.

-

Plusieurs options de stop-loss et take-profit

Le stop-loss peut être défini en pourcentage, basé sur l'ATR ou sur les extrêmes récents. Le take-profit peut être défini via un ratio de profit. La gestion du capital permet de contrôler la taille des positions. L'utilisateur peut librement combiner ces éléments en fonction des caractéristiques de l'instrument et de sa tolérance au risque.

-

Graphiques clairs

Les graphiques de la stratégie sont clairs et affichent visuellement les niveaux de stop-loss et de take-profit. Les lignes d'ouverture sont facilement identifiables pour repérer les signaux de trading.

Risques et optimisation

-

Possibilité de petites pertes

En raison du trading à court terme, il est impossible d'éviter complètement les petites pertes dues aux oscillations normales. On peut élargir la marge de stop-loss ou optimiser la logique de gestion du capital.

-

Risque de fausses ruptures

En cas de fausse rupture de prix, des signaux erronés peuvent se former. Tester différentes périodes d'EMA pourrait filtrer les fausses ruptures, ou optimiser les paramètres des indicateurs de tendance.

-

Risque de défaillance des indicateurs de base

Si les indicateurs de base ne fonctionnent plus, cela peut générer de multiples signaux erronés. Il est nécessaire de vérifier régulièrement l'efficacité des indicateurs et d'ajuster dès que des problèmes sont détectés.

-

Optimisation de la période de backtest

La période de backtest actuelle est fixe et ne correspond pas aux différents cycles de marché des instruments. Il est recommandé d'optimiser pour correspondre à la période de trading principale du contrat.

-

Optimisation de l'adaptabilité aux instruments

Il est possible d'ajuster finement les paramètres de la stratégie en fonction des caractéristiques des données de chaque instrument pour augmenter le taux de réussite des positions longues et courtes. Une approche d'optimisation pas à pas est recommandée pour comparer l'impact des différents paramètres sur la stratégie.

Conclusion

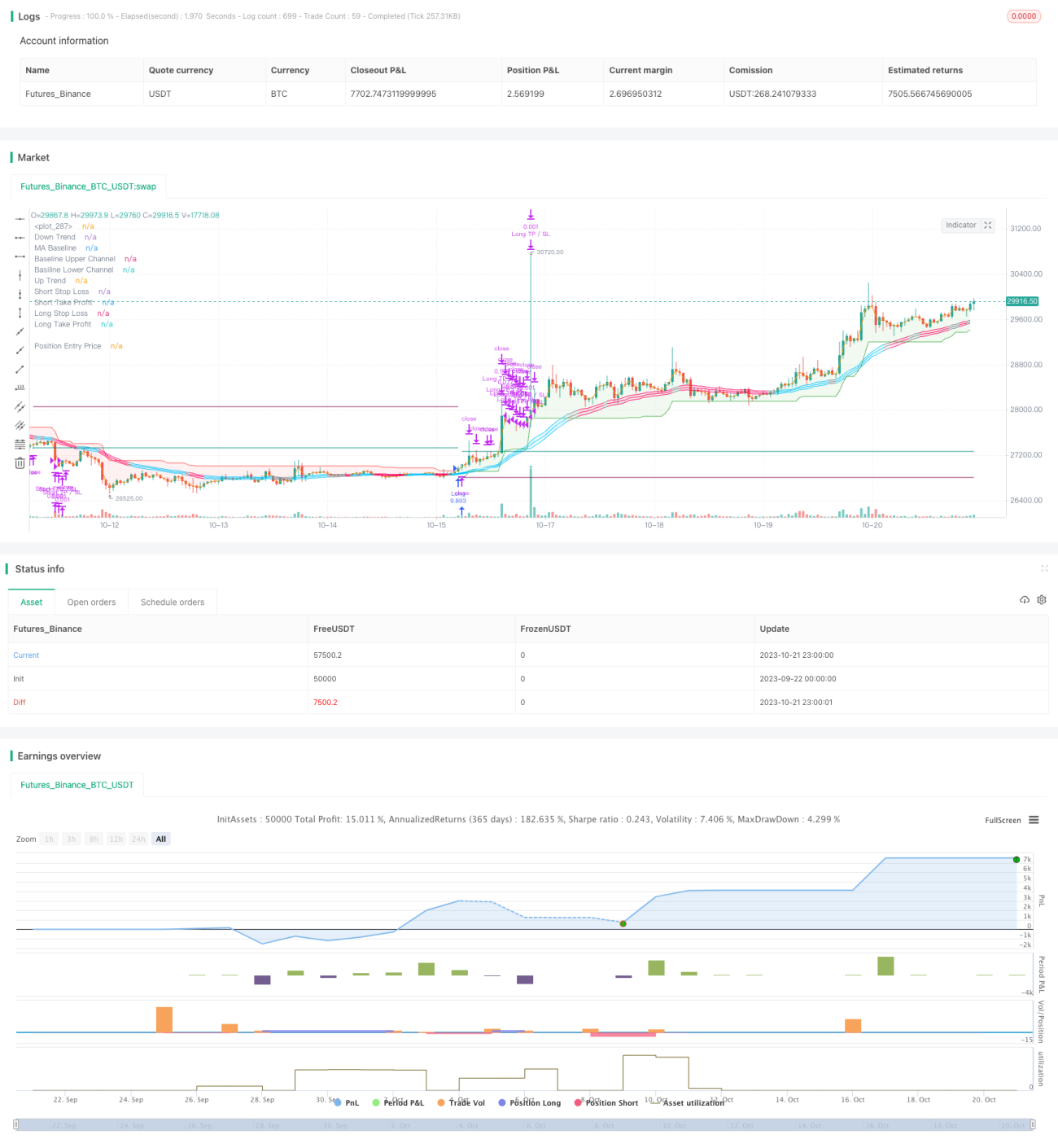

Cette stratégie génère des signaux de trading en combinant plusieurs indicateurs, ce qui permet de filtrer efficacement les fausses ruptures. Elle convient aux crypto-monnaies et aux actions individuelles très volatiles. Elle offre également plusieurs options de stop-loss et take-profit, ce qui la rend flexible. Globalement, la stratégie produit des signaux de trading stables et peut générer de bons rendements sur les marchés oscillants à moyen et court terme. En optimisant davantage, on peut adapter les paramètres aux différents instruments de trading et améliorer le profit factor. Cette stratégie est un système de trading efficace qui mérite d'être étudié en profondeur.

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to myncrypto, jason5480, kevinmck100

// @version=5- 1